|

市場調査レポート

商品コード

1755357

白色セメント市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年)White Cement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 白色セメント市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年) |

|

出版日: 2025年05月21日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

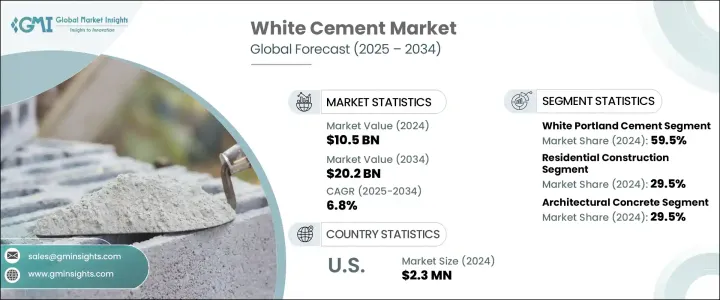

世界の白色セメントの市場規模は、2024年に105億米ドルとなり、世界のインフラ開拓の急増により、CAGR 6.8%で成長し、2034年には202億米ドルに達すると予測されています。

都市化が急速に進む中、各国政府は道路、橋梁、公共建築物の建設に多額の投資を行っており、白色セメントのような高品質で見た目も美しい建材への需要が高まっています。

持続可能性は、白色セメント市場を前進させるもう一つの重要な要因となっています。白色セメントの熱反射特性は、エネルギー効率の高い建築に最適であり、環境に優しい建材への需要の高まりと一致しています。建築家や建設業者が二酸化炭素排出量の削減を目指す中、白色セメントは省エネルギーと環境維持に貢献することから、建設業界で好まれる材料として位置づけられています。進化する市場ニーズに応えるため、各メーカーは白色セメントの新しい配合を導入し、強度の向上や硬化時間の短縮など、より優れた性能特性を提供しています。このような技術革新により、白色セメントの用途は拡大し、大規模な建設プロジェクトにおいて、より実行可能で費用対効果の高いものとなっています。都市の成長機会が続き、建設動向が進化するにつれて、同市場はその勢いを維持し、建築材料分野の既存企業や新規参入企業に大きな機会を提供すると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025~2034年 |

| 当初の市場規模 | 105億米ドル |

| 市場規模予測 | 202億米ドル |

| CAGR | 6.8% |

2024年には、白色ポルトランドセメントが59.5%のシェアを占める。白色ポルトランドセメントは、その高い強度、優れた仕上がり、美観により、最も広く使用されています。白色ポルトランドセメントは、壁、床、彫刻など、色や明るさの均一性が重要な建築・装飾用途で主に使用されています。この分野の需要は、高級建築プロジェクトの開発が進み、住宅や商業空間において視覚に訴える構造を好む傾向が強まっていることが大きな要因となっています。

2024年の住宅建設分野の市場シェアは29.5%です。白色セメントは、その卓越した仕上げ、耐久性、美的価値により、住宅建設で非常に好まれ、内外の壁、床材、装飾要素に人気のある選択肢となっています。都市化と人口増加に後押しされた住宅需要の高まりが、この分野の成長の重要な要因となっています。住宅所有者がエレガントで長持ちする素材を求める中、白色セメントは高級で長持ちする住宅空間を作るための好ましい選択肢となっています。

米国の白色セメント市場は2024年に230万米ドルで85%のシェアを占めました。同国の白色セメント消費は、建設活動の拡大、技術の進歩、持続可能な建築慣行への強い関心に牽引され、急成長を遂げるとみられています。耐久性と美観に優れた建材への高い需要が、インフラ開発の急増と相まって、米国の白色セメント消費を大幅に押し上げています。

J.K.セメント、Aalborg Portland、UltraTech Cement、Cemex、Cimsaなどの主要企業は、これらの戦略を駆使して白色セメントの需要増に対応し、競争の激しい市場で優位に立とうとしています。白色セメント市場の企業は、存在感を高め、市場での地位を強化するために、いくつかの重要な戦略を実施しています。製品のイノベーション、生産能力の拡大、戦略的パートナーシップの構築などです。高強度配合、美観仕上げ、持続可能性など、特定のニーズに対応する特殊な白色セメントを開発することで、各社は住宅と商業の両部門からの高まる需要に確実に応えています。生産効率と品質を向上させる最先端技術への投資もまた、重要な戦略です。これにより、企業は優れた製品の一貫性を確保しながら、高まる需要を満たすことができます。

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 製造プロセス分析

- 原材料分析と調達戦略

- 白色セメントと灰色セメントの比較分析

- 利益率分析

- バリューチェーン分析

- トランプ政権の関税の影響:構造化された概要

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)注:上記の貿易統計は主要国についてのみ提供されます

- 主要輸出国

- 主要輸入国

- 利益率分析

- 主なニュースと取り組み

- 技術の情勢

- 伝統的な製造技術

- 高度な製造技術

- 新興技術

- 特許分析

- 規制情勢

- 市場力学

- 市場促進要因

- 美観建築資材の需要増加

- 都市化とインフラ整備の開発

- 建築用途での採用増加

- プレキャスト・プレハブ建設の成長

- 市場抑制要因

- 灰色セメントに比べて高い生産コスト

- 環境問題と炭素排出

- 原材料価格の変動

- 高品質原材料の入手への制約

- 市場機会

- 生産プロセスにおける技術の進歩

- 新興国における需要の増加

- 環境に優しい白色セメントの変種の開発

- 応用分野の拡大

- 市場の課題

- 厳しい環境規制

- 生産における高いエネルギー消費

- 輸送と物流の課題

- 代替材料との競合

- 規制枠組み分析

- 国際規格(ASTM C989/C989 M、EN 197-1)

- 地域の規制と基準

- 環境コンプライアンス要件

- 品質認証システム

- テクノロジー情勢

- 現在の技術動向

- スラグセメント製造における新興技術

- デジタル化とインダストリー4.0の影響

- 研究開発イニシアチブとイノベーション・パイプライン

- 価格分析

- 価格動向分析

- コスト構造分析

- 価格に影響を与える要因

- 地域による価格差

- 市場促進要因

- PESTEL分析

- ポーターのファイブフォース分析

- 規制枠組みと政府の取り組み

- COVID-19の影響白色セメント市場

- ロシア・ウクライナ紛争がサプライチェーンに与える影響

- 新規参入者の市場参入戦略

- 価格分析と動向

- 貿易分析:輸出入シナリオ

第4章 競合情勢

- 市場シェア分析

- 戦略的ダッシュボード

- 主要な利害関係者と市場ポジショニング

- 競合ベンチマーキング

- 競合ポジショニングマトリックス

- 競争戦略

- 新製品開発

- 企業合併・買収 (M&A)

- 事業提携・協力

- 生産能力拡張

- 主要企業のSWOT分析

- 競争の激しさ:ポーターのファイブフォース分析

第5章 市場推計・予測:製品種類別(2021~2034年)

- 主要動向

- 白色ポートランドセメント

- 石工用白色セメント

- 白色ポートランド石灰石セメント(PLC)

- その他(白色アルミン酸カルシウムセメント等)

第6章 市場推計・予測:グレード別(2021~2034年)

- 主要動向

- タイプ52.5

- タイプ42.5

- タイプ32.5

- その他

第7章 市場推計・予測:用途別(2021~2034年)

- 主要動向

- 住宅建設

- 商業建設

- インフラ開発

- 装飾用途

第8章 市場推計・予測:最終用途別(2021~2034年)

- 主要動向

- 建築用コンクリート

- プレキャスト製品

- 人造大理石フローリング

- スイミングプール

- カウンタートップと装飾要素

- その他

第9章 市場推計・予測:地域別(2021~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ

第10章 企業プロファイル

- Aalborg Portland A/S

- Adana Cimento Sanayii T.A.S.

- Aditya Birla Group(UltraTech Cement Ltd.-Birla White)

- Cementir Holding N.V.

- Cemex S.A.B. de C.V.

- Cimsa Cimento Sanayi ve Ticaret A.S..

- Federal White Cement Ltd.

- Holcim Group

- J.K. Cement Ltd.

- Lehigh White Cement Company

- OYAK Cement

- Ras Al Khaimah Cement Company(RAKCC)

- Royal White Cement Inc.

- Saveh White Cement Co.

- Shargh White Cement Co.

The Global White Cement Market was valued at USD 10.5 billion in 2024 and is estimated to grow at 6.8% CAGR to reach USD 20.2 billion by 2034, driven by the surge in global infrastructure development. With urbanization progressing rapidly, governments are investing significantly in constructing roads, bridges, and public buildings, increasing the demand for high-quality, visually appealing building materials such as white cement.

Sustainability has become another key factor propelling the white cement market forward. Its heat-reflective properties make it an excellent choice for energy-efficient construction, aligning with the increasing demand for eco-friendly building materials. As architects and builders seek to reduce carbon footprints in their designs, white cement's benefits in contributing to energy savings and environmental sustainability have positioned it as a preferred material in the construction industry. In response to evolving market needs, manufacturers are introducing new formulations of white cement that offer enhanced performance characteristics, such as improved strength and faster setting times. These innovations are expanding the scope of white cement applications, making them more viable and cost-effective for large-scale construction projects. As urban growth continues and construction trends evolve, the market is expected to maintain its positive momentum, offering significant opportunities for established companies and new entrants in the building materials sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.5 Billion |

| Forecast Value | $20.2 Billion |

| CAGR | 6.8% |

In 2024, white Portland cement represented a 59.5% share. This segment is the most widely used due to its high strength, superior finish, and aesthetic appeal. It is predominantly employed in architectural and decorative applications, such as walls, flooring, and sculptures, where uniformity in color and brightness is essential. The demand for this segment is largely driven by the growing development of premium construction projects and an increasing preference for visually appealing structures in residential and commercial spaces.

The residential construction sector held a market share of 29.5% in 2024. White cement is highly favored in residential construction due to its exceptional finishing, durability, and aesthetic value, making it a popular choice for interior and exterior walls, flooring, and decorative elements. The rise in housing demand, fueled by urbanization and population growth, has been a key factor in the sector's growth. As homeowners seek materials that offer elegance and longevity, white cement has become a preferred option for creating high-end, lasting residential spaces.

U.S. White Cement Market held an 85% share valued at USD 2.3 million in 2024. The country is set to experience rapid growth in white cement consumption, driven by an expansion in construction activities, technological advancements, and a strong focus on sustainable building practices. The high demand for durable and aesthetically pleasing building materials, combined with a surge in infrastructure development, is significantly boosting the consumption of white cement in the U.S.

Key players such as J.K. Cement, Aalborg Portland, UltraTech Cement, Cemex, and Cimsa are capitalizing on these strategies to meet the growing demand for white cement and stay ahead in the highly competitive market. Companies in the white cement market have implemented several key strategies to bolster their presence and strengthen their market position. These include focusing on product innovation, expanding production capacities, and building strategic partnerships. By developing specialized white cement variants that cater to specific needs like high-strength formulations, aesthetic finishes, or sustainability, companies ensure they meet the growing demand from both residential and commercial sectors. Investment in cutting-edge technologies that improve production efficiency and quality is also a crucial strategy. This allows companies to meet the rising demand while ensuring superior product consistency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research Methodology

- 1.2 Research Objectives

- 1.3 Market Definition and Scope

- 1.4 Market Segmentation

- 1.5 Data Sources

- 1.5.1 Primary Research

- 1.5.2 Secondary Research

- 1.6 Market Estimation Approach

- 1.7 Research Assumptions and Limitations

- 1.8 Base Year and Forecast Period

Chapter 2 Executive Summary

- 2.1 Market Snapshot

- 2.2 Global White Cement Market Highlights

- 2.3 Regional Market Highlights

- 2.4 Segmental Market Highlights

- 2.5 Competitive Landscape Snapshot

- 2.6 Investment Highlights and Strategic Recommendations

- 2.7 Key Market Trends and Future Growth Indicators

- 2.8 Analyst Perspective and Critical Insights

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Manufacturing process analysis

- 3.1.2 Raw material analysis and sourcing strategies

- 3.1.3 White cement vs. gray cement: comparative analysis

- 3.1.4 Profit margin analysis

- 3.1.5 Value chain analysis

- 3.2 Impact of trump administration tariffs - structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.2 Price volatility in key materials

- 3.2.2.3 Supply chain restructuring

- 3.2.2.4 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code) Note: the above trade statistics will be provided for key countries only.

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.5.1 Technology landscape

- 3.5.2 Traditional manufacturing technologies

- 3.5.3 Advanced manufacturing technologies

- 3.5.4 Emerging technologies

- 3.5.5 Patent analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Market dynamics

- 3.7.1 Market drivers

- 3.7.1.1 Growing demand for aesthetic construction materials

- 3.7.1.2 Increasing urbanization and infrastructure development

- 3.7.1.3 Rising adoption in architectural applications

- 3.7.1.4 Growth in precast and prefabricated construction

- 3.7.2 Market Restraints

- 3.7.2.1 Higher production costs compared to gray cement

- 3.7.2.2 Environmental concerns and carbon emissions

- 3.7.2.3 Raw material price volatility

- 3.7.2.4 Limited availability of high-quality raw materials

- 3.7.3 Market Opportunities

- 3.7.3.1 Technological advancements in production processes

- 3.7.3.2 Growing demand in emerging economies

- 3.7.3.3 Development of eco-friendly white cement variants

- 3.7.3.4 Expansion of application areas

- 3.7.4 Market Challenges

- 3.7.4.1 Stringent Environmental Regulations

- 3.7.4.2 High energy consumption in production

- 3.7.4.3 Transportation and logistics challenges

- 3.7.4.4 Competition from alternative materials

- 3.7.5 Regulatory Framework Analysis

- 3.7.5.1. International standards (ASTM C989/C989 M, EN 197-1)

- 3.7.5.2 Regional regulations and standards

- 3.7.5.3 Environmental compliance requirements

- 3.7.5.4 Quality certification systems

- 3.7.6 Technology Landscape

- 3.7.6.1 Current technological trends

- 3.7.6.2 Emerging technologies in slag cement production

- 3.7.6.3 Digitalization and industry 4.0 impact

- 3.7.6.4 R&d initiatives and innovation pipeline

- 3.7.7 Pricing Analysis

- 3.7.7.1 Price trend analysis

- 3.7.7.2 Cost structure analysis

- 3.7.7.3 Factors affecting pricing

- 3.7.7.4 Regional price variations

- 3.7.1 Market drivers

- 3.8 PESTLE Analysis

- 3.9 Porter's five forces analysis

- 3.10 Regulatory framework and government initiatives

- 3.11 Impact of covid-19 on white cement market

- 3.12 Impact of Russia Ukraine conflict on supply chain

- 3.13 Market entry strategies for new players

- 3.14 Pricing analysis and trends

- 3.15 Trade analysis: import-export scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Market share analysis, 2024

- 4.2 Strategic dashboard

- 4.3 Key stakeholders and market positioning

- 4.4 Competitive benchmarking

- 4.5 Competitive positioning matrix

- 4.6 Competitive strategies

- 4.6.1 new product developments

- 4.6.2 mergers and acquisitions

- 4.6.3 partnerships and collaborations

- 4.6.4 capacity expansions

- 4.7 SWOT analysis of key players

- 4.8 competitive intensity - Porter's five forces analysis

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 White Portland Cement

- 5.3 White Masonry Cement

- 5.4 White Portland Limestone Cement (PLC)

- 5.5 Others (White Calcium Aluminate Cement, etc.)

Chapter 6 Market Estimates and Forecast, By Grade, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Type 52.5

- 6.3 Type 42.5

- 6.4 Type 32.5

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Residential Construction

- 7.3 Commercial Construction

- 7.4 Infrastructure Development

- 7.5 Decorative Applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Architectural Concrete

- 8.3 Precast Products

- 8.4 Terrazzo Flooring

- 8.5 Swimming Pools

- 8.6 Countertops and Decorative Elements

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Aalborg Portland A/S

- 10.2 Adana Cimento Sanayii T.A.S.

- 10.3 Aditya Birla Group (UltraTech Cement Ltd. - Birla White)

- 10.4 Cementir Holding N.V.

- 10.5 Cemex S.A.B. de C.V.

- 10.6 Cimsa Cimento Sanayi ve Ticaret A.S..

- 10.7 Federal White Cement Ltd.

- 10.8 Holcim Group

- 10.9 J.K. Cement Ltd.

- 10.10 Lehigh White Cement Company

- 10.11 OYAK Cement

- 10.12 Ras Al Khaimah Cement Company (RAKCC)

- 10.13 Royal White Cement Inc.

- 10.14 Saveh White Cement Co.

- 10.15 Shargh White Cement Co.