養殖用ワクチン市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測

Aquaculture Vaccines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035- 発行日

- ページ情報

- 英文 134 Pages

- 納期

- 2~3営業日

- 商品コード

- 1959621

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

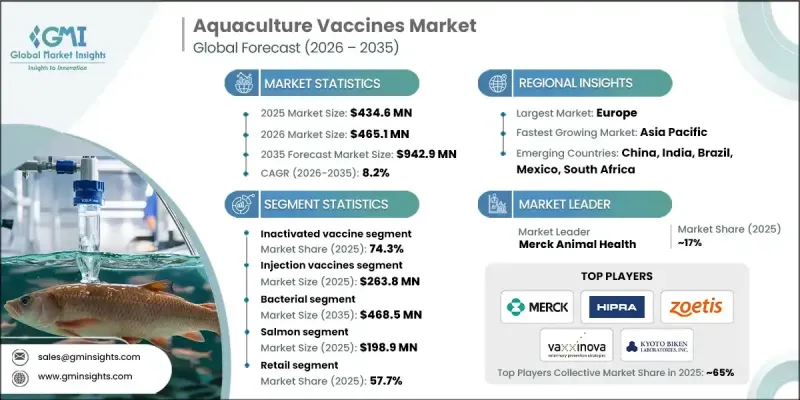

世界の水産養殖用ワクチン市場は、2025年に4億3,460万米ドルと評価され、2035年までにCAGR8.2%で成長し、9億4,290万米ドルに達すると予測されています。

市場成長は、世界の水産養殖生産の拡大と魚類需要の高まりによって牽引されています。ビブリオ菌、エアロモナス菌、その他の病原体による感染症を含む細菌・ウイルス感染症の頻発により、死亡率を低減し生産性を向上させるワクチンの必要性が高まっています。水産養殖用ワクチンは、魚類や甲殻類などの水生動物の免疫系を刺激し、特定の病原体に対する抵抗性を提供する生物学的製剤です。注射、浸漬、経口投与などの経路で投与されるこれらのワクチンは、疾病発生の最小化、抗生物質使用量の削減、持続可能な養殖業の促進に貢献します。アジア太平洋地域やラテンアメリカを中心とした新興市場が成長に寄与しているほか、経口・浸漬ワクチン投与技術の研究開発投資も増加しています。製造業者と養殖企業との連携により、革新的なソリューションの迅速な商業化と広範な普及が可能となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 4億3,460万米ドル |

| 予測金額 | 9億4,290万米ドル |

| CAGR | 8.2% |

不活化ワクチンセグメントは74.3%のシェアを占め、2035年までCAGR8.1%で成長すると予測されています。その安全性、広範囲な保護効果、安定性により、生産者の間で非常に好まれています。これらのワクチンは様々な養殖種に広く使用され、病原性への逆戻りのリスクなく一貫した免疫応答を提供します。注射剤や浸漬剤など複数の投与形態が利用可能であり、運用上の柔軟性を提供します。非生ワクチン製剤を推奨する規制基準、抗生物質不使用水産物に対する消費者需要の増加、集約的養殖システムにおけるバイオセキュリティへの注力が、その採用をさらに後押ししています。

注射ワクチン分野は2025年に2億6,380万米ドルの市場規模を記録し、2035年までCAGR8.1%で拡大が見込まれます。注射ワクチンは魚類に正確な投与量を直接投与することで優れた有効性と持続的な免疫を提供し、細菌性・ウイルス性病原体に対する最適な防御を保証します。自動ワクチン接種システムや人間工学に基づいた装置の革新により、投与が簡素化され、動物へのストレスが軽減され、孵化場や育成養殖場全体での業務効率が向上しました。

欧州水産養殖ワクチン市場は、先進的な水産養殖産業、疾病予防に対する強力な規制重視、ワクチンプログラムの早期導入により、2025年に43%のシェアを占めました。予防的抗生物質使用に対する規制上の制限がワクチンへの移行を加速させており、確立されたコールドチェーン流通ネットワーク、熟練した獣医サポート、主要ワクチンメーカーの存在が持続的な成長に寄与しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 細菌性・ウイルス性感染症の急増

- 世界の水産養殖生産量の増加

- 新規水産養殖用ワクチンの開発と発売

- 抗生物質に代わる養殖用ワクチンの採用拡大養殖用ワクチンの採用拡大

- 業界の潜在的リスク&課題

- 小規模養殖業者における認知度の低さ

- 複雑なワクチン開発手順

- 市場機会

- 経口および浸漬型ワクチンの登場

- 水産養殖投資が増加する新興市場への進出

- 促進要因

- 成長可能性分析

- 技術動向

- 現在の技術動向

- 新興技術

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- パイプライン分析

- 今後の市場動向

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携および協力関係

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:ワクチン種類別、2022-2035

- 不活化ワクチン

- 弱毒生ワクチン

- サブユニットワクチン

- その他のワクチンタイプ

第6章 市場推計・予測:投与経路別、2022-2035

- 注射ワクチン

- 経口ワクチン

- 浸漬および噴霧

第7章 市場推計・予測:用途別、2022-2035

- 細菌性

- ウイルス性

- 寄生虫

- 複合

第8章 市場推計・予測:タイプ別、2022-2035

- サーモン

- マス

- ティラピア

- スズキ

- 鯛

- ヒラメ

- コイ

- その他の魚種

第9章 市場推計・予測:流通チャネル別、2022-2035

- 小売り

- 電子商取引

- 動物病院/動物診療所付属薬局

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ノルウェー

- アイルランド

- トルコ

- デンマーク

- アジア太平洋地域

- 中国

- インド

- インドネシア

- フィリピン

- ベトナム

- オーストラリア

- ニュージーランド

- ラテンアメリカ

- ブラジル

- メキシコ

- チリ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Cavac

- CIBA

- HIPRA

- Kemin Industries

- Kyoritsu Seiyaku

- Kyoto Biken Laboratories

- Merck Animal Health

- Nisseiken

- Phibro Animal Health

- Tecnovax

- Vaxxinova International

- Veterquimica

- Virbac

- Zoetis

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 134 Pages

- 納期

- 2~3営業日