|

市場調査レポート

商品コード

1844368

電子料金徴収の市場機会、成長促進要因、産業動向分析、2025年~2034年の予測Electronic Toll Collection (ETC) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 電子料金徴収の市場機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年09月26日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

概要

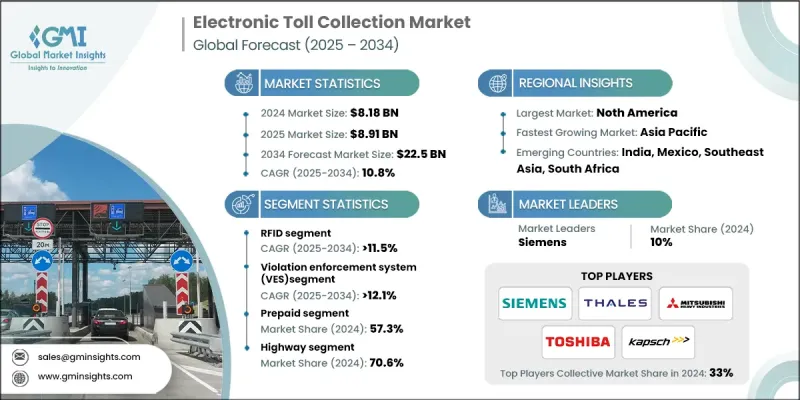

電子料金徴収(ETC)の世界市場規模は、2024年に81億8,000万米ドルとなり、CAGR 10.8%で成長し、2034年には225億米ドルに達すると予測されています。

都市人口の急増と自家用車所有率の上昇により、特に高速道路や都市回廊で交通渋滞が発生しています。ETCシステムは、料金支払いを自動化し、渋滞を緩和し、料金所での処理能力を向上させることで、交通の遅れを減らすように設計されています。世界各国の政府は、デジタル料金徴収フレームワークへの移行を優先し、相互運用性の標準化を推進し、手作業による現金徴収を廃止しています。RFID、人工知能、クラウドプラットフォーム、ANPRシステムなどの技術進歩により、最新のETCソリューションはより正確で効率的、かつ安全になっています。また、これらの技術は運用コストの削減にも役立ち、より広範な展開を可能にしています。さらに、モバイル・ウォレットやデジタル決済ソリューションの普及により、利用者の利便性はさらに向上しています。ETCシステムは、アイドリング時間と燃料消費を削減し、排出量の削減につながることで、環境の持続可能性に貢献します。各国が持続可能性イニシアティブと脱炭素目標に取り組む中、ETCはよりクリーンでスマートな交通システムの構築に不可欠な役割を果たしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 81億8,000万米ドル |

| 予測金額 | 225億米ドル |

| CAGR | 10.8% |

2024年、RFID技術セグメントは46%のシェアを占め、2034年までCAGR 11.5%で成長すると予測されます。RFIDは、世界の料金徴収ネットワーク、特にアジア全域の地域において、依然として支配的で費用対効果の高いソリューションです。これらのシステムは、その手頃な価格、シンプルさ、広範な採用により、非常に支持されています。一方、DSRC(Dedicated Short-Range Communication:専用近距離通信)は、主に高速の一般道料金徴収環境やV2X通信において、欧州や韓国などの一部の地域で引き続き使用されています。RFIDが世界市場をリードする一方で、DSRCは特定の地域のエコシステムで存在感を維持しています。

違反取締システム(VES)セグメントは、2025年から2034年にかけてCAGR 12.1%で成長する見込みです。オープンロード、キャッシュレス料金へのシフトが加速するにつれ、自動取締りツールの需要が大幅に高まっています。VES技術は、カメラ、センサーシステム、ANPRを利用して通行料金違反者を特定し、コンプライアンスを実施します。これらのシステムは、違反検知を自動化することで、収益損失を防ぎ、料金関連法規の遵守を確実にするのに役立ちます。AIとアナリティクスによって強化された最新のVESソリューションは、検知精度が向上し、次世代の有料道路インフラに不可欠なものとなっています。

米国電子料金徴収(ETC)市場は2024年に87.4%のシェアを占めます。全電子料金(AET)システムの普及により、有料道路の運営方法が変革され、現金払いがなくなり、よりスムーズな交通の流れが可能になりつつあります。これらのシステムは運用コストを削減するだけでなく、ダイナミックな料金設定モデルを通じて渋滞管理もサポートします。リアルタイムの交通データに基づく変動料金制が普及しつつあり、オフピークの移動を促し、交通効率を向上させることで、移動行動に影響を与えるのに役立っています。

世界の電子料金徴収(ETC)市場をリードする主要企業には、シーメンス、タレス、Conduent、東芝、Kapsch TrafficCom、三菱重工業、Neology、EFKON、Cubic、TransCore/ST Engineeringなどがあります。ETC市場のプレーヤーは、その地位を強化するため、交通当局や政府との戦略的提携に注力し、統合された料金徴収インフラを展開しています。研究開発への投資は、精度の向上、システムコストの削減、AI主導型アナリティクスの実装を優先しています。各社は、特に急成長地域における長期契約を確保することで、グローバルな事業展開を積極的に進めています。また、多くの企業が、管轄区域を超えたシームレスな移動を可能にする相互運用性プロトコルに取り組んでいます。

よくあるご質問

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 電子料金徴収バリューチェーン

- 政府と民間セクターの関係

- テクノロジープロバイダーとオペレーターのダイナミクス

- 標準化団体の影響要因

- 交通局統合の混乱

- 業界への影響要因

- 促進要因

- 交通渋滞の深刻化

- 政府の政策と規制

- 技術的進歩

- 環境持続可能性の目標

- シームレスな旅行の需要の高まり

- 業界の潜在的リスク&課題

- 高い導入コスト

- プライバシーとデータセキュリティに関する懸念

- 市場機会

- 新興市場への拡大

- スマートモビリティとの統合とそ

- AIと分析の導入

- 環境と持続可能性への取り組み

- 促進要因

- 成長可能性分析

- 規制情勢

- FHWA電子料金徴収基準

- DOTインテリジェント交通システムガイドライン

- DSRCのFCC周波数割り当て

- 国際規格(ISO、CEN、ETSI)

- 地方運輸局規制

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許分析

- 価格動向分析

- 運用コストの比較

- 総所有コスト分析

- コスト内訳分析

- インフラ開発コスト

- 技術導入費用

- システム統合とカスタマイズ

- 持続可能性と環境側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

- 市場展開統計

- ETCシステム設置率

- トランスポンダー採用指標

- 交通量処理分析

- 投資情勢分析

- 政府のインフラ投資

- 民間有料道路投資

- PPPプロジェクトの資金調達分析

- 競合情報

- テクノロジーリーダーシップ評価

- ソリューションカテゴリー別市場シェア

- 契約の勝敗分析

- 顧客行動分析

- ビジネスモデルの進化

- 従来のシステム統合モデル

- 建設・運営・譲渡(BOT)モデル

- パフォーマンスと品質基準

- 取引の正確性要件

- システム可用性基準

- リスク評価フレームワーク

- 実装タイムライン分析

- システム設計・計画段階

- インフラストラクチャのインストールタイムライン

- 相互運用性と標準フレームワーク

- 技術的な相互運用性の要件

- ビジネスルールの調和

- プライバシーとデータセキュリティ

- トラフィック管理統合

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 市場参入障壁

- 主なニュースと取り組み

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- RFID

- DSRC

- GPS/GNSS

- ビデオ分析

- その他

第6章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 自動車両分類(AVC)

- 違反執行システム(VES)

- 自動車両識別システム(AVIS)

- その他(バックオフィス・サービス)

第7章 市場推計・予測:支払い方法別、2021年~2034年

- 主要動向

- プリペイド

- ハイブリッド

- 後払い

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 都市部

- 高速道路

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- オランダ

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- 世界のトップ企業

- Kapsch TrafficCom

- TransCore(Roper Technologies)

- Cubic Transportation Systems

- Siemens Mobility

- Thales

- EFKON

- Q-Free

- Conduent

- Neology

- Toshiba

- 地域有力企業

- TagMaster

- TOLL COLLECT

- Autostrade Tech

- VINCI Highways

- Mitsubishi Heavy Industries

- DENSO

- Huawei Technologies

- Dahua Technology

- International Road Dynamics

- 新興企業とイノベーター

- Genetec

- Raytheon Technologies

- Bosch Mobility Solutions

- Continental

- Atos

- NEC

- Hitachi Vantara

- Accenture

- Cognizant Technology Solutions

- Tata Consultancy Services