|

|

市場調査レポート

商品コード

1833681

睡眠時無呼吸症候群用インプラントの市場機会と促進要因、産業動向分析、2025年~2034年予測Sleep Apnea Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 睡眠時無呼吸症候群用インプラントの市場機会と促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年09月10日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

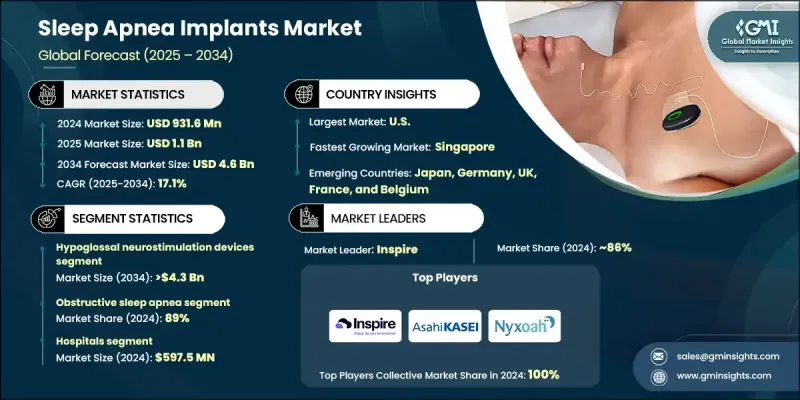

睡眠時無呼吸症候群用インプラントの世界市場は、2024年には9億3,160万米ドルと評価され、CAGR 17.1%で成長し、2034年には46億米ドルに達すると推定されています。

この急成長は、閉塞性睡眠時無呼吸症候群の有病率の上昇、CPAP療法のコンプライアンスの制限、睡眠関連の健康状態に対する意識の高まりによって推進されています。睡眠時無呼吸症候群用インプラントは、マスクベースの治療に代わる、低侵襲でマスクフリーのソリューションを提供し、睡眠中の閉塞を防ぐために気道の筋肉を刺激します。多くの患者が従来の治療法に不快感や不耐性、不便さを感じていることから、これらのデバイスは支持を集めています。臨床的な革新と患者に優しい装置への注目の高まりにより、インプラントは長期的で効果的な解決策を求める患者にとって重要な選択肢となりつつあります。また、医師の支持の高まり、技術の進歩、未治療のOSAと心血管、代謝、神経学的リスクとの関連性に対する認識の高まりにより、市場は拡大しています。競合情勢を形成しているのは、Inspire、Nyxoah、旭化成などの大手企業であり、大手企業は広範な製品ポートフォリオと世界的なリーチを活用する一方、中小企業はニッチ技術と集中的な研究努力によって成長を推進しています。これらのダイナミクスが相まって、世界的な睡眠時無呼吸症候群治療の変革が進んでいます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 9億3,160万米ドル |

| 予測金額 | 46億米ドル |

| CAGR | 17.1% |

舌下神経刺激装置セグメントは2024年に86.7%のシェアを占め、実証された臨床結果、医師の嗜好、従来の治療法に不耐性の患者への広範な採用が支持されています。CPAPの長期的なアドヒアランスには限界があり、患者の約3分の1しか一貫した使用を維持していないことから、生活の質と利便性の向上を提供する埋め込み型オプションへの需要がさらに高まっています。

閉塞性睡眠時無呼吸症候群は、OSAの高い有病率と従来の治療法の欠点に牽引され、2024年には89%のシェアを占める。何百万人もの患者が診断を受けていないが、この疾患が心臓病、糖尿病、認知機能低下と関連していることへの認識は高まっており、長期的な利益をもたらすインプラントを用いた治療を推進する原動力となっています。

病院部門は、2024年に5億9,750万米ドルを稼ぎ出し、インプラント治療がその原動力となっています。病院の優位性は、高度なインフラ、専門外科医の確保、包括的な術後ケアに起因しており、舌下神経刺激装置や呼吸神経刺激装置などの装置の安全な埋め込みと継続的なモニタリングが保証されています。集学的チームと高度な診断ツールが、病院での導入率をさらに高めています。

米国睡眠時無呼吸症候群用インプラント2024年の市場規模は8億4,000万米ドル。同地域の成長の原動力は、OSA患者の多さ、有利な償還制度、植込み型デバイスの早期導入です。強固な医療インフラと活発な臨床研究、そして旭化成、Inspire Medical Systems、Nyxoahといった企業の存在が、この分野での日本のリーダーシップを牽引し続けています。

睡眠時無呼吸症候群用インプラント業界の有力企業には、Inspire、Nyxoah、旭化成などがあります。睡眠時無呼吸症候群用インプラント市場における足場を固めるため、各社は製品イノベーション、臨床研究、地域拡大を中心とした戦略を実施しています。各社は、従来の治療法よりもアドヒアランスを向上させる低侵襲で患者に優しいデバイスの開発に多額の投資を行っています。臨床試験プログラムの拡大も、有効性を検証し、規制当局の承認を確保し、医師の信頼を築くために不可欠です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 閉塞性睡眠時無呼吸症の有病率の増加

- CPAPに対する遵守率とアドヒアランスが低い

- 技術的進歩

- 睡眠時無呼吸症に関する意識の高まり

- 業界の潜在的リスク&課題

- 睡眠時無呼吸症候群用インプラントの高コスト

- 睡眠時無呼吸症候群用インプラントに関連する合併症

- 市場機会

- OSAと診断される患者数の増加

- 新興市場への進出

- 促進要因

- 成長可能性分析

- 払い戻しシナリオ

- 規制情勢

- 米国

- 欧州

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- 新興国での導入

- OSAの発生率と有病率, 2021-2024

- 製品パイプライン分析

- 起動シナリオ

- 価格分析、2024

- 投資情勢

- 消費者行動分析

- ペイシェントジャーニーマップ

- ポーター分析

- PESTEL分析

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 米国

- 欧州

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 舌下神経刺激装置

- 横隔膜神経刺激装置

第6章 市場推計・予測:適応症別、2021-2034

- 主要動向

- 閉塞性睡眠時無呼吸症

- 中枢性睡眠時無呼吸

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 外来手術センター

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 米国

- 欧州

- ドイツ

- 英国

- スイス

- フランス

- スペイン

- イタリア

- オランダ

- ベルギー

- オーストリア

- フィンランド

- 日本

- シンガポール

第9章 企業プロファイル

- Asahi Kasei

- Inspire

- Nyxoah