|

市場調査レポート

商品コード

1892757

ツナ缶市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Canned Tuna Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| ツナ缶市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月09日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

概要

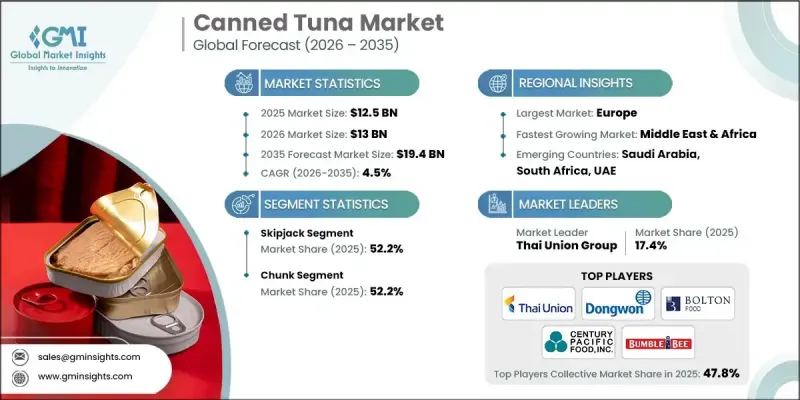

世界のツナ缶市場は、2025年に125億米ドルと評価され、2035年までにCAGR4.5%で成長し、194億米ドルに達すると予測されております。

ツナ缶は、マグロを油・水・塩水と共に缶詰にした保存食品であり、手軽で長期保存が可能なタンパク源としてご家庭で広くご利用いただいております。手頃な価格、栄養価の高さ、調理の簡便さから、世界中の家庭で定番商品となっております。高タンパク質食や健康的な食品への消費者関心の高まりが需要を後押ししており、缶詰マグロはフィットネス意識の高い方に理想的な低脂肪タンパク源を提供します。世界各国の政府や保健機関は、特に高齢者や健康志向の若い世代を対象にタンパク質摂取を推奨しており、缶詰マグロが総合的な健康維持や食事目標達成に果たす役割を強調しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 125億米ドル |

| 予測金額 | 194億米ドル |

| CAGR | 4.5% |

2024年時点で、カツオセグメントは52.2%のシェアを占めており、2035年までCAGR 4.6%で成長すると予測されています。その広範な入手可能性、低コスト、そしてマイルドな風味が、その優位性に寄与しています。熱帯海域ではカツオが豊富に供給されるため、製造業者の調達コストが削減され、競争力のある価格設定が可能となります。安定したサプライチェーンと、よりマイルドな味を好む消費者の嗜好が、その市場での地位をさらに強化しています。

チャンクマグロセグメントは2025年に52.2%のシェアを占め、その魅力的な食感と汎用性により引き続き主導的地位を維持しています。チャンクマグロは、サラダ、サンドイッチ、レディミールなどにおいて消費者と食品メーカー双方から支持されており、小売および外食産業チャネル全体で高い需要が見込まれる製品です。

北米のツナ缶市場は、2026年から2035年にかけてCAGR4.6%で拡大が見込まれており、米国単独でも2025年には30億米ドル規模に達すると予測されています。健康と持続可能性に対する消費者の意識の高まりが、責任ある調達方法による有機缶詰マグロの需要を牽引しています。メーカー各社は持続可能な漁獲を確保するため、選択的漁具の使用や船舶追跡技術の導入など、環境に配慮した漁業手法を採用しています。軽量化やリサイクル可能な素材を含む包装技術の革新は、環境意識の高い消費者への訴求力を高めると同時に、規制や業界の持続可能性基準を満たしています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- タンパク質摂取量の増加

- 食品産業の拡大

- 利便性動向がフレーバー製品とパウチ包装の普及を促進

- 業界の潜在的リスク&課題

- マグロの価格変動性

- 代替タンパク質からの競合

- 市場機会

- 即食可能なタンパク質製品の需要拡大

- 環境に配慮した包装への関心の高まり

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- タイプ別

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許状況

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントへの配慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:タイプ別、2022-2035

- 主要動向

- ビンナガマグロ

- カツオ

- キハダマグロ

- メバチマグロ

- クロマグロ

- トンゴル/ロングテール

- その他

第6章 市場推計・予測:製品形態別、2022-2035

- 主要動向

- 固形

- チャンク

- フレーク

- 燻製

- その他

第7章 市場推計・予測:容器タイプ別、2022-2035

- 主要動向

- 金属缶

- フレキシブルパウチ(レトルトパウチ)

- ガラス瓶

- その他

第8章 市場推計・予測:最終用途別、2022-2035

- 主要動向

- 小売・家庭消費

- 外食産業(レストラン、ホテル、ケータリング)

- 機関向け(学校、病院、軍隊、企業)

- 食品加工・製造

- ペットフード

- その他

第9章 市場推計・予測:流通チャネル別、2022-2035

- 主要動向

- 量販店(スーパーマーケット、ハイパーマーケット、倉庫型会員制店)

- コンビニエンスストア

- オンライン小売・電子商取引

- 専門店・健康食品店

- 外食産業向け卸売業者

- 輸出・国際流通業者

- その他

第10章 市場推計・予測:地域別、2022-2035

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第11章 企業プロファイル

- American Tuna

- Bumble Bee Foods

- Century Pacific Food

- Crown Prince

- Dongwon Group

- Nauterra

- Princes Food

- Safe Catch

- StarKist Co.

- Thai Union Group

- Wild Planet Foods