|

市場調査レポート

商品コード

1928983

自動車ドアモジュール市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Automotive Door Module Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 自動車ドアモジュール市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月15日

発行: Global Market Insights Inc.

ページ情報: 英文 245 Pages

納期: 2~3営業日

|

概要

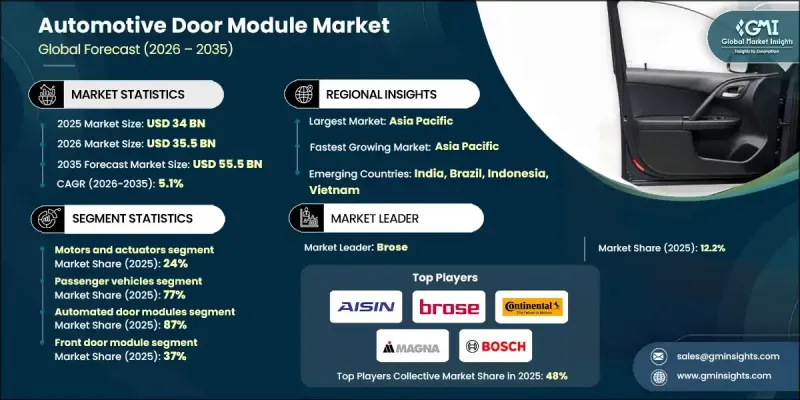

世界の自動車ドアモジュール市場は、2025年に340億米ドルと評価され、2035年までにCAGR5.1%で成長し、555億米ドルに達すると予測されています。

市場拡大は、世界の自動車生産の着実な成長と、現代車両における快適性・利便性・安全技術の統合進展によって牽引されています。電動モビリティへの移行加速はドアモジュール設計を再構築し、効率性と航続距離最適化を支える軽量素材や先進電子システムの採用を促進しています。自動車メーカーは組み立て時間短縮、生産ワークフローの効率化、製造コスト全体削減のため、モジュラー式車両アーキテクチャの優先度を高めています。複数のドア関連部品を単一モジュールに統合することで、取り付け時間の短縮、品質の一貫性向上、大量生産車両プラットフォーム全体での拡張性が実現されます。安全性や使いやすさの向上に対する消費者の期待の高まりも、市場成長をさらに後押ししています。アクセス制御、乗員保護、自動化機能に関連する特徴が車両カテゴリー全体で広く採用されつつあり、OEMメーカーによる統合ドアモジュールソリューションの大規模導入を促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 340億米ドル |

| 予測金額 | 555億米ドル |

| CAGR | 5.1% |

モーターおよびアクチュエーターセグメントは2025年に24%のシェアを占め、2026年から2035年にかけてCAGR6.1%で成長すると予測されています。このセグメントの需要拡大は、車両の電動化が進み、自動化機能の利用が増加していることに支えられています。これらの機能には、ドアシステムにシームレスに統合できるコンパクトでエネルギー効率の高い電気機械部品が求められています。

自動ドアモジュールセグメントは2025年に87%のシェアを占めました。電子制御式アクセスシステムおよびウィンドウシステムの各車種への普及拡大が、その強い採用を牽引しています。電気自動車および高級車の継続的な成長は、ドアモジュールの電子的複雑性をさらに高めており、自動化ソリューションへの持続的な需要を支えています。

中国自動車ドアモジュール市場は2025年に53%のシェアを占め、85億米ドルの規模に達しました。同国の優位性は、高い自動車生産台数と、量産車からプレミアム乗用車(電気自動車モデルを含む)に至る幅広い需要に支えられています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 増加する自動車生産台数

- 電気自動車および高級車の成長

- モジュラー車両アーキテクチャに焦点を当てて

- 安全性および快適性機能の向上

- 業界の潜在的リスク&課題

- 高度なシステム統合の複雑性

- OEMメーカーへのコスト圧力

- 市場機会

- 軽量素材の採用

- スマートドアおよびアクセス技術

- 新興自動車市場における拡大

- 成長可能性分析

- 規制情勢

- 北米

- 米国における車両安全対策

- FMVSS側面衝突基準

- カリフォルニア州車両規制適合性

- カナダ車両ガイドライン

- 欧州

- EU車両基準

- ユーロNCAPガイドライン

- 国内規制への適合

- ENドアモジュール規格

- アジア太平洋地域

- 中国における自動車規制

- インド安全基準

- 日本モジュールガイドライン

- 韓国規格

- ASEAN地域ガイドライン

- ラテンアメリカ

- ブラジルにおける自動車基準

- アルゼンチンにおけるコンプライアンス

- メキシコにおける規制

- 地域別安全ガイドライン

- 中東・アフリカ

- アラブ首長国連邦(UAE)車両基準

- サウジアラビアの規制

- 南アフリカにおけるコンプライアンス

- 地域別自動車基準

- 北米

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出入

- コスト内訳分析

- 特許分析

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- OEM採用とプラットフォーム普及率分析

- 価格設定、平均販売価格(ASP)及びコストの推移

- EVアーキテクチャがドアモジュール設計に与える影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:コンポーネント別、2022-2035

- ラッチ及びハンドル

- ウィンドウレギュレーター

- スピーカー

- モーター及びアクチュエータ

- 電気コネクタ及び配線

- 制御ユニット

- シールシステム

- その他

第6章 市場推計・予測:車両別、2022-2035

- 乗用車

- ハッチバック車

- セダン

- SUVおよびクロスオーバー車

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第7章 市場推計・予測:モジュール別、2022-2035

- 手動ドアモジュール

- 自動ドアモジュール

第8章 市場推計・予測:推進力別、2022-2035

- 内燃機関(ICE)

- BEV(バッテリー式電気自動車)

- ハイブリッド車

第9章 市場推計・予測:ドア別、2022-2035

- 玄関ドアモジュール

- リアドアモジュール

- 引き戸モジュール

- リフトゲートドアモジュール

第10章 市場推計・予測:販売チャネル別、2022-2035

- OEM

- アフターマーケット

第11章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- オランダ

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- シンガポール

- タイ

- インドネシア

- ベトナム

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

第12章 企業プロファイル

- 世界プレイヤー

- Aisin

- Brose

- Continental

- Denso

- Forvia

- Hyundai Mobis

- Magna International

- Robert Bosch

- Valeo

- ZF Friedrichshafen

- 地域プレイヤー

- Flex-N-Gate

- Grupo Antolin

- Hi-Lex

- Inteva Products

- PHA Korea

- 新興企業/ディスラプター

- CIE Automotive

- DaikyoNishikawa

- Dura Automotive Systems

- Hirotec

- Kiekert