|

|

市場調査レポート

商品コード

1620486

自動車用アクティブサスペンションシステム市場の成長機会、成長促進要因、産業動向分析、2024~2032年予測Automotive Active Suspension System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 - 2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 自動車用アクティブサスペンションシステム市場の成長機会、成長促進要因、産業動向分析、2024~2032年予測 |

|

出版日: 2024年10月30日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

自動車用アクティブサスペンションシステムの世界市場は、2023年に42億米ドルの評価額に達し、2024~2032年にかけてCAGR 4.6%で成長する見込みです。

アクティブサスペンションシステムの統合により、自動車産業はますます変貌を遂げ、先進技術によって自動車の性能と快適性が向上しています。従来のサスペンションとは異なり、アクティブシステムはアクチュエータと先進的ソフトウェアを利用して各車輪をリアルタイムで調整し、路面状況の変化にシームレスに適応します。この適応性により、荒れた路面での効率的な乗り心地や、高速走行時の優れた安定性がもたらされ、現代の消費者に付加価値をもたらしています。電気自動車やハイブリッド車の採用が増加していることも、アクティブサスペンションシステムの成長を促す大きな要因となっています。

これらの車両は、低重心でバッテリー重量が重く設計されていることが多く、ハンドリングと快適性に独特の課題があります。アクティブサスペンション技術は、リアルタイムの調整を可能にすることでこれらに対処し、荷重が加わった場合でもバランスとスムーズな乗り心地を確保します。自動車メーカーが電気自動車やハイブリッドモデルの高性能化と独自機能の追求に努める中、アクティブサスペンションシステムは差別化の鍵となりつつあり、この市場セグメントのさらなる拡大に拍車をかけています。市場は流通チャネル別にOEMとアフターマーケットに分けられ、2023年にはOEMが市場の30億米ドルを占める。OEMは、生産時にアクティブサスペンションシステムを統合し、互換性と最適な性能を確保することで、大きなシェアを維持しています。

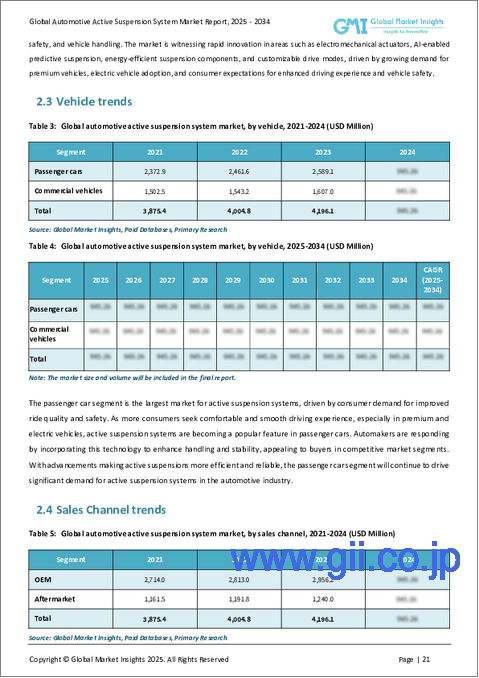

プレミアムな自動車機能に対する需要は増加の一途をたどっており、OEMは、快適性と安定性の向上を求める消費者の嗜好に応えるため、高級モデルや電動モデルにアクティブサスペンションを組み込むケースが増えています。この動向は、予測期間にわたってOEMセグメントの成長を促進すると予想されます。車両別では、乗用車と商用車があり、2023年のシェアは乗用車が62%を占める。乗り心地と安全性の向上に対する消費者の需要が、特に高級乗用車や電気乗用車でのアクティブサスペンションの採用を促進しています。自動車メーカーは、ハンドリングと乗り心地を改善するために乗用車にこの技術を搭載し、快適で安定した運転体験を求める購入者に対応しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2023年 |

| 予測年 | 2024~2032年 |

| 開始金額 | 42億米ドル |

| 予測金額 | 63億米ドル |

| CAGR | 4.6% |

消費者の嗜好が進化するにつれ、この動向は今後も続くと考えられます。中国市場は重要な成長促進要因であり、2023年には売上シェアの35%を占める。中国では、高級車や電気自動車に対する需要が高く、EV導入に対する政府の支援や消費者の所得増加もあって、アクティブサスペンションシステムを搭載した自動車の普及が加速しています。また、世界の動向や規制の優先順位に合わせて、現地の自動車メーカーも先進的なサスペンション技術を統合するための研究開発に多額の投資を行っています。このように、快適性を求める消費者の需要と電気自動車に対する規制上の支援が組み合わさることで、中国はアクティブサスペンションシステムにとって極めて重要な市場となっており、産業の成長軌道における重要性が高まっています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- サプライヤーの状況

- 原料サプライヤー

- 部品サプライヤー

- メーカー

- サービスプロバイダー

- 販売業者

- 最終用途

- 利益率分析

- コスト内訳分析

- 価格分析

- 技術とイノベーションの展望

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 車両の安定性と制御性の向上

- 乗客の快適性と安全性に対する需要の高まり

- EVと高級車の採用増加

- センサーとアクチュエータ技術の進歩

- 産業の潜在的リスク・課題

- 高い開発コストと統合コスト

- 複雑なメンテナンス要件とコスト

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:システム別、2021~2032年

- 主要動向

- 電磁サスペンション

- 油圧式サスペンション

- 空気圧サスペンション

- 電気油圧式サスペンション

第6章 市場推定・予測:車両別、2021~2032年

- 主要動向

- 乗用車

- 商用車

第7章 市場推定・予測:アクチュエータ別、2021~2032年

- 主要動向

- リニア

- ロータリー

第8章 市場推定・予測:技術別、2021~2032年

- 主要動向

- セミアクティブ

- フルアクティブ

第9章 市場推定・予測:流通チャネル別、2021~2032年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推定・予測:地域別、2021~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 東南アジア

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Audi(Volkswagen Group)

- Bosch

- Brembo

- BWI

- ClearMotion

- Continental

- Denso

- Hitachi

- Hyundai Mobis

- JTEKT

- KYB

- Magna

- Mando

- Marelli

- Mercedes-Benz

- NIO

- Schaeffler

- Tenneco

- Toyota(Aisin Seiki)

- ZF

The Global Automotive Active Suspension System Market reached a valuation of USD 4.2 billion in 2023, with expectations of growing at a 4.6% CAGR from 2024 to 2032. The integration of active suspension systems is increasingly transforming the automotive industry, enhancing vehicle performance and comfort through advanced technology. Unlike traditional suspensions, active systems utilize actuators and sophisticated software to make real-time adjustments for each wheel, adapting seamlessly to changing road conditions. This adaptability provides efficient rides over rough surfaces and superior stability during high-speed maneuvers, adding value for modern consumers. The rising adoption of electric and hybrid vehicles is a significant factor driving active suspension system growth.

These vehicles, often designed with a lower center of gravity and heavier battery weight, present unique handling and comfort challenges. Active suspension technology addresses these by enabling real-time adjustments, ensuring balance and smoother rides even with added load. As automakers strive for higher performance and unique features in electric and hybrid models, active suspension systems are becoming key differentiators, spurring further expansion in this market segment. The market is divided by sales channel into OEMs and the aftermarket, with OEMs commanding USD 3 billion of the market in 2023. OEMs maintain a substantial share by integrating active suspension systems during production, ensuring compatibility and optimal performance.

The demand for premium automotive features continues to rise, and OEMs are increasingly incorporating active suspensions into luxury and electric models to cater to consumer preferences for enhanced comfort and stability. This trend is expected to bolster the growth of the OEM segment over the forecast period. Segmented by vehicle type, the market includes passenger cars and commercial vehicles, with passenger cars holding a 62% share in 2023. Consumer demand for enhanced ride quality and safety is driving active suspension adoption, particularly in premium and electric passenger vehicles. Automakers are responding by equipping passenger cars with this technology to improve handling and ride smoothness, catering to buyers looking for a comfortable and stable driving experience.

| Market Scope | |

|---|---|

| Start Year | 2023 |

| Forecast Year | 2024-2032 |

| Start Value | $4.2 Billion |

| Forecast Value | $6.3 Billion |

| CAGR | 4.6% |

This trend is set to continue as consumer preferences evolve. China market represents a significant growth driver, holding 35% of the revenue share in 2023. High demand for luxury and electric vehicles in China, alongside government support for EV adoption and increasing consumer incomes, is accelerating the uptake of vehicles equipped with active suspension systems. Local automakers are also investing heavily in R&D to integrate advanced suspension technologies, aligning with global trends and regulatory priorities. This combination of consumer demand for comfort and regulatory support for electric vehicles makes China a pivotal market for active suspension systems, reinforcing its importance in the industry's growth trajectory.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material supplier

- 3.2.2 Component supplier

- 3.2.3 Manufacturer

- 3.2.4 Service provider

- 3.2.5 Distributor

- 3.2.6 End use

- 3.3 Profit margin analysis

- 3.4 Cost breakdown analysis

- 3.5 Price analysis

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Enhanced vehicle stability and control

- 3.9.1.2 Rising demand for passenger comfort and safety

- 3.9.1.3 Increased EV and luxury vehicle adoption

- 3.9.1.4 Advancements in sensor and actuator technology

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High development and integration costs

- 3.9.2.2 Complex maintenance requirements and costs

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By System, 2021 - 2032 ($Mn, Units)

- 5.1 Key trends

- 5.2 Electromagnetic suspension

- 5.3 Hydraulic suspension

- 5.4 Pneumatic suspension

- 5.5 Electro-hydraulic suspension

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2032 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.3 Commercial vehicles

Chapter 7 Market Estimates & Forecast, By Actuator, 2021 - 2032 ($Mn, Units)

- 7.1 Key trends

- 7.2 Linear

- 7.3 Rotary

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2032 ($Mn, Units)

- 8.1 Key trends

- 8.2 Semi-active

- 8.3 Fully active

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2032 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2032 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Audi (Volkswagen Group)

- 11.2 Bosch

- 11.3 Brembo

- 11.4 BWI

- 11.5 ClearMotion

- 11.6 Continental

- 11.7 Denso

- 11.8 Hitachi

- 11.9 Hyundai Mobis

- 11.10 JTEKT

- 11.11 KYB

- 11.12 Magna

- 11.13 Mando

- 11.14 Marelli

- 11.15 Mercedes-Benz

- 11.16 NIO

- 11.17 Schaeffler

- 11.18 Tenneco

- 11.19 Toyota (Aisin Seiki)

- 11.20 ZF