|

市場調査レポート

商品コード

1871284

ローラーベアリング市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測Roller Bearings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ローラーベアリング市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年10月30日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

概要

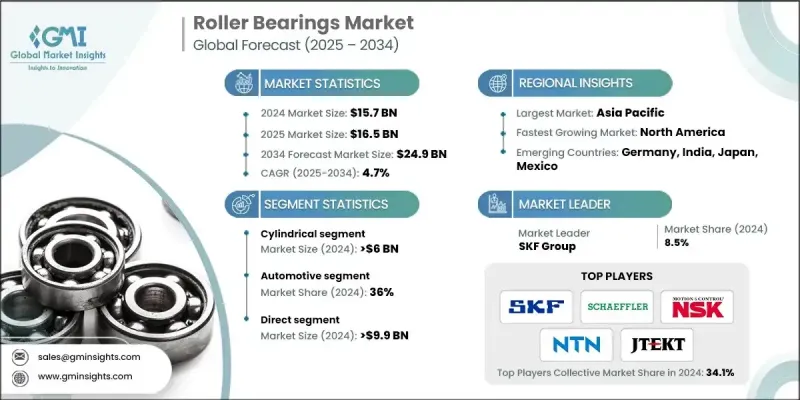

世界のローラーベアリング市場は、2024年に157億米ドルと評価され、2034年までにCAGR4.7%で成長し、249億米ドルに達すると予測されています。

ローラーベアリングは、建設、鉱業、製造業など、信頼性と耐久性が効率的な操業の鍵となる産業において、不可欠な部品として機能しております。産業分野全体での自動化と先進機械の導入拡大は、重荷重、高圧力、極端な温度変動に対応可能な高性能ベアリングの需要を牽引しております。産業自動化と省エネルギーシステムを推進する各国政府の取り組みも、市場の成長をさらに加速させております。研究開発への注力が進む中、ローラーベアリングは過酷な産業環境において、性能・精度・寿命の向上を実現する方向へ進化を続けております。再生可能エネルギーやスマート製造を支援する世界的な取り組みも市場の進化に影響を与え続け、効率性と稼働安定性を高めるイノベーションを促進しております。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年度 | 2025-2034 |

| 開始時価値 | 157億米ドル |

| 予測金額 | 249億米ドル |

| CAGR | 4.7% |

円筒ころ軸受セグメントは、2024年に60億米ドルに達しました。これは、重いラジアル荷重を支え、高速で効率的に動作する軸受への需要に牽引されたものです。これらの軸受は、産業用モーター、製造、自動車システムで広く採用されています。産業用モーターだけで製造業の総エネルギー消費量の半分以上を占めており、円筒ころ軸受はそれらの運転効率向上に重要な役割を果たしています。これにより、省エネルギーとメンテナンスコスト削減を求める業界全体で強い需要が生じています。

直接販売セグメントは2024年に99億米ドルに達し、OEMとの直接的なパートナーシップ維持の有効性によりローラーベアリング市場を独占しています。直接流通により、メーカーはカスタマイズされたソリューションを提供すると同時に、円滑なコミュニケーションと技術協力を確保できます。このアプローチは、精度、品質保証、性能の信頼性がOEMの主要な意思決定要因となる自動車、航空宇宙、重機製造などの高付加価値分野において特に有益です。

米国ローラーベアリング市場は2024年に77.1%のシェアを占めました。同国の先進的な製造エコシステム、強固な自動車産業基盤、拡大を続ける航空宇宙・重機セクターが成長の主要因です。継続的な技術開発と主要業界プレイヤーの存在が、米国を地域における主導的勢力として強化し、産業用ローラーベアリングの国内外需要を支えています。

グローバルローラーベアリング市場の主要企業には、NBIベアリングス・欧州、HKTベアリングス、C&Uグループ、ミネベア、NTN、NSK、SKF、シェフラーグループ、ティムケン社、RBCベアリングス、ブラマー、大同金属工業、ハルビンベアリング製造、JTEKT、レックスノードなどが挙げられます。ローラーベアリング市場の企業は、技術革新、製品の多様化、戦略的提携に注力し、グローバルな存在感を強化しています。研究開発への多額の投資により、過酷な環境下でも効率的に機能する先進的で高耐久性のベアリングを開発することが可能となっています。多くの企業が自動化とスマート製造プロセスを導入し、精度の向上と生産コストの削減を図っています。産業、自動車、航空宇宙分野のOEMメーカーとの連携により、長期契約と製品カスタマイズの機会を確保しています。地域的な製造拠点とサプライチェーンの拡大により、迅速な納品とコスト効率の向上が可能となります。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 産業の拡大と自動化

- 自動車産業の成長

- 技術的進歩と製品革新

- 業界の潜在的リスク&課題

- 高い生産コスト

- 代替技術の台頭

- 機会

- 省エネルギー型およびスマートローラーベアリングシステム

- 産業オートメーションおよびスマート製造の成長

- 促進要因

- 成長可能性分析

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- タイプ別

- 規制情勢

- 規格およびコンプライアンス要件

- 地域別規制枠組み

- 認証基準

- 貿易統計(HSコード-8482)

- 主要輸入国

- 主要輸出国

- ギャップ分析

- リスク評価と軽減策

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協力関係

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- 円筒形

- テーパー加工

- 球状

- その他

- 針

- 推力

- 分割

第6章 市場推計・予測:材料別、2021-2034

- 主要動向

- 鋼材

- セラミック

- ポリマー

- ハイブリッド

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- ギアボックス

- 電気モーター

- ポンプ及びコンプレッサー

- 風力タービン

- コンベヤ

- 工作機械

第8章 市場推計・予測:最終用途産業別、2021-2034

- 主要動向

- 自動車

- 農業

- 電気

- 鉱業・建設業

- 鉄道・航空宇宙産業

- 自動車アフターマーケット

- その他

第9章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 直接販売

- 間接

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Brammer

- C&U Group

- Daido Metal

- Harbin Bearing Manufacturing

- HKT Bearings

- JTEKT

- Minebea

- NBIベアリングス・欧州

- NSK

- NTN

- RBC Bearings

- Rexnord

- Schaeffler Group

- SKF

- The Timken Company