|

市場調査レポート

商品コード

1858983

脳磁図の市場機会、成長促進要因、産業動向分析、2025~2034年予測Magnetoencephalography Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 脳磁図の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年10月09日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

概要

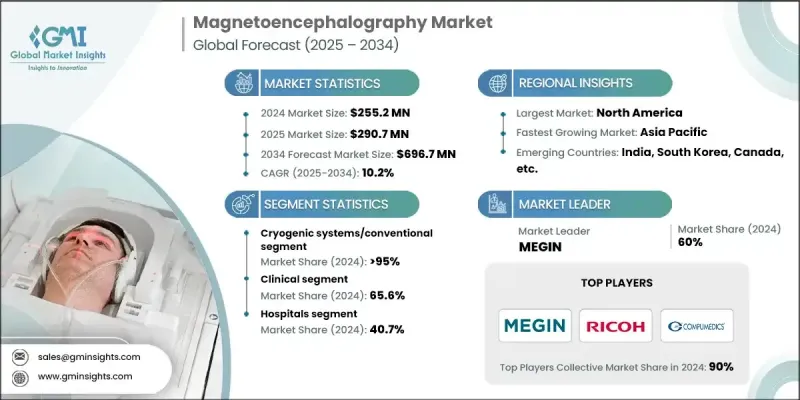

脳磁図の世界市場は、2024年に2億5,520万米ドルと評価され、CAGR 10.2%で成長し、2034年には6億9,670万米ドルに達すると予測されています。

脳磁図(MEG)の需要は、神経疾患の発生率の上昇、人口の高齢化、高度な診断ツールへの依存度の増加により加速しています。臨床機関や研究機関では、神経学的評価の精度とスピードを高めるためにMEGの導入が進んでいます。脳活動をリアルタイムで追跡できるこの技術は、てんかん、アルツハイマー病、パーキンソン病などの診断や管理に不可欠なものとなっています。臨床での使用に加え、MEGシステムは脳機能研究、精神医学的評価、神経発達研究などにも広く応用されています。技術の進歩と脳ネットワーク接続のより深い理解が、ヘルスケアエコシステム全体の革新と統合を引き続き促進しています。特に先進地域では、ヘルスケアのインフラが整備され、神経科学への取り組みに対する資金援助が充実しているため、採用が進んでいます。メーカー各社は、特に新興市場において、流通戦略の強化と低コストモデルを通じてMEGシステムへのアクセス拡大に取り組んでいます。個別化治療や早期診断への動向の高まりは、脳磁図システムの世界的な長期的市場需要をさらに促進すると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 2億5,520万米ドル |

| 予測金額 | 6億9,670万米ドル |

| CAGR | 10.2% |

OPMシステム分野は、2034年までCAGR 24.9%で成長し、ニューロイメージングにおける革新的な進歩としての地位を確立します。これらのシステムは、室温で効率的に動作する光ポンプ磁力計を使用して構築されており、複雑な極低温コンポーネントは不要です。そのコンパクトなウェアラブル・フォーマットにより、センサーを頭皮に直接配置することができ、空間分解能が向上し、自然な動作中にデータを取得することができます。OPMベースのMEGシステムは、柔軟性、運用コストの低さ、実環境への適応性から、小児用や外来モニタリングに特に魅力的です。その拡張性と可搬性は、臨床現場と神経科学研究センターの両方で支持され続けています。

2024年、臨床分野のシェアは65.6%でした。神経障害を患う患者数の増加と早期診断への重点化が、このセグメントの優位性に寄与しています。MEGは、異常な脳活動を正確に特定することで、手術前のマッピングや疾患管理において重要な役割を果たしています。その非侵襲的で高解像度の能力は、正確なマッピングが手術計画と患者の転帰に極めて重要であるてんかん、腫瘍、変性神経疾患の治療に特に有用です。

北米脳磁図市場は2024年に39.5%のシェアを占める。同地域は、医学研究における強固な基盤、広範なヘルスケアへのアクセス、脳関連疾患と診断される患者数の増加などの恩恵を受けています。MEGの早期臨床導入と病院診療への統合は、診断への応用拡大に役立っています。地域政府も神経科学プロジェクトに資金を提供し、脳マッピング研究イニシアチブを支援することで、重要な役割を果たしています。これらの要因により、北米はMEGシステムを使用した技術展開と臨床結果の両方においてフロントランナーとして位置づけられています。

世界の脳磁図市場で活動している主要企業には、FieldLine Inc.、リコー、Cerca Magnetics Limited、Compumedics Limited、MAG4Health、MEGIN、CTF MEG NEURO INNOVATIONS, INC.などがあります。脳磁図分野の企業は、研究開発への戦略的投資とグローバル展開を通じて市場での地位を強化しています。イノベーションは、モビリティとアクセシビリティを向上させるOPMベースのソリューションのような次世代MEGシステムに重点を置き、中心であり続けています。企業は、新興市場での設置やサービス・インフラを改善することにより、地理的に拡大しています。研究機関や病院との協力関係は、臨床検証や製品採用を加速させるのに役立っています。さらに、システム統合を簡素化し、操作の複雑さを軽減する努力がなされており、MEGを日常的な臨床使用にとってより現実的なものにしています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 神経疾患の有病率の増加

- 脳磁図分野における急速な技術進歩

- 臨床診断と研究におけるアプリケーションの成長

- 業界の潜在的リスク&課題

- 代替神経画像技術の利用可能性

- 脳磁図システムの高コスト

- 機会

- ポータブル&ウェアラブルMEGシステム

- AI統合&自動分析

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- 技術ロードマップとイノベーションの展望

- SQUIDテクノロジーの進化

- OPM技術の進歩

- 量子センサー開発

- AI/ML統合スケジュール

- 価格分析、地域別2024

- fMRIやEEGに対するMEGの利点

- パイプライン分析

- 世界のMEG設置数,地域別・国別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- アジア太平洋地域

- 中国

- 日本

- 北米

- ブランド分析

- 償還シナリオ

- ポーター分析

- PESTEL分析

- 今後の市場動向

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- グローバル

- 北米

- 欧州

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

- 主な発展

- 合併・買収

- パートナーシップ

- 新製品発表

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 極低温システム/従来型

- OPMシステム

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 臨床

- てんかん

- 自閉症

- 認知症

- 脳卒中

- 外傷性脳損傷(TBI)

- その他の用途

- 研究

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- イメージングセンター

- 学術研究機関

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- アジア太平洋地域

- 中国

- 日本

- 世界のその他の地域(RoW)

第9章 企業プロファイル

- Cerca Magnetics Limited

- Compumedics Limited

- CTF MEG NEURO INNOVATIONS, INC.

- FieldLine Inc.

- MAG4Health

- MEGIN

- Ricoh