|

市場調査レポート

商品コード

1928996

電気推進衛星市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Electric Propulsion Satellites Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 電気推進衛星市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月15日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

概要

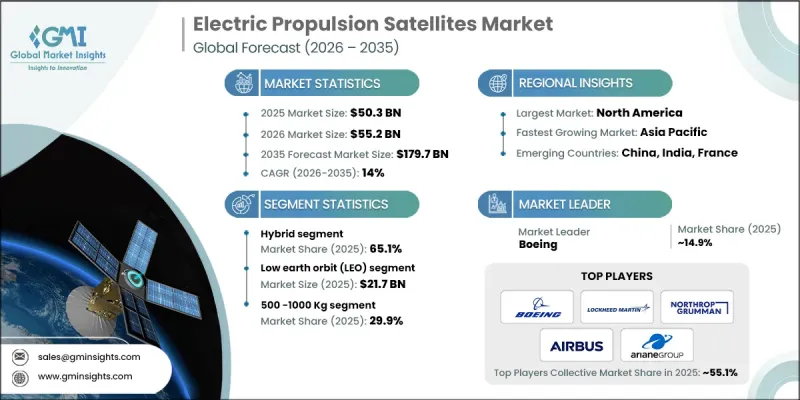

世界の電気推進衛星市場は、2025年に503億米ドルと評価され、2035年までにCAGR 14%で成長し、1,797億米ドルに達すると予測されています。

市場成長は、大規模衛星コンステレーションへの需要加速、電気推進効率の継続的向上、コスト最適化された打ち上げ・軌道上運用ソリューションへの選好高まりによって支えられています。通信・観測・保安目的の衛星配備増加は、ミッション寿命延長と運用コスト削減を実現する推進システムの必要性を強めています。電気推進技術の進歩は推力効率と運用柔軟性を高め、衛星がより少ない燃料質量で複雑なミッションを遂行することを可能にしています。環境に配慮した宇宙運用への関心の高まりも、よりクリーンな推進システムの採用を促進しております。商業宇宙エコシステムの拡大と、官民双方の利害関係者の参加増加が相まって、需要をさらに刺激しております。衛星プログラム全体においてコスト効率は依然として重要な優先事項であり、性能・拡張性・長期ミッション経済性をバランスさせる推進アーキテクチャへの関心を高め、持続的な市場拡大を支えております。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 503億米ドル |

| 予測金額 | 1,797億米ドル |

| CAGR | 14% |

ハイブリッド推進セグメントは2025年に65.1%のシェアを占めました。このセグメントは、多様なミッション要件を満たすために電気推進システムと化学推進システムを組み合わせることで利点を得ています。衛星運用事業者が、機動性と耐久性の両方をサポートしつつコスト効率を維持する信頼性の高い推進ソリューションを求める中、ハイブリッド構成への需要は引き続き増加しています。

低軌道(LEO)セグメントは2025年に217億米ドルの市場規模を生み出しました。頻繁な展開を必要とする大規模コンステレーションへの適合性、効率的な推進性能、幅広いアプリケーションにおける信頼性の高い運用カバレッジにより、LEO衛星への強い需要が牽引されています。

北米の電気推進衛星市場は2025年に36.7%のシェアを占めました。同地域の市場リーダーシップは、衛星技術への持続的な投資、先進的な通信インフラへの強い需要、そして官民資金による推進技術革新の継続的な開発によって支えられています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 世界衛星コンステレーションに対する需要の高まり

- 電気推進技術の効率性における進展

- 手頃な価格の打ち上げソリューションに対する需要の増加

- 防衛・商業分野における宇宙打ち上げの急増

- 宇宙インフラ開発への投資増加

- 業界の潜在的リスク&課題

- 初期開発および導入コストの高さ

- 技術的制約と性能上の懸念

- 市場機会

- 持続可能な宇宙技術に対する需要の増加

- 衛星部品の小型化における進展

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 新興ビジネスモデル

- コンプライアンス要件

- 防衛予算分析

- 世界の防衛支出動向

- 地域別防衛予算配分

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- サプライチェーンのレジリエンス

- 地政学的分析

- 労働力分析

- デジタルトランスフォーメーション

- 合併、買収、および戦略的提携の動向

- リスク評価と管理

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 市場集中度分析

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオ比較

- 製品ラインの広さ

- 技術

- イノベーション

- 地理的プレゼンス比較

- 世界展開分析

- サービスネットワークのカバー率

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー企業

- 課題者

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績比較

- 主な発展

- 合併・買収

- 提携および協業

- 技術的進歩

- 拡大と投資戦略

- サステナビリティへの取り組み

- デジタルトランスフォーメーションの取り組み

- 新興/スタートアップ競合の動向

第5章 市場推計・予測:軌道別、2022-2035

- 低軌道(LEO)

- 中軌道(MEO)

- 静止軌道(GEO)

第6章 市場推計・予測:衛星タイプ別、2022-2035

- 完全電気式

- ハイブリッド

第7章 市場推計・予測:衛星質量別、2022-2035

- 100kg未満

- 100~500 kg

- 500~1000 kg

- 1000kg超

第8章 市場推計・予測:推進力別、2022-2035

- 電気熱式

- 静電式

- 電磁式

- その他

第9章 市場推計・予測:用途別、2022-2035

- 地球観測

- 航法

- 通信

- 気象監視

- その他

第10章 市場推計・予測:最終用途別、2022-2035

- 政府

- 軍事

- その他

- 商業用

第11章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- 世界の主要企業

- Boeing

- Lockheed Martin

- Northrop Grumman

- Airbus

- ArianeGroup

- 地域別主要企業

- 北米

- Aerojet Rocketdyne

- Busek Co. Inc.

- L3Harris Technologies

- アジア太平洋地域

- Bellatrix Aerospace

- 欧州

- OHB System

- Safran Group

- Sitael Spa

- Thales Alenia Space

- ThrustMe

- 北米

- ニッチプレーヤー/ディスラプター

- Accion Systems Inc.

- Ad Astra Rocket