|

市場調査レポート

商品コード

1833629

自動車用コックピットドメインコントローラの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Automotive Cockpit Domain Controller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用コックピットドメインコントローラの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年09月01日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

概要

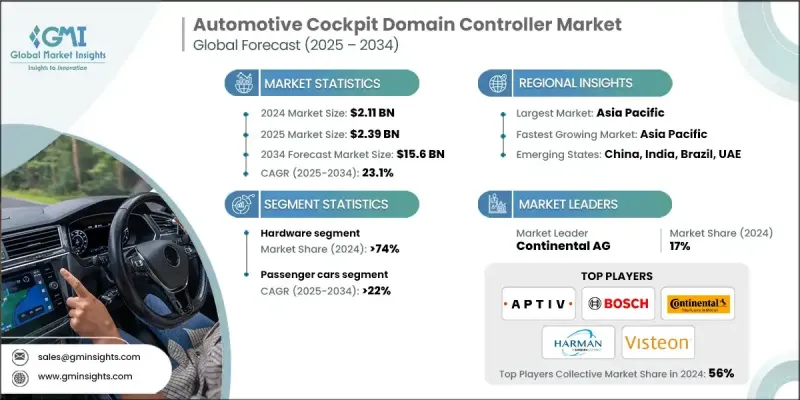

Global Market Insights Inc.が発行した最新レポートによると、自動車用コックピットドメインコントローラの世界市場規模は2024年に21億1,000万米ドルと推定され、CAGR23.1%で2025年の23億9,000万米ドルから2034年には156億米ドルに成長すると予測されています。

自動車メーカーは、複数のスタンドアロンECUから集中型コックピットドメインコントローラに移行することで、ソフトウェアアーキテクチャを合理化し、複雑さを軽減しています。この統合により、配線と重量が削減されるだけでなく、インフォテインメント、計器クラスタ、空調システム全体の更新と診断が簡素化されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 市場金額 | 21億1,000万米ドル |

| 予測金額 | 156億米ドル |

| CAGR | 23.1% |

ハードウェアでの採用増加

自動車用コックピットドメインコントローラ市場のハードウェア分野は、複雑なインフォテインメント、コネクティビティ、安全機能を同時に管理できる強力でエネルギー効率の高いプロセッサの提供に焦点を当てた技術革新により、2024年に大きなシェアを占めました。この分野は、高度なSoC、GPU、高速通信インターフェースを、車載グレードの条件に耐えられるよう設計された、コンパクトで熱的に最適化されたモジュールに統合することで成長を牽引しています。リアルタイム処理とマルチタスク機能に対する需要が高まる中、ハードウェアサプライヤーは、多様な車両要件を満たすためにモジュール設計とスケーラブルアーキテクチャを優先し、次世代スマートコックピットの信頼性と性能を確保しています。

牽引力を増す乗用車

乗用車セグメントは、強化されたユーザー体験、接続性、安全性に対する消費者の期待の高まりに後押しされ、2024年に顕著な収益を上げました。OEMは、音声認識、マルチディスプレイのセットアップ、AIを搭載したアシスタントなど、堅牢なドメインコントローラによって編成されたシームレスなインタラクションを提供するスマートコックピットの統合に多額の投資を行っています。これは、運転体験を再定義する、よりスマートでコネクテッドなインテリアへの明確な動向を反映しています。

アジア太平洋が有望な地域となる

アジア太平洋は、急速な都市化、自動車生産の増加、高度な車載技術に対する消費者の需要の拡大により、自動車用コックピットドメインコントローラ市場の主要な成長エンジンとなっています。中国、日本、韓国、インドなどの国々は、電動モビリティとデジタル変革を推進する政府のイニシアティブに支えられて、スマート車両技術に多額の投資を行っています。市場の成長を後押ししているのは、コネクテッド・インテリジェント・コックピット・ソリューションに対する需要の高まりを取り込もうとする、現地の製造能力とグローバルサプライヤーと地域の自動車メーカーとの強力な協力関係です。

自動車用コックピットドメインコントローラ市場の主要企業は、Visteon、NVIDIA、Robert Bosch、Qualcomm Technologies、Aptiv、HARMAN、Denso、Intel、Faurecia、Continentalです。

市場ポジションを強化するため、自動車用コックピットドメインコントローラ分野の企業はいくつかの戦略的イニシアティブに注力しています。これには、AI、AR、5Gコネクティビティなどの新技術を統合した、スケーラブルで高性能なプラットフォームを開発するための研究開発投資が含まれます。多くの企業は、特定の車種や地域に合わせてカスタマイズされたソリューションを共同開発するために、OEMやソフトウェア開発者とパートナーシップや合弁事業を結んでいます。さらに、特にアジア太平洋を中心に製造拠点を拡大することで、より迅速な納品とコストメリットを実現しています。各社はまた、進化する安全基準と消費者の期待に応えるため、サイバーセキュリティ機能と無線アップデート機能を重視し、競争が激しく急速に進化するこの市場での足場を固めています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- グローバル

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 一次調査と検証

- 一次情報

- 予測モデル

- 調査の前提条件と制限

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 成長促進要因

- コネクテッドカーやソフトウェア定義車両への需要の高まり

- 集中型電気自動車アーキテクチャへの移行

- 高度なインフォテインメントとデジタルコックピット体験に対する消費者の需要の高まり

- EVと自動運転車の成長

- 半導体・ソフトウェア企業とのOEMティア1コラボレーション

- 業界の潜在的リスク・課題

- 高い統合・ソフトウェア検証コスト

- サイバーセキュリティとデータプライバシーのリスク

- 市場機会

- クラウド対応・OTAアップデートエコシステムの拡大

- 新興市場(APAC、LATAM、MEA)への浸透拡大

- 高度なHMIとマルチモーダルインタラクションシステム

- モビリティサービス・フリートアプリケーションとの統合

- 成長促進要因

- 成長可能性分析

- 規制と基準の情勢

- 世界の規制枠組みの分析

- 機能安全規格とその実装

- 地域ごとの規制の違いとコンプライアンス

- コンプライアンスコスト分析と実装戦略

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- ハードウェア技術の成熟度

- ソフトウェアプラットフォームの準備

- 統合の複雑さの評価

- 将来の技術ロードマップ

- ハードウェアの進化のタイムラインとマイルストーン

- ソフトウェアプラットフォーム開発ロードマップ

- 新興技術統合スケジュール

- 標準の進化と業界への影響

- オートサーアダプティブプラットフォームの進化

- ISO 26262の更新と安全性への影響

- サイバーセキュリティ標準ロードマップ

- 現在の技術動向

- コスト構造分析とビジネスケースフレームワーク

- 総所有コスト(TCO)分析

- ROIモデルと回収分析

- 価格戦略分析とベンチマーク

- 市場セグメント別の投資要件

- 特許分析

- 持続可能性とESG影響評価

- 環境影響分析と指標

- 社会的影響の考慮と指標

- ガバナンスとコンプライアンスのフレームワーク

- ESG投資の意義と財務への影響

- ユースケースとアプリケーション

- 最良のシナリオ

- サプライチェーンインテリジェンスとリスク評価

- グローバルサプライチェーンのマッピングと分析

- 半導体サプライチェーンの深掘り

- 地政学的リスク評価

- サプライチェーンのレジリエンスと最適化戦略

- 知的財産と特許の情勢

- 特許出願の動向とイノベーション分析

- 主要特許保有者と知的財産戦略分析

- IP収益化の機会と戦略

- 事業の自由と知的財産リスク管理

- 市場参入戦略的枠組み

- 市場参入戦略分析

- 顧客セグメンテーションとターゲティング戦略

- チャネル戦略とパートナーエコシステム

- マーケティングと販売の有効性

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- システムオンチップ

- モジュール

- メモリ

- 接続性

- モジュール

- ディスプレイインターフェース

- カメラとセンサー

- その他(電源管理IC、HUD)

- システムオンチップ

- ソフトウェア

- サービス

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車

- 中型商用車

- 大型商用車

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 集中型アーキテクチャ

- 分散アーキテクチャ

- ゾーンアーキテクチャ

- ハイブリッドアーキテクチャ

第8章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM(オリジナル機器メーカー)チャネル

- アフターマーケットチャネル

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- インフォテインメントシステム

- デジタル計器クラスター

- ヒューマンマシンインターフェース(HMI)

- ヘッドアップディスプレイ(HUD)の統合

- ドライバー監視システム

- 気候制御・快適システム

- 高度なアプリケーションと新たなユースケース

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- グローバルプレーヤー

- Aptiv

- Continental

- Denso

- HARMAN International Industries

- Intel

- NVIDIA

- Qualcomm Technologies

- Robert Bosch

- STMicroelectronics

- Texas Instruments

- Visteon

- Valeo

- 地域プレーヤー

- Alpine Electronics

- Faurecia

- Hyundai Mobis

- Infineon Technologies

- LG Electronics

- Magna International

- NXP Semiconductors

- Panasonic

- Sony

- 新興プレーヤー/破壊者

- Analog Devices

- Black Sesame Technologies

- BYD Company

- ECARX Holdings

- Horizon Robotics

- Huawei Technologies

- MediaTek

- Renesas Electronics

- Tesla