|

|

市場調査レポート

商品コード

1638824

シリンジ市場の機会、成長促進要因、産業動向分析、2024~2032年の予測Syringes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 - 2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| シリンジ市場の機会、成長促進要因、産業動向分析、2024~2032年の予測 |

|

出版日: 2024年11月04日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

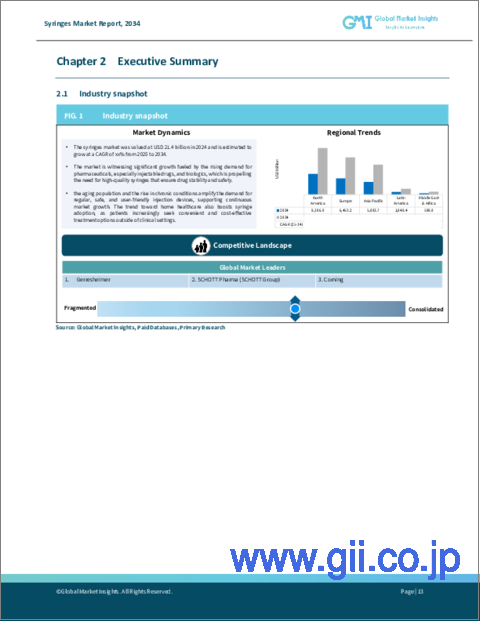

世界のシリンジ市場は2023年に196億米ドルと評価され、2024年から2032年までのCAGRは10.9%と予測されています。

シリンジは、流体の注入と引き抜きに不可欠な医療機器で、正確な流体制御のためのバレル、プランジャー、針またはノズルで構成されています。

この市場の成長を牽引しているのは、人口の高齢化と慢性的な健康状態の増加であり、これが安全で信頼性の高いシリンジに対する需要を高めています。さらに、在宅ヘルスケアの導入が増加していることも、患者が臨床の場を超えてより便利で手頃な価格の治療ソリューションを求めるようになり、シリンジの使用を後押ししています。

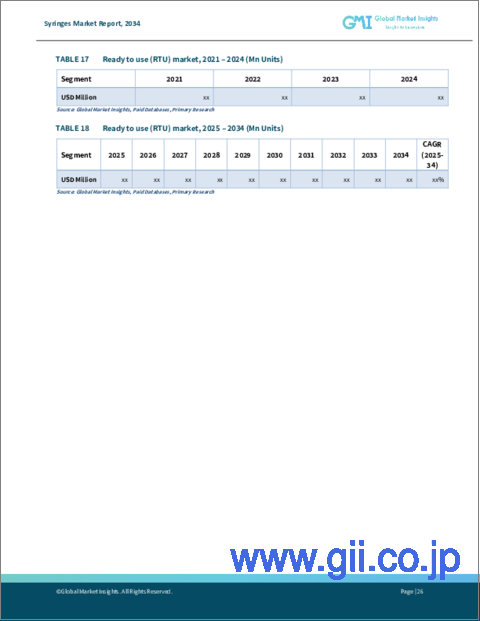

市場はプレパレーション別に、すぐに使える(RTU)シリンジと滅菌準備済み(RTS)シリンジに区分されます。RTUセグメントは、ヘルスケアプロバイダーと患者にとっての利便性により、CAGR予想11.1%で市場をリードしています。多くの場合、RTUシリンジには薬剤があらかじめ充填されているため、投与が簡素化され、投与ミスが最小限に抑えられ、汚染リスクが低減されます。RTUシリンジのデザインは、特に慢性疾患管理におけるコンプライアンスを促進し、自己投与が容易なことから在宅ヘルスケアでますます支持されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2023 |

| 予測年 | 2024-2032 |

| 開始金額 | 196億米ドル |

| 予測金額 | 491億米ドル |

| CAGR | 10.9% |

用途別では、低分子、診断薬、生物学的製剤に分類され、2023年のシェアは生物学的製剤が54.7%を占める。このセグメントの強みは、正確なデリバリー方法を必要とする慢性疾患や自己免疫疾患をターゲットとした生物学的製剤の需要が高まっていることに起因します。個別化医療へのシフトは、効率的な送達システムの必要性をさらに強調し、生物学的製剤の市場優位性を確固たるものにしています。

北米では米国がCAGR 10.6%でリードしており、これは高度なヘルスケア・インフラ、強力な研究開発努力、医療機器に対する高い需要に牽引されています。米国は技術革新に注力しており、患者の安全性と治療効果を高める安全設計やプレフィルドオプションなど、先進的なシリンジ技術が生み出されています。慢性疾患の増加やワクチン接種への取り組みが、市場の成長をさらに刺激しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患と高齢者人口の増加

- ワクチン接種イニシアチブの増加

- 患者の安全性に焦点を当てた技術の進歩

- 生物製剤およびバイオシミラーの研究活動の増加

- 業界の潜在的リスク&課題

- 針刺し損傷のリスクの高さ

- 厳しい規制要件

- 促進要因

- 成長可能性分析

- 規制状況

- 今後の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:プレパレーション別、2021年~2032年

- 主要動向

- すぐに使える(RTU)

- 滅菌準備済み(RTS)

第6章 市場推計・予測:用途別、2021年~2032年

- 主要動向

- 低分子医薬品

- 生物製剤

- 診断薬

第7章 市場推計・予測:材料別、2021年~2032年

- 主要動向

- ガラス

- プラスチック/ポリマー

第8章 市場推計・予測:サイズ別、2021年~2032年

- 主要動向

- 1 ml未満

- 1 ml-2 ml

- 3 ml-5 ml

- 6 ml-10 ml

- 10-20 ml

- 20-30 ml

- >30 ml

第9章 市場推計・予測:最終用途別、2021年~2032年

- 主要動向

- 病院・クリニック

- 製薬・バイオテクノロジー企業

- 開発・製造受託機関(CDMO)

- 診断ラボ

- その他エンドユーザー

第10章 市場推計・予測:地域別、2021年~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Becton, Dickinson and Company(BD)

- Cardinal Health

- Corning

- Daikyo Seiko

- DWK Life Sciences

- Gerresheimer AG

- ICU Medical

- Mitsubishi Gas Chemical Company

- Nipro

- SCHOTT Pharma(SCHOTT Group)

- Shandong Province Medicinal Glass

- SHIOTANI GLASS

- Terumo

- Weigao Group

- West Pharmaceutical Services

The Global Syringes Market was valued at USD 19.6 billion in 2023, with projections indicating a 10.9% CAGR from 2024 to 2032. Syringes, vital medical devices for fluid injection and withdrawal, consist of a barrel, plunger, and needle or nozzle for precise fluid control.

Growth in this market is driven by an aging population and an increase in chronic health conditions, which elevate the demand for safe, reliable injection devices. Additionally, the rise in home healthcare adoption supports syringe use as patients seek more convenient and affordable treatment solutions beyond clinical settings.

The market is segmented by preparation into ready-to-use (RTU) and ready-to-sterilize (RTS) syringes. The RTU segment leads the market, with an anticipated 11.1% CAGR, owing to its convenience for healthcare providers and patients. Often prefilled with medication, RTU syringes simplify administration, minimize dosage errors, and reduce contamination risk. Their design promotes compliance, particularly in chronic disease management, and is increasingly favored in home healthcare due to the ease of self-administration.

| Market Scope | |

|---|---|

| Start Year | 2023 |

| Forecast Year | 2024-2032 |

| Start Value | $19.6 Billion |

| Forecast Value | $49.1 Billion |

| CAGR | 10.9% |

By application, the market is categorized into small molecules, diagnostics, and biologics, with biologics holding a 54.7% share in 2023. This segment's strength stems from the growing demand for biologic drugs targeting chronic and autoimmune conditions, which require precise delivery methods. The shift toward personalized medicine further underscores the need for efficient delivery systems, solidifying biologics' market dominance.

In North America, the U.S. leads with a CAGR of 10.6%, driven by advanced healthcare infrastructure, strong R&D efforts, and high demand for medical devices. The U.S. focus on innovation has produced advanced syringe technologies, including safety-engineered and prefilled options that enhance patient safety and treatment effectiveness. Rising chronic diseases and vaccination initiatives further stimulate market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising chronic diseases and geriatric population

- 3.2.1.2 Increasing vaccination initiatives

- 3.2.1.3 Growing technology advancement focusing on patient safety

- 3.2.1.4 Rise in biologics and biosimilars research activities

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High risk of needlestick injuries

- 3.2.2.2 Stringent regulatory requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Preparation, 2021 - 2032 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Ready to use (RTU)

- 5.3 Ready to sterilize (RTS)

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2032 ($ Mn and Units)

- 6.1 Key trends

- 6.2 Small molecules

- 6.3 Biologics

- 6.4 Diagnostics

Chapter 7 Market Estimates and Forecast, By Material, 2021 - 2032 ($ Mn and Units)

- 7.1 Key trends

- 7.2 Glass

- 7.3 Plastic/ polymers

Chapter 8 Market Estimates and Forecast, By Size, 2021 - 2032 ($ Mn and Units)

- 8.1 Key trends

- 8.2 <1 ml

- 8.3 1 ml - 2 ml

- 8.4 3 ml - 5 ml

- 8.5 6 ml - 10 ml

- 8.6 10 - 20 ml

- 8.7 20 - 30 ml

- 8.8 >30 ml

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2032 ($ Mn and Units)

- 9.1 Key trends

- 9.2 Hospitals & clinics

- 9.3 Pharma & biotech companies

- 9.4 Contract development and manufacturing organizations (CDMOs)

- 9.5 Diagnostic laboratories

- 9.6 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2032 ($ Mn and Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Becton, Dickinson and Company (BD)

- 11.2 Cardinal Health

- 11.3 Corning

- 11.4 Daikyo Seiko

- 11.5 DWK Life Sciences

- 11.6 Gerresheimer AG

- 11.7 ICU Medical

- 11.8 Mitsubishi Gas Chemical Company

- 11.9 Nipro

- 11.10 SCHOTT Pharma (SCHOTT Group)

- 11.11 Shandong Province Medicinal Glass

- 11.12 SHIOTANI GLASS

- 11.13 Terumo

- 11.14 Weigao Group

- 11.15 West Pharmaceutical Services