|

市場調査レポート

商品コード

1913379

血行動態モニタリング装置市場:市場機会、成長促進要因、産業動向分析、将来予測(2026~2035年)Hemodynamic Monitoring Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 血行動態モニタリング装置市場:市場機会、成長促進要因、産業動向分析、将来予測(2026~2035年) |

|

出版日: 2026年01月05日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

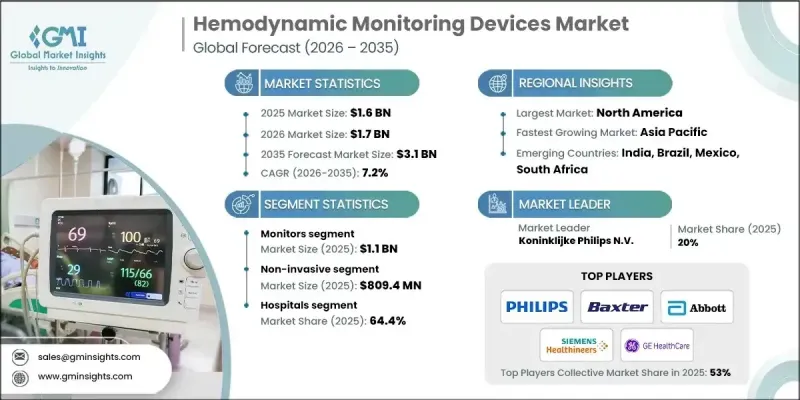

世界の血行動態モニタリング装置市場は、2025年に16億米ドルと評価され、2035年までにCAGR 7.2%で成長し、31億米ドルに達すると予測されています。

この成長は、世界の慢性疾患の増加、モニタリング技術の継続的な革新、遠隔医療ベースのケアモデルの普及拡大、および世界の外科手術件数の増加によって説明されます。血行動態モニタリング装置は、血圧、血流、および全身の循環効率をリアルタイムで追跡することにより、心血管機能のパフォーマンスを評価するシステムと定義されます。これらのツールは、心拍出量、血管抵抗、および関連する生理学的指標に関する継続的な知見を提供することで、臨床判断を支援します。その役割は、手術室、集中治療環境、および高度な依存を必要とする病院環境において特に重要視されています。慢性疾患の蔓延拡大は、特に迅速な介入が必要な状況において、精密な心血管評価ツールの需要を高めているとされています。これらの疾患に関連する合併症は、タイムリーかつ正確な治療判断を支援する先進的なモニタリングプラットフォームの採用を医療提供者に促しています。人工知能(AI)や遠隔接続機能がモニタリングソリューションに深く組み込まれるにつれ、市場動向はさらに加速すると予想され、血行動態モニタリングは現代の臨床ケア提供の中核要素としての地位を確立しつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026~2035年 |

| 当初の市場規模 | 16億米ドル |

| 市場規模予測 | 31億米ドル |

| CAGR | 7.2% |

モニター分野は2025年に11億米ドルの市場規模を生み出しました。このカテゴリーには、高度なベッドサイドシステム、モバイルプラットフォーム、および心拍出量、動脈圧、中心静脈圧を含む継続的な心血管データを提供するように設計された統合モニタリングソリューションが含まれます。これらのモニタリングシステムは、重篤な臨床環境において患者の安定性を維持し、治療方針を決定するための重要なツールと見なされています。利用率は集中治療室(ICU)で最も高く、重篤または不安定な状態の患者を管理するには、中断のない心血管モニタリングが不可欠です。

非侵襲性セグメントは2025年に8億940万米ドルに達し、2035年までCAGR7.3%で成長すると予測されています。非侵襲的循環動態モニタリングソリューションは、皮膚を損傷したりカテーテルを挿入したりすることなく心血管パラメータを評価する技術として位置付けられています。これらのシステムは、患者の安全性と運用効率に重点を置き、高度な生理学的測定手法を用いて心拍出量や輸液反応性を評価します。医療施設では、周術期および集中治療ワークフロー全体において、処置リスクの低減、セットアップ時間の短縮、コスト効率の改善が図られることから、非侵襲的アプローチがますます重視されています。

米国の血行動態モニタリング装置市場は、2025年に5億2,040万米ドル規模に達しました。米国は心血管疾患の発生率が高く、医療インフラが整備されていることから、市場をリードしているとされています。国内の病院や高度医療センターでは、複雑な外科手術、外傷管理、高度な心臓インターベンションを受ける患者を支援するため、幅広いモニタリングソリューションに大きく依存していると言われています。

よくあるご質問

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界のエコシステム分析

- 業界への影響要因

- 促進要因

- 世界の慢性疾患の発生率上昇

- 血行動態モニタリング装置における技術的進歩

- 遠隔医療サービスへの選好の高まり

- 手術件数の増加

- 業界の潜在的リスクと課題

- 患者モニタリング装置の高コスト

- 厳格な規制枠組み

- 市場機会

- 外来・在宅医療環境における拡大

- AIとデータ分析の統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術進歩

- 現在の技術動向

- 新興技術

- サプライチェーン分析

- 償還シナリオ

- 価格分析(2024年)

- 将来の市場動向

- ポーターのファイブフォース分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業別の市場シェア分析

- 企業マトリックス分析

- 主要企業の競合分析

- 競合ポジショニング・マトリックス

- 主な動向

- 企業合併・買収 (M&A)

- 事業提携・協力

- 新製品の発売

- 拡大計画

第5章 市場の推定・予測:製品別(2022~2035年)

- 使い捨て製品

- モニター

第6章 市場の推定・予測:システムの種類別(2022~2035年)

- 非侵襲性

- 侵襲性

- 低侵襲性

第7章 市場の推定・予測:最終用途別(2022~2035年)

- 病院

- 外来手術センター

- 在宅医療

- その他の用途

第8章 市場の推定・予測:地域別(2022~2035年)

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott Laboratories

- Baxter International

- Becton, Dickinson and Company(BD)

- Canon Medical Systems Corporation

- Deltex Medical Group

- Edwards Lifesciences Corporation

- GE HealthCare Technologies

- Getinge

- ICU Medical

- Koninklijke Philips N.V.

- Masimo Corporation

- Mindray

- Nihon Kohden Corporation

- OSYPKA MEDICAL

- Siemens Healthineers.