自動車サイバーセキュリティの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Automotive Cybersecurity Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 345 Pages

- 納期

- 2~3営業日

- 商品コード

- 1822601

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

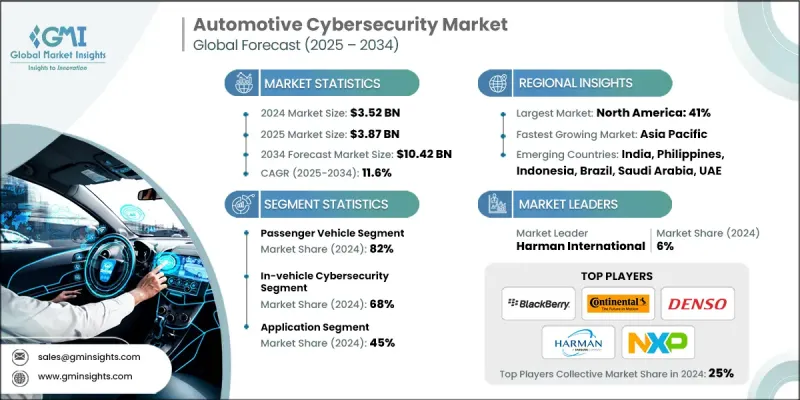

世界の自動車サイバーセキュリティ市場は2024年に35億2,000万米ドルと推定されました。

Global Market Insights Inc.が発行した最新レポートによると、同市場は2025年の38億7,000万米ドルから2034年には104億2,000万米ドルへとCAGR 11.6%で成長すると予測されています。

自動車がV2X(Vehicle-to-everything)通信や組み込みインフォテインメント・システムを介してますます接続されるようになるにつれて、ハッカーの攻撃対象は大幅に拡大しています。このため自動車メーカーは、リアルタイムのデータ交換、車両ネットワーク、デジタルシステムを保護するための強固なサイバーセキュリティ・ソリューションへの投資を迫られています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 35億2,000万米ドル |

| 予測金額 | 104億2,000万米ドル |

| CAGR | 11.6% |

乗用車の需要拡大

自動車サイバーセキュリティ市場の乗用車セグメントは、コネクテッドカー、インフォテインメントシステム、自律走行技術の急速な成長により、2024年に持続可能なシェアを維持した。消費者がよりスマートで安全な、よりデジタルな運転体験を期待する中、自動車メーカーは先進的なサイバーセキュリティプロトコルを乗用車に直接組み込むようになっています。

車載サイバーセキュリティの採用拡大

車載サイバーセキュリティ分野は、電子制御ユニット(ECU)、インフォテインメント・システム、テレマティクス、車両ネットワークを外部の脅威から保護することに重点が置かれており、2024年に大きなシェアを占めました。自動車がモバイル・コンピュータのように機能するようになっているため、車載サイバーセキュリティはリアルタイムの脅威検知、安全な通信、データの完全性を保証します。OEMは現在、ソフトウェア・ファイアウォール、侵入検知システム、暗号化を車両のハードウェアおよびソフトウェア・スタックに直接組み込み、ゼロからセキュリティを設計しています。

注目を集めるアプリケーション

自動車サイバーセキュリティ市場のアプリケーション・セグメントは、テレマティクスやインフォテインメントからADAS(先進運転支援システム)やパワートレイン制御まで、2024年に顕著な収益を上げました。最新の自動車では、車内のあらゆるデジタル・タッチポイントを保護する必要があります。車両アーキテクチャの複雑化に伴い、サイバーセキュリティ・アプリケーションは各システムに合わせて調整され、エンド・ツー・エンドの保護が確保されるようになっています。

有利な地域として台頭する北米

北米自動車サイバーセキュリティ市場は、強力な規制の後ろ盾、技術に精通した消費者、サイバーセキュリティと自動車の大手イノベーターの存在によって、2024年に力強い成長を維持した。米国では、モビリティ・ソリューションにサイバー耐性を組み込もうとしています。米国サイバーセキュリティ行政命令のような規制の枠組みや、データプライバシーに関する消費者の意識の高まりを受けて、自動車メーカーは堅牢な車載セキュリティシステムへの投資を加速させています。さらに、OEMと大手ハイテク企業との提携が、車両セキュリティ・プロトコルの新たなブレークスルーを後押ししています。

自動車サイバーセキュリティ市場の主要企業は、Karamba Security、Lear、Harman International、Denso、Upstream Security、NXP、Blackberry、Aptiv、Continental、Intertekです。

自動車サイバーセキュリティ市場の各社は、コネクテッドカーや自律走行車における新たな脅威に対応する最先端のセキュリティソリューションを開発するため、広範な研究開発を通じてイノベーションに注力しています。自動車メーカー、技術プロバイダー、規制機関との戦略的提携や協力関係により、製品の統合とコンプライアンスが加速しています。多くの企業が、車両の安全性を高めるため、リアルタイムの脅威検知システムやAI主導のサイバーセキュリティフレームワークに多額の投資を行っています。買収や合弁事業を通じて世界的な事業拠点を拡大することも、新たな市場や顧客セグメントを獲得するための一般的な戦術です。

目次

第1章 調査手法

- 調査デザイン

- 調査アプローチ

- データ収集方法

- GMI独自のAIシステム

- AIを活用した調査の強化

- ソース一貫性プロトコル

- AIの精度指標

- 基本推定と計算

- 基準年計算

- 予測モデル

- 市場予測の主な動向

- 定量化された市場影響分析

- 成長パラメータの予測に対する数学的影響

- シナリオ分析フレームワーク

- 1次調査と検証

- 一次情報の一部(ただしこれに限定されるわけではない)

- データマイニングソース

- 二次

- 有料ソース

- 公開情報源

- 地域別の情報源

- 二次

- 調査の軌跡と信頼度スコア

- 調査トレイルの構成要素:

- スコアリングコンポーネント

- 調査の透明性に関する補足

- ソースアトリビューションフレームワーク

- 品質保証指標

- 信頼へのコミットメント

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 自動車OEM

- サイバーセキュリティソリューションプロバイダー

- クラウドサービスプロバイダー

- ティア1サプライヤー

- テクノロジーインテグレーター

- 最終用途

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- サプライヤーの情勢

- 業界への影響要因

- 促進要因

- コネクテッドカーの導入拡大

- 自動車メーカーに対する厳格なサイバーセキュリティ規制

- 車両アーキテクチャの複雑化

- 無線アップデートの普及

- 業界の潜在的リスク&課題

- サイバーセキュリティソリューションの実装におけるコスト制約

- レガシーシステム統合

- 市場機会

- コネクテッドカーの普及拡大

- ソフトウェア定義車両への移行

- 規制の推進とコンプライアンス基準

- EVと自動運転車の拡大

- 促進要因

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 従来のセキュリティアプローチと限界

- 次世代セキュリティアーキテクチャ

- 自動車開発プロセスとの統合

- 新興技術

- 人工知能と機械学習のアプリケーション

- 行動分析と異常検出

- 安全な車両通信のためのブロックチェーン

- 量子コンピューティングが暗号に与える影響

- ゼロトラストセキュリティアーキテクチャ

- 自動車システム戦略の実装

- ネットワークセグメンテーションとマイクロセグメンテーション

- アイデンティティおよびアクセス管理(IAM)ソリューション

- ソフトウェア定義車両(SDV)のセキュリティ

- セキュリティバイデザインの原則

- 継続的なセキュリティ監視

- 動的セキュリティポリシー管理

- 将来の技術革新(2025-2034)

- 量子耐性暗号の実装

- 6Gネットワークのセキュリティ要件

- エッジコンピューティングのセキュリティ課題

- 自動運転車のセキュリティの進化

- 技術準備レベル(TRL)評価

- 現在の技術成熟度分析

- 商業化のタイムライン予測

- 投資要件とROI分析

- 現在の技術動向

- 特許分析

- 価格動向と経済分析

- コスト分析とROI評価

- サイバーセキュリティ投資分析

- CSMS導入コスト評価

- インシデントコスト影響分析

- 地域によるコストの違い

- コスト最適化戦略

- 財務リスク評価

- 脅威インテリジェンスと攻撃分析

- 現在の脅威情勢の評価

- 攻撃ベクトルの分類と分析

- 重大なシステムの脆弱性

- 高度な持続的脅威(APT)分析

- インシデント対応とフォレンジック機能

- 脅威インテリジェンスの共有と連携

- ユースケース

- 投資情勢と資金調達分析

- 費用便益分析

- 最良のシナリオ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 軽商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第6章 市場推計・予測:セキュリティ別、2021-2034

- 主要動向

- 応用

- ネットワーク

- 終点

第7章 市場推計・予測:展開モード別、2021-2034

- 主要動向

- クラウドベース

- オンプレミス

- ハイブリッド

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- ADASと安全性

- ボディコントロールと快適性

- インフォテインメント

- テレマティクス

- パワートレインシステム

- 通信システム

第9章 市場推計・予測:形態別、2021-2034

- 主要動向

- 車載サイバーセキュリティ

- 外部クラウドサイバーセキュリティ

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- フィリピン

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- グローバルプレーヤー

- Argus Cyber Security

- Blackberry

- Bosch

- BT Group

- Cisco Systems

- Continental

- Denso

- ESCRYPT

- Harman International

- Intel

- Irdeto Automotive

- Karamba Security

- Lear Corporation

- Microsoft

- NXP Semiconductors

- Symantec

- Trillium Secure

- Vector Informatik

- 地域プレーヤー

- Aptiv

- Eneos Cyber Solutions

- Intertek

- OneLayer

- SafeRide Technologies

- Tuxera Automotive

- 新興プレーヤー

- Arilou Technologies

- AutoCrypt

- GuardKnox

- Karamba Security

- Keen Security Lab

- Upstream Security

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 345 Pages

- 納期

- 2~3営業日