冠動脈ステント市場の機会、成長要因、業界動向分析、および2026年~2035年の予測

Coronary Stents Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1998699

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

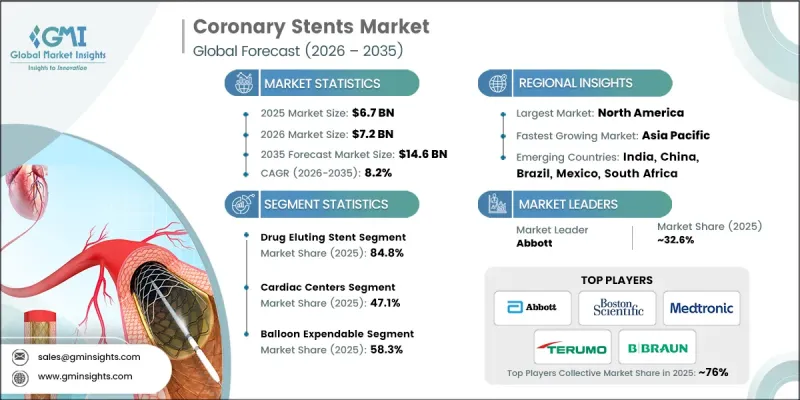

世界の冠動脈ステント市場は、2025年に67億米ドルと評価され、CAGR 8.2%で成長し、2035年までに146億米ドルに達すると推定されています。

市場の成長は、心血管疾患の有病率の上昇、高齢化、ステント技術の進歩、および低侵襲手術の普及拡大によって牽引されています。冠動脈ステントは、狭窄または閉塞した冠動脈に挿入される管状の医療機器であり、血管の開存性を維持し、血流を改善し、心筋梗塞を予防する役割を果たします。世界の主要な死因である冠動脈疾患の発生率の増加が、需要を後押ししています。薬剤溶出型ステント、生体吸収性スキャフォールド、ポリマーフリーステントなどの技術革新は、再狭窄や血栓症を最小限に抑えることで、長期的な治療成績を向上させています。患者の意識の高まり、臨床医の信頼感の向上、および血行再建術の拡大が、さらなる普及を後押ししています。薬剤溶出型ステントや生分解性ステントへの移行、患者中心のアプローチといった動向が、世界の業界の成長を形作っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026-2035 |

| 開始時の市場規模 | 67億米ドル |

| 予測額 | 146億米ドル |

| CAGR | 8.2% |

薬剤溶出型ステントセグメントは、再狭窄を最小限に抑え、患者の長期的な転帰を改善し、低侵襲治療を支援する能力により、2025年には84.8%のシェアを占めました。薬剤溶出型ステントは、過剰な組織増殖を防ぐために薬剤を放出するため、ベアメタルステントと比較して優れた長期的な結果をもたらし、これが臨床現場での広範な採用を後押ししています。

コバルト・クロム合金セグメントは、2035年までに75億米ドルに達すると予想されています。コバルト・クロム合金ステントは高い引張強度と耐久性を備えており、動脈圧下でも血管の拡張を維持しつつ、より薄いストラット設計を可能にします。これらの薄いストラットは、動脈への損傷を軽減し、血流を改善し、治癒を促進すると同時に、再狭窄や血栓症のリスクを最小限に抑えることで、セグメントの成長を牽引しています。

2025年時点で、北米の冠動脈ステント市場は39.6%のシェアを占めました。米国では、座りがちな生活習慣、高脂肪食、ストレスを要因として心血管疾患の負担が深刻化しており、これが冠動脈ステント留置術の需要を押し上げています。同地域における高度な医療インフラ、専門的な心臓センター、熟練した医療専門家の存在により、ステント留置術が広く利用可能となっています。病院やインターベンション心臓病センターにおける革新的なステント技術の導入が、同地域の成長をさらに後押ししています。

よくあるご質問

目次

第1章 調査手法

- 調査アプローチ

- 品質に関する取り組み

- GMI AIポリシーおよびデータ完全性に関する取り組み

- 情報源の一貫性に関するプロトコル

- GMI AIポリシーおよびデータ完全性に関する取り組み

- 調査の経緯と信頼度スコアリング

- 調査の経緯の構成要素

- スコアリングの構成要素

- データ収集

- 一次情報の一部リスト

- データマイニング情報源

- 有料情報源

- 地域別情報源

- 有料情報源

- 基本推定および算出方法

- 各アプローチにおける基準年の算出

- 予測モデル

- 定量化された市場影響分析

- 成長パラメータが予測に与える数学的影響

- 定量化された市場影響分析

- 調査の透明性に関する補足

- 情報源の帰属フレームワーク

- 品質保証指標

- 信頼への取り組み

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 冠動脈疾患の有病率の上昇

- 低侵襲手術への需要の高まり

- 発展途上国における技術の進歩

- 心臓疾患の予防ケアに対する認識と注目の高まり

- 業界の潜在的リスク&課題

- 製品の不具合およびリコール

- 厳格な規制承認

- 発展途上国における熟練した医療従事者の不足

- 市場機会

- 生体吸収性ステントおよび次世代ステントの開発

- デジタルヘルスと画像診断技術の統合

- 促進要因

- 成長可能性分析

- 規制状況(1次調査に基づく)

- 北米

- 欧州

- アジア太平洋地域

- 技術動向

- 現在の技術動向

- 新興技術

- 償還シナリオ(1次調査に基づく)

- 将来の市場動向

- 価格分析(2025年)(1次調査に基づく)

- ポーター分析

- PESTEL分析

- 顧客洞察(1次調査に基づく)

- スタートアップのシナリオ

- AIおよび生成AIが市場に与える影響

- 投資環境

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析(1次調査に基づく)

- 世界

- 北米

- 欧州

- アジア太平洋地域

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:製品別、2022-2035

- 薬剤溶出型ステント

- 生体吸収性血管スキャフォールド(BVS)

- ベアメタルステント

第6章 市場推計・予測:タイプ別、2022-2035

- バルーン式使い捨てステント

- 自己吸収型ステント

第7章 市場推計・予測:材料別、2022-2035

- コバルト・クロム合金

- ステンレス鋼

- その他の材料

第8章 市場推計・予測:最終用途別、2022-2035

- 心臓センター

- 病院

- 外来手術センター

- その他のエンドユーザー

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Abbott

- Andramed

- B. Braun

- Biosensors International Group

- Biotronik

- Boston Scientific

- Cook Medical

- Elixir Medical

- GENOSS

- Medtronic

- Meril Life Science

- MicroPort Scientific

- Sahajanand Laser Technology Limited

- Stryker

- Terumo

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日