|

市場調査レポート

商品コード

1913479

軌道敷設設備市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Track Laying Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 軌道敷設設備市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月23日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

概要

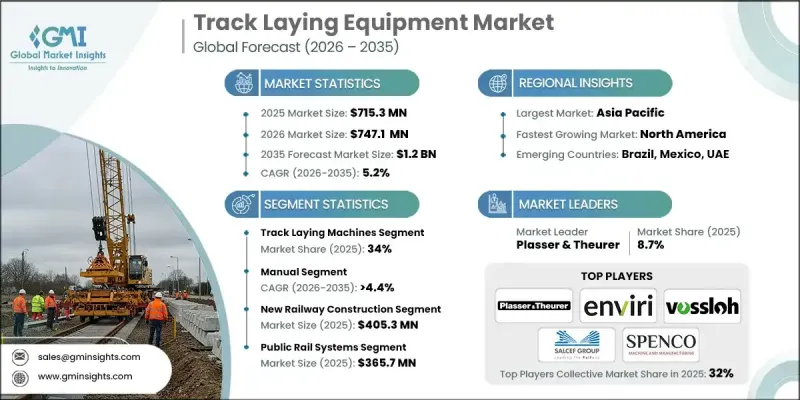

世界の軌道敷設設備市場は、2025年に7億1,530万米ドルと評価され、2035年までにCAGR5.2%で成長し、12億米ドルに達すると予測されています。

市場拡大の背景には、大規模な鉄道ネットワーク開発、都市部人口増加の加速、新規鉄道路線への投資拡大、ならびに既存鉄道資産の改修需要の増加が挙げられます。鉄道当局、地下鉄事業者、貨物輸送サービス提供者は、施工精度の向上、ライフサイクルコストの削減、厳格なプロジェクト納期遵守に注力しています。その結果、一貫した建設品質の達成、労働生産性の向上、長期的な軌道性能の強化を図る上で、現代的な軌道敷設ソリューションの導入が不可欠となっています。さらに、新規鉄道線路や改修プロジェクトにおける安全基準の遵守と精密設置への重視が高まっていることも、市場の見通しをさらに強固なものとしています。都市交通、貨物輸送網、長距離鉄道路線への継続的な投資は、技術基準を維持しつつ迅速な展開を支援する効率的な設備に対する持続的な需要を生み出しています。成熟地域と新興地域の双方において、鉄道インフラが経済成長とモビリティ開発の優先事項であり続ける中、軌道敷設設備市場は引き続き勢いを増しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 7億1,530万米ドル |

| 予測金額 | 12億米ドル |

| CAGR | 5.2% |

設備設計とデジタル統合の進歩により、鉄道線路の敷設および保守の方法が再構築されています。半自動化および自動化機械への移行は、インテリジェント制御システムや接続された監視プラットフォームと相まって、より一貫した生産性を実現し、手作業への依存度を低減しています。次世代軌道敷設ソリューションを採用する事業者にとって、精度向上、資産活用率の改善、ダウンタイムの削減が重要な利点となりつつあります。都市鉄道システムや長距離路線での導入拡大に伴い、プロジェクトライフサイクル全体を通じて効率性と耐久性を支える技術的に高度な設備への需要が高まっています。

2025年時点で軌道敷設機械セグメントは34%のシェアを占めました。この優位性は、線路と枕木の迅速な設置を支援しつつ、位置精度と施工の一貫性を維持する同セグメントの能力に起因します。地下鉄プロジェクト、貨物線、大規模インフラ開発における高い稼働率により、軌道敷設機械は現代の鉄道建設ワークフローの中核コンポーネントとしての地位を確立しています。

手動セグメントは2025年に55%のシェアを占め、2026年から2035年にかけてCAGR 4.4%での成長が見込まれています。手頃な価格、操作の簡便性、標準的な鉄道建設・保守作業への適応性により、高い採用率を維持しています。特に大規模自動化が未成熟な地域では、柔軟性と初期投資の低さから、多くの請負業者や鉄道当局が手動設備への依存を継続しています。

中国軌道敷設機器市場は2025年に42%のシェアを占めました。アジア太平洋地域は、広範な鉄道網拡張、高いインフラ支出、先進的な軌道建設ソリューションの導入増加に支えられ、主要地域市場として台頭しています。鉄道近代化と技術統合への継続的な投資が、同地域の強固な市場地位をさらに強化しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 世界の鉄道インフラの急速な拡大

- 軌道敷設および保守設備における技術的進歩

- 政府投資と近代化プログラム

- 都市化、工業化、および貨物需要の増加

- 業界の潜在的リスク&課題

- 高額な設備投資と機器コスト

- 熟練労働者不足と研修要件

- 市場機会

- 鉄道建設・保守の自動化とデジタル化

- 新興市場と新規鉄道プロジェクト

- 既存鉄道インフラのアップグレードと近代化

- デジタルおよび自動化された軌道敷設ソリューションの導入

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 米国連邦鉄道局(FRA)の規制

- カナダ運輸基準

- 欧州

- ドイツのTUVおよびBaFinへの準拠

- フランスDGITMガイドライン

- 英国鉄道規制庁(ORR)の規制

- イタリア国土交通省のコンプライアンス

- アジア太平洋地域

- 中国工業情報化部(MIIT)ガイドライン

- 日本の国土交通省基準

- 韓国国土交通省(MOLIT)の規制

- インド鉄道省及びBISガイドライン

- ラテンアメリカ

- ブラジルANTT及びDENIT規制

- メキシコ連邦通信運輸省(SCT)及びフェロカリレス社(FERROCARRILES)ガイドライン

- 中東・アフリカ

- アラブ首長国連邦道路交通局(RTA)ガイドライン

- サウジアラビア運輸総局(GAT)の規制

- 北米

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 自動化・ロボティクス

- AIと機械学習

- モノのインターネット(IoT)

- 新興技術

- ハイパーコネクテッド鉄道ネットワーク

- 軌道敷設向けロボティクス・アズ・ア・サービス(RaaS)

- AIによる予知保全と動的資源配分

- 現在の技術動向

- 価格動向

- 地域別

- 製品別

- コスト内訳分析

- 特許分析

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- 使用事例シナリオ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:機器別、2022-2035

- 軌道敷設機

- タンピングマシン

- バラストレギュレーター

- 枕木敷設機

- 溶接機

- その他

第6章 市場推計・予測:技術別、2022-2035

- マニュアル

- 半自動化

- 完全自動化

第7章 市場推計・予測:用途別、2022-2035

- 新規鉄道建設

- 線路保守

- アップグレードおよび近代化

第8章 市場推計・予測:最終用途別、2022-2035

- 公共鉄道システム

- 民間貨物運送会社

- 民間旅客事業者

- 防衛

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベルギー

- オランダ

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- シンガポール

- 韓国

- ベトナム

- インドネシア

- マレーシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Global Player

- Balfour Beatty Rail

- Enviri

- Harsco Rail

- Matisa

- Plasser &Theurer

- Salfec

- Spenco

- Tampertec

- Vossloh

- Weihua Group

- Regional Player

- Alstom Track Solutions

- CRRC Railway Equipment

- CSR Zhuzhou

- Kinki Sharyo

- Lloyds Register Rail

- Orenstein &Koppel

- Robel

- Shandong Railway Construction Machinery

- VAE Group

- ZTR Rail

- 新興企業

- Gulf Rail Technologies

- Metro Track Systems

- RailTech Innovations

- RapidRail Machinery

- TrackTech Solutions