|

市場調査レポート

商品コード

1982318

顕微手術用ロボットの市場機会、成長要因、業界動向分析、および2026年~2035年の予測Microsurgery Robot Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 顕微手術用ロボットの市場機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年02月25日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

概要

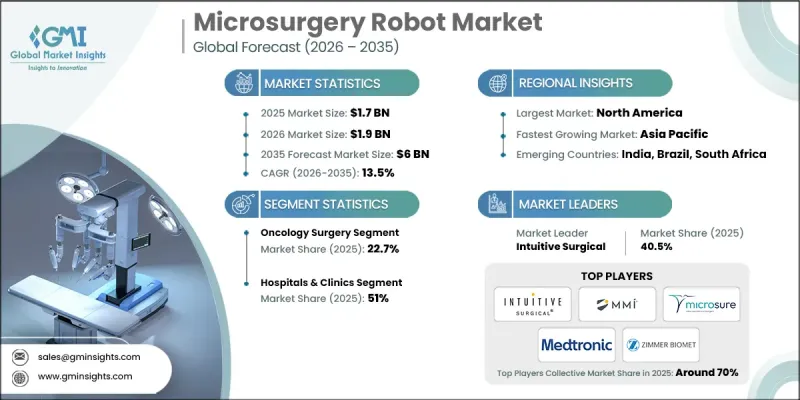

世界のマイクロサージェリーロボット市場は、2025年に17億米ドルと評価され、2035年までにCAGR 13.5%で成長し、60億米ドルに達すると推定されています。

市場の拡大は、低侵襲手術技術への需要の高まり、ロボット支援プラットフォームの急速な技術革新、および精密な外科的介入を必要とする慢性疾患の増加によって牽引されています。先進国における高度なロボット開発への財政支援の増加と、外科医の研修プログラムの拡充が相まって、導入率が向上しています。継続的な研究開発投資、医療技術(MedTech)分野での連携、そしてより手頃な価格のロボットシステムの導入が、商業化のプロセスをさらに加速させています。世界中の医療提供者は、外傷の軽減、回復期間の短縮、合併症リスクの低減、患者満足度の向上といった臨床的利点から、低侵襲アプローチへと移行しています。また、病院は手術の精度向上、複雑な処置の標準化、長期的な治療成果の最適化を図るため、ロボット技術の導入を優先しており、マイクロサージェリーロボットは現代の手術環境における変革的なソリューションとして位置づけられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 17億米ドル |

| 予測額 | 60億米ドル |

| CAGR | 13.5% |

外科的治療を必要とする慢性疾患の世界の負担の増大は、ロボット支援マイクロサージェリーシステムへの需要を引き続き牽引しています。複数の専門分野にわたる複雑な手術において、ロボットプラットフォームがもたらす操作性の向上、手振れの低減、および拡大された視認性が役立っています。手術の複雑さが増すにつれ、ロボット技術は精度、一貫性、および手術全体の効率性を向上させるために活用されており、先進的な医療提供システムにおけるその役割を強化しています。

泌尿器科手術セグメントは、2025年に3億5,230万米ドルの市場規模を記録しました。このセグメントは、同専門分野におけるロボットシステムの早期導入と、日常的な手術ワークフローへの継続的な統合により、依然として大きな貢献を果たしています。成長の原動力としては、発展途上地域への拡大、技術的に高度な手術での利用増加、および手術のパフォーマンス向上を目的とした手術種別専用ロボットプラットフォームの導入が挙げられます。

2025年、病院およびクリニックセグメントは51%のシェアを占めました。大規模な三次医療機関や大学病院が導入の大部分を占めており、多くの場合、多様な外科分野にわたって複数のロボットシステムを運用しています。これらの施設は、高い手術件数、体系化されたトレーニング体制、支援的な償還枠組み、そして先進技術の導入に必要な資金力といった利点を享受しています。

2025年の米国の顕微手術用ロボット市場規模は8億9,880万米ドルと評価されました。専門的な外科手術件数の増加が、市場の継続的な拡大を後押しすると予想されます。米国は、高度な医療インフラ、公的・民間保険者による有利な償還支援、イノベーションを促進する明確な規制プロセス、専門分野を横断した強い手術需要、そして包括的な外科医教育プログラムにより、市場をリードし続けています。

よくあるご質問

目次

第1章 調査手法

- 調査アプローチ

- 品質に関する取り組み

- GMI AIポリシーおよびデータ完全性への取り組み

- 情報源の一貫性プロトコル

- GMI AIポリシーおよびデータ完全性への取り組み

- 調査の経緯と信頼度スコアリング

- 調査トレイルの構成要素

- スコアリングの構成要素

- データ収集

- 一次情報の一部リスト

- データマイニング情報源

- 有料情報源

- 地域別情報源

- 有料情報源

- 基本推定および算出方法

- 基準年の算出

- 予測モデル

- 定量化された市場影響分析

- 成長パラメータが予測に与える数学的影響

- 定量化された市場影響分析

- 調査の透明性に関する補足

- 情報源帰属フレームワーク

- 品質保証指標

- 信頼への取り組み

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 低侵襲手術に対する需要の高まり

- 技術的進歩

- 慢性疾患の罹患率の増加

- 先進国におけるマイクロサージェリー用ロボットの開発資金の増加

- 業界の潜在的リスク&課題

- ロボットシステムに伴う高コスト

- 熟練した医療従事者の不足

- 機会

- 予測手術に向けたAIおよび機械学習との統合

- 精密な処置のためのロボット手術器具の小型化

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格分析

- 償還シナリオ

- スタートアップの動向

- 政策の展望

- ポーターの分析

- PESTEL分析

- ギャップ分析

- 将来の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:用途別、2022-2035

- 腫瘍外科

- 泌尿器科手術

- 産婦人科手術

- 微小吻合

- 再建外科

- 耳鼻咽喉科手術

- 消化器外科

- 心臓血管外科

- 尿管腎鏡検査

- 神経血管外科

- 眼科手術

- その他の用途

第6章 市場推計・予測:最終用途別、2022-2035

- 病院および診療所

- 外来手術センター

- 研究機関

- その他のエンドユーザー

第7章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- ASENSUS SURGICAL

- CMR Surgical

- Distalmotion

- Intuitive Surgical

- Medical Micro Instruments(MMI)

- Medtronic

- meerecompany

- MicroSure

- Preceyes

- Siemens Healthineers

- Zimmer Biomet