|

市場調査レポート

商品コード

1913420

スペースランダー・ローバー市場の機会、成長促進要因、業界動向分析、予測(2026年~2035年)Space lander and Rover Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| スペースランダー・ローバー市場の機会、成長促進要因、業界動向分析、予測(2026年~2035年) |

|

出版日: 2025年12月19日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

概要

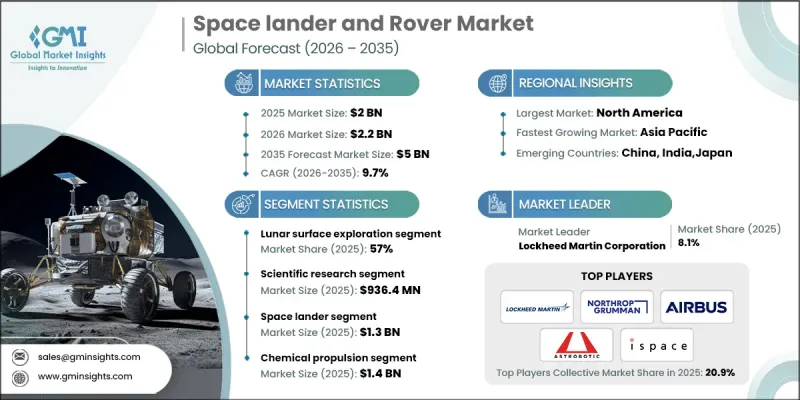

世界のスペースランダー・ローバーの市場規模は、2025年に20億米ドルと評価され、2035年までにCAGR9.7%で成長し、50億米ドルに達すると予測されています。

この成長は、惑星探査ミッションへの世界の関心の高まりと、自律移動・航法・ロボットシステムにおける継続的な進歩によって支えられています。政府や民間組織は、地球外探査目標に向けた長期資金提供を強化しており、これが先進的な地表探査プラットフォームの需要を牽引しています。民間セクターの参加拡大はイノベーションサイクルを加速させ、より軽量で高性能、かつコスト効率に優れたランダー・ローバーの開発を促進しています。搭載型知能、耐久性、エネルギー効率における技術的進歩が、市場の勢いをさらに強化しています。探査の野心が短期ミッションを超えて拡大するにつれ、過酷な環境下で動作可能な信頼性の高いシステムへの需要は増加の一途をたどっています。この進化する状況は、メーカーに対し、長期ミッションや将来のインフラ開発を支援する適応性の高いプラットフォームの開発を促しており、世界市場全体での着実な成長を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026年~2035年 |

| 開始時金額 | 20億米ドル |

| 予測金額 | 50億米ドル |

| CAGR | 9.7% |

月面探査セグメントは2025年に57%のシェアを占めました。このセグメントは、過酷な地表環境下で効率的に稼働可能な自律システムの需要拡大から恩恵を受けています。メーカー各社は、持続的な月面ミッションを支援しつつ、コスト効率と運用信頼性を維持するよう設計された先進的な移動プラットフォーム・資源利用技術を優先的に開発しています。

科学研究セグメントは2025年に9億3,640万米ドルの市場規模を生み出しました。このセグメントの成長は、探査ミッションへの投資増加と、惑星表面からの正確な科学データに対する需要拡大によって牽引されています。メーカー各社は、進化する研究目標に対応するため、高精度計測機器、堅牢なデータ収集システム、適応性の高いミッションアーキテクチャの開発に注力しています。

北米のスペースランダー・ローバー市場は2025年に48%のシェアを占めました。この地域優位性は、強力な公的資金、民間宇宙企業との連携強化、ミッション性能向上と運用コスト削減を目指す自律技術の急速な発展によって支えられています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 成長促進要因

- 月面・火星探査ミッションに対する世界の関心の高まり

- 自律航行・モビリティシステムにおける技術的進歩

- 民間セクターによる宇宙探査技術への投資と拡大

- 政府による長期的な月面・火星植民計画への取り組み

- 宇宙探査のための現地資源利用(ISRU)能力の開発

- 業界の潜在的リスクと課題

- 開発コストの高さと技術的複雑さ

- 過酷な宇宙環境によるミッション失敗のリスク

- 市場機会

- 持続可能な宇宙居住施設の開発

- 自律型探査技術の進展

- 成長促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 新興ビジネスモデル

- コンプライアンス要件

- 防衛予算分析

- 世界の防衛支出動向

- 地域別防衛予算配分

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

- 主要防衛近代化プログラム

- 予算予測(2026~2035年)

- 業界成長への影響

- 国別防衛予算

- セグメント別防衛予算配分

- 人員

- 運用・保守

- 調達

- 研究開発・試験評価

- インフラストラクチャー・建設

- 技術とイノベーション

- サプライチェーンのレジリエンス

- 地政学的分析

- 労働力分析

- デジタルトランスフォーメーション

- 合併・買収・戦略的提携の動向

- リスク評価と管理

- 主要契約授与(2022~2025年)

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 市場集中度分析

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオ比較

- 製品ラインの幅広さ

- 技術

- イノベーション

- 地理的プレゼンス比較

- 世界展開分析

- サービスネットワークのカバー率

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- チャレンジャー

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績比較

- 主な発展

- 合併・買収

- 提携・協業

- 技術的進歩

- 事業拡大と投資戦略

- サステナビリティへの取り組み

- デジタルトランスフォーメーションの取り組み

- 新興/スタートアップ競合の動向

第5章 市場推計・予測:ミッションタイプ別(2022年~2035年)

- 月面探査

- 火星表面探査

- 小惑星・彗星探査

第6章 市場推計・予測:車両タイプ別(2022年~2035年)

- スペースランダー

- スペースラローバー

第7章 市場推計・予測:推進方式別(2022年~2035年)

- 化学推進

- 電気推進/イオン推進

- ハイブリッド推進システム

第8章 市場推計・予測:用途別(2022年~2035年)

- 化学推進

- 電気推進/イオン推進

- ハイブリッド推進システム

第9章 市場推計・予測:最終用途別(2022年~2035年)

- 政府・防衛機関

- 宇宙探査機関

- 民間航空宇宙企業

- 研究機関

第10章 市場推計・予測:地域別(2022年~2035年)

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- 世界の主要企業

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- NASA

- Roscosmos

- Airbus SE

- 地域の主要企業

- 北米

- Blue Origin

- Canadian Space Agency

- アジア太平洋

- ISRO

- Japan Aerospace Exploration Agency(JAXA)

- China Academy of Space Technology

- 欧州

- European Space Agency

- Spacebit Technologies

- 北米

- ニッチ企業/ディスラプター

- Astrobotic Technology

- ispace, inc.