|

市場調査レポート

商品コード

1844370

左心房付属器閉鎖装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Left Atrial Appendage Closure Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 左心房付属器閉鎖装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年09月18日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

概要

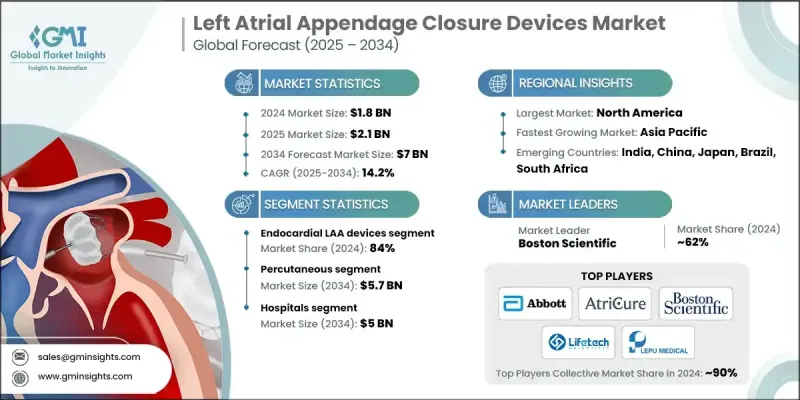

世界の左心房付属器閉鎖装置市場は2024年に18億米ドルと評価され、CAGR 14.2%で成長し、2034年には70億米ドルに達すると推定されています。

市場拡大の背景には、心房細動の罹患率の上昇、低侵襲な心血管系処置への嗜好の高まり、ヘルスケアシステム全体における償還政策の範囲の拡大があります。LAA閉鎖デバイスは、非弁膜症性心房細動と診断された患者において、血栓形成の一般的な部位である左心房付属器を閉鎖することで、脳卒中リスクを低減するために使用されます。心房細動が、特に高齢者層でより一般的になるにつれて、こうした脳卒中予防ソリューションへの需要が高まっています。世界中の政府は、心房細動に関連する合併症に関連する長期的なヘルスケアコストを軽減するために、心血管治療への投資を増やしています。また、増加する資金は、一般市民の意識向上キャンペーンや、次世代閉鎖装置を含むより高度な治療技術の研究を支援しています。早期診断と革新的なデバイスベースの治療オプションの重視により、LAA閉鎖デバイス産業は世界規模で有望な展望を形成しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 18億米ドル |

| 予測金額 | 70億米ドル |

| CAGR | 14.2% |

2024年、心内膜型LAA閉鎖装置セグメントのシェアは84%。これらのデバイスは、強力な臨床試験の実績、医師からの幅広い信頼、実世界での応用の成功に裏打ちされた低侵襲アプローチで広く選ばれています。そのデザインにより、医師はカテーテルを用いた手技でLAAを封鎖し、開心術を必要とせずに心房細動患者の脳卒中リスクを低下させることができます。この分野は、回復に要する時間が短く、長期的な転帰が証明された手技に対する需要の高まりから、引き続き恩恵を受ける。

経皮的セグメントは、その適応性とインターベンショナル・カーディオロジー・インフラストラクチャーの利用可能性の拡大により、2034年までに57億米ドルに達すると予測されています。この方法は、経験豊富な臨床医と最新のカテ室技術に支えられ、病院や心臓治療センターなどさまざまな環境で手技を実施できます。そのアクセスのしやすさと手技の安全性の広さが、この市場における支配的な手技としての地位を確固たるものにしています。

北米左心房付属器閉鎖装置2024年のシェアは46.2%。同地域は、高度なヘルスケア・インフラ、強固な研究開発、一貫した臨床試験活動に支えられた心臓構造治療のイノベーションにおけるリーダーです。高度に専門化された医療センターが存在し、心臓手技のトレーニングへのアクセスが広がっていることが、手技の成長を支えています。さらに、AIを活用した術前計画やデジタル監視ツールなどの技術的進歩が、LAA閉鎖分野における北米のリーダーシップをさらに強化しています。

左心房付属器閉鎖装置市場で積極的に競合している著名企業には、MicroPort、Medtronic、LEPU MEDICAL、Abbott、AtriCure、Boston Scientific、Lifetechなどがあります。左心房付属器閉鎖装置市場に参入している企業は、足場を固めるために戦略的な取り組みを実施しています。その多くは、移植の容易さ、手技の安全性、長期的な有効性を向上させる次世代デバイスを開発するため、研究開発に多額の投資を行っています。企業は、より迅速な規制当局の承認を得て臨床検証を強化するため、臨床試験パイプラインを拡大しています。病院や研究センターとの戦略的提携は、実地研修やデータ共有を通じて医師の採用を拡大するために進められています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 心房細動の有病率の増加

- 技術的進歩

- 低侵襲手術の導入増加

- 償還対象範囲の拡大

- 業界の潜在的リスク&課題

- 手続きコストが高め

- 合併症のリスク

- 市場機会

- 新興市場への進出

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術的情勢

- 現在の技術

- 新興技術

- 将来の市場動向

- 払い戻しシナリオ

- パイプライン分析

- 投資情勢

- 価格分析、2024

- ポーターの分析

- PESTEL分析

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ・中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 心内膜LAAデバイス

- 心外膜LAAデバイス

第6章 市場推計・予測:手順別、2021-2034

- 主要動向

- 経皮的

- 外科手術

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 外来手術センター

- その他の用途

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott

- AtriCure

- Boston Scientific

- LEPU MEDICAL

- Lifetech

- Medtronic

- MicroPort