MLOpsの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

MLOps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1664839

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

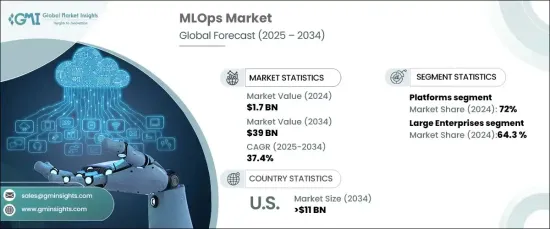

世界のMLOps市場は2024年に17億米ドルとなり、2025年から2034年までのCAGRは37.4%と堅調な成長が予測されています。

クラウドプラットフォームは、膨大なデータセットと複雑な機械学習ワークフローを効率的に管理するために必要な拡張性と柔軟性を提供するため、クラウドコンピューティングへの移行の増加が大きな推進力となっています。

クラウドベースのMLOpsソリューションにより、企業は複数の環境にシームレスにモデルを展開できます。このアプローチにより、オンプレミスの大規模なインフラが不要になると同時に、パフォーマンスとスケーラビリティが向上します。これらのソリューションを活用することで、企業は機械学習の運用を合理化し、より効率的に進化する需要に対応することができます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 17億米ドル |

| 予測金額 | 390億米ドル |

| CAGR | 37.4% |

新しい機械学習モデルの市場投入までの時間を短縮することは、競争力の維持を目指す組織にとって重要な優先事項となっています。MLOpsプラットフォームは、継続的インテグレーションと継続的デプロイメント(CI/CD)によって開発、テスト、デプロイメントのプロセスを自動化することで、これを促進します。この自動化により、ワークフローが加速し、手作業による介入が最小限に抑えられ、モデルの拡張性と一貫した更新が保証されます。

MLOps市場は、コンポーネント別にプラットフォームとサービスに区分されます。2024年にはプラットフォームが市場をリードし、総シェアの72%を占めました。この優位性は、データパイプライン管理、モデル展開、実験追跡、パフォーマンスモニタリングを統合するエンドツーエンドのソリューションに対する需要の高まりに起因します。包括的なプラットフォームは、ワークフローを簡素化しながら人工知能イニシアチブを拡大しようとする企業にますます支持されています。

コンサルティング、統合、マネージドサービスなどのサービスも大きな成長を遂げています。これらのサービスは、クラウド移行、インフラ最適化、コンプライアンス要件などの導入課題を克服するために組織を支援します。オーダーメイドのガイダンスに対する需要の高まりは、MLOpsエコシステムにおける専門家によるサポートの重要性を浮き彫りにしています。

最終用途別では、市場は大企業と中小企業に分類されます。2024年には、大企業が64.3%の市場シェアを占め、AIワークフローの最適化、予測分析の強化、ガバナンスの改善を目的としたMLOpsソリューションの採用が牽引しています。一方、中小企業は、プロセスの自動化とイノベーションの促進を可能にする、コスト効率が高く使いやすいツールを急速に導入しています。AIツールの利用しやすさが増していることもこの動向を後押ししており、中小企業は多額のインフラ投資を行うことなく拡張性を実現できます。

北米では、米国がMLOps市場をリードしており、2034年までに110億米ドルを超えると予測されています。ヘルスケア、金融、製造業などの業界でAIと機械学習が積極的に採用されていることが、市場拡大の推進において極めて重要な役割を担っていることを裏付けています。クラウドインフラと高性能コンピューティングへの投資はMLOpsソリューションの採用をさらに促進し、企業のモデル運用の改善と展開時間の短縮を支援します。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 一次調査と検証

- 一次ソース

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- テクノロジープロバイダー

- モデル開発とトレーニングプラットフォーム

- データ管理プロバイダー

- モデル展開とガバナンスのプロバイダー

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- MLOpsの使用事例

- テクノロジーとイノベーションの展望

- 主なニュースと取り組み

- 規制状況

- 影響要因

- 成長促進要因

- AIと機械学習の採用拡大

- モデル展開の迅速化の要求

- 規制コンプライアンスとモデルガバナンス

- クラウドの採用と拡張性

- 業界の潜在的リスク・課題

- データプライバシーとセキュリティへの懸念

- 熟練した専門家の不足

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- プラットフォーム

- サービス

第6章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- クラウドベース

- オンプレミス

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 大企業

- 中小企業

第8章 市場推計・予測:業界別、2021年~2034年

- 主要動向

- ヘルスケア

- 小売・eコマース

- 製造・サプライチェーン

- BFSI

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Alteryx

- Amazon Web Services(AWS)

- Atos

- Capgemini

- Cisco

- Cloudera

- Databricks

- Google Cloud

- H2O.ai

- IBM

- Microsoft

- NVIDIA

- Oracle

- Red Hat

- Salesforce

- SAP

- Siemens

- TIBCO Software

- VMware

- Weights &Biases

目次

The Global MLOps Market was valued at USD 1.7 billion in 2024 and is forecasted to grow at a robust CAGR of 37.4% from 2025 to 2034. The increasing shift towards cloud computing serves as a major driver, as cloud platforms offer the scalability and flexibility needed to manage extensive datasets and complex machine learning workflows efficiently.

Cloud-based MLOps solutions enable organizations to deploy models seamlessly across multiple environments. This approach eliminates the need for extensive on-premises infrastructure while delivering enhanced performance and scalability. By leveraging these solutions, businesses can streamline machine learning operations and adapt to evolving demands with greater efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 billion |

| Forecast Value | $39 billion |

| CAGR | 37.4% |

Reducing the time-to-market for new machine learning models has become a critical priority for organizations aiming to maintain a competitive edge. MLOps platforms facilitate this by automating the development, testing, and deployment processes through continuous integration and continuous deployment (CI/CD). This automation accelerates workflows, minimizes manual intervention, and ensures models remain scalable and consistently updated.

The MLOps market is segmented by components into platforms and services. Platforms led the market in 2024, capturing 72% of the total share. This dominance stems from the growing demand for end-to-end solutions that unify data pipeline management, model deployment, experiment tracking, and performance monitoring. Comprehensive platforms are increasingly favored by enterprises seeking to scale artificial intelligence initiatives while simplifying their workflows.

Services, including consulting, integration, and managed services, are also witnessing significant growth. These services assist organizations in overcoming adoption challenges such as cloud migration, infrastructure optimization, and compliance requirements. The rise in demand for tailored guidance highlights the importance of expert support in the MLOps ecosystem.

By end use, the market is categorized into Large Enterprises and SME. In 2024, Large Enterprises held a 64.3% market share, driven by the adoption of MLOps solutions to optimize AI workflows, enhance predictive analytics, and improve governance. Meanwhile, SME are rapidly embracing cost-effective, user-friendly tools that enable them to automate processes and foster innovation. The growing accessibility of AI tools supports this trend, allowing smaller businesses to achieve scalability without heavy infrastructure investments.

In North America, the United States leads the MLOps market, projected to surpass USD 11 billion by 2034. The country's strong adoption of AI and machine learning across industries such as healthcare, finance, and manufacturing underscores its pivotal role in driving market expansion. Investments in cloud infrastructure and high-performance computing further propel the adoption of MLOps solutions, helping businesses improve model operations and reduce deployment times.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Technology providers

- 3.1.2 Model development and training platforms

- 3.1.3 Data management providers

- 3.1.4 Model deployment and governance providers

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Use cases of MLOps

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increased adoption of AI and machine learning

- 3.8.1.2 Demand for faster model deployment

- 3.8.1.3 Regulatory compliance and model governance

- 3.8.1.4 Cloud adoption and scalability

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Data privacy and security concerns

- 3.8.2.2 Lack of skilled professionals

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Platform

- 5.3 Services

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Cloud-based

- 6.3 On-Premises

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 ($Mn)

- 7.1 Key trends

- 7.2 Large enterprises

- 7.3 SME

Chapter 8 Market Estimates & Forecast, By Vertical, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Healthcare

- 8.3 Retail & e-commerce

- 8.4 Manufacturing & supply chain

- 8.5 BFSI

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alteryx

- 10.2 Amazon Web Services (AWS)

- 10.3 Atos

- 10.4 Capgemini

- 10.5 Cisco

- 10.6 Cloudera

- 10.7 Databricks

- 10.8 Google Cloud

- 10.9 H2O.ai

- 10.10 IBM

- 10.11 Microsoft

- 10.12 NVIDIA

- 10.13 Oracle

- 10.14 Red Hat

- 10.15 Salesforce

- 10.16 SAP

- 10.17 Siemens

- 10.18 TIBCO Software

- 10.19 VMware

- 10.20 Weights & Biases

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日