|

市場調査レポート

商品コード

1833676

鉄鉱石ペレットの市場機会と成長促進要因、産業動向分析、2025年~2034年予測Iron Ore Pellets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 鉄鉱石ペレットの市場機会と成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年09月01日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

概要

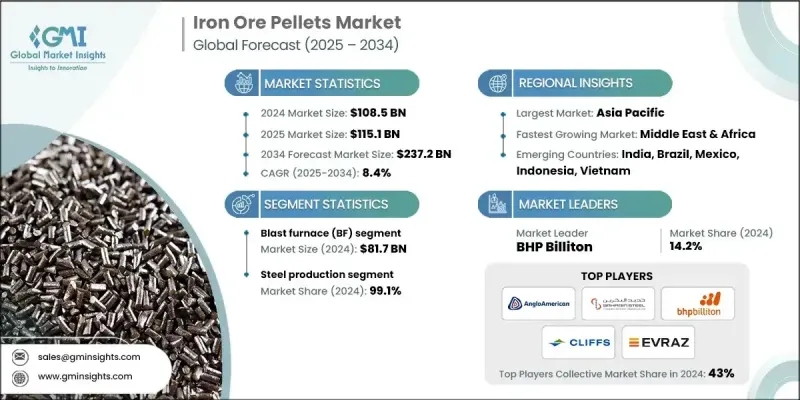

Global Market Insights Inc.が発行した最新レポートによると、鉄鉱石ペレットの世界市場は2024年に1,085億米ドルと推定され、CAGR 8.4%で2025年の1,151億米ドルから2034年には2,372億米ドルに成長すると予測されています。

鉄鉱石ペレットは、製鉄、特に高炉や直接還元鉄(DRI)プロセスにおいて重要な原料です。世界的なインフラプロジェクト、自動車生産、建設活動が拡大し続ける中、高品位鉄鉱石ペレットの需要も並行して高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 1,085億米ドル |

| 予測金額 | 2,372億米ドル |

| CAGR | 8.4% |

高炉(BF)の採用増加

高炉(BF)セグメントは、大規模製鉄事業における重要な役割に牽引され、2024年に注目すべきシェアを占めました。鉄鉱石ペレットは、一貫したサイズ、高鉄分、低ガングーレベルにより高炉プロセスで好まれ、炉効率を改善し、エネルギー消費を削減します。一貫製鉄所では、より厳しい排出基準を満たしながら生産性の向上を目指しており、高品質ペレットの需要は増加の一途をたどっています。

成長する鉄鋼生産

ペレットは冶金学的特性と炉効率の面で塊鉱や焼結鉱よりも優れた性能を発揮するため、鉄鋼生産セグメントは2024年に大きなシェアを獲得しました。ペレットの安定した品質は安定した生産を保証し、全体的な二酸化炭素排出量の削減に役立つため、従来の高炉と新興の直接還元鉄(DRI)プロセスの両方で不可欠となっています。

アジア太平洋が有利な地域となる

アジア太平洋鉄鉱石ペレット市場は、中国、インド、東南アジアの急速な工業化、都市開拓、大規模な鉄鋼生産能力によって後押しされ、2034年まで適正なCAGRで成長します。インフラ投資が急増し続け、環境規制が厳しくなるにつれて、この地域では持続可能な製鉄を支援するために高品位ペレットへの強いシフトが見られます。インドのような国々は、輸入焼結原料への依存を減らすために国内ペレット生産を拡大しています。この地域のプレーヤーは、生産能力を拡大し、選鉱とペレタイジング技術に投資し、合弁会社を設立して原料アクセスを確保し、増大する需要に効率的に対応しています。

鉄鉱石ペレット市場に参入している主な企業は、クリーブランド・クリフス、FERREXPO、METALLOINVEST、BHPビリトン、Jindal SAW、Evraz、LKAB Koncernkontor、Anglo American、Iron Ore Company of Canada、Bahrain Steelです。

業界各社は、その地位を強化するために、垂直統合、技術革新、戦略的パートナーシップを採用しています。その多くは、ペレットの品質を高め、資源利用を最適化するために、選鉱プラントや低品位鉱石処理に投資しています。採掘からペレット生産までの垂直統合は、より良いコスト管理と一貫した原料供給を可能にします。さらに、企業は低炭素ペレット製造プロセスに注力し、ESG目標に沿った持続可能性イニシアティブに取り組んでいます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場規模・予測:学年別、2021-2034

- 主要動向

- 高炉(BF)

- 直接還元(DR)

第6章 市場規模・予測:Balling Technologies社, 2021-2034

- 主要動向

- ボーリングディスク

- ボールドラム

第7章 市場規模・予測:用途別、2021-2034

- 主要動向

- 鉄鋼生産

- 鉄系化学物質

第8章 市場規模・予測:技術別、2021-2034

- 主要動向

- 電気アーク炉

- 電気誘導炉

- 酸素ベース/高炉

第9章 市場規模・予測:製品ソース別、2021-2034

- 主要動向

- ヘマタイト

- 磁鉄鉱

- その他

第10章 市場規模・予測:ペレット化プロセス別、2021-2034

- 主要動向

- トラベリンググレート(TG)

- 格子窯(GK)

- その他

第11章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東およびアフリカ

第12章 企業プロファイル

- Anglo American

- Bahrain Steel

- BHP Billiton

- Cleveland-Cliffs

- Evraz

- FERREXPO

- Iron Ore Company of Canada

- Jindal SAW

- LKAB Koncernkontor

- METALLOINVEST