|

市場調査レポート

商品コード

1822636

動物飼料用タンパク質の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Animal Feed Protein Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 動物飼料用タンパク質の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年08月28日

発行: Global Market Insights Inc.

ページ情報: 英文 192 Pages

納期: 2~3営業日

|

概要

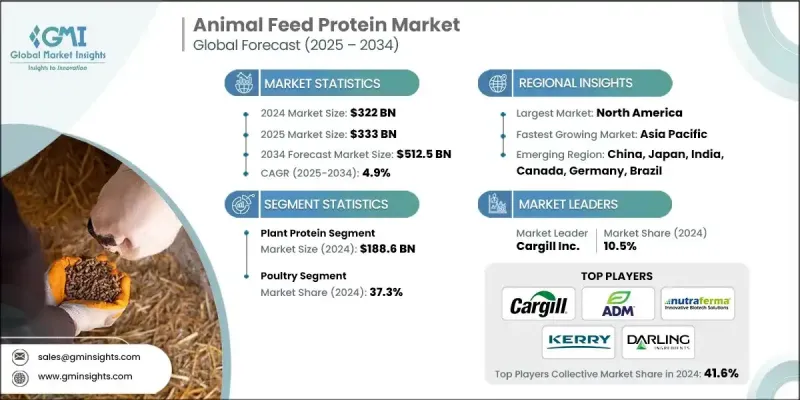

Global Market Insights Inc.が発行した最新レポートによると、世界の動物飼料用タンパク質市場は2024年に3,220億米ドルと推定され、CAGR 4.9%で2025年の3,330億米ドルから2034年には5,125億米ドルに成長すると予測されています。

世界の人口が増加し、特に開発途上国の所得が上昇するにつれて、食肉と乳製品の需要が増加しています。このため、家畜の健全な成長と生産性を支える高品質な動物飼料用タンパク質の必要性が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 3,220億米ドル |

| 予測金額 | 5,125億米ドル |

| CAGR | 4.9% |

植物性タンパク質の採用増加

植物性タンパク質セグメントは、その費用対効果、豊富な入手可能性、持続可能な調達により、2024年に注目すべきシェアを占めました。大豆粕、キャノーラ、エンドウ豆タンパク質などの原料は、高い栄養価と消化のしやすさから、複数の家畜種で広く使用されています。企業は、非遺伝子組み換えやオーガニックの植物性タンパク質の開発に投資しているほか、アミノ酸プロファイルを改善し、標的動物の健康に役立つ生物学的利用能(バイオアベイラビリティ)を高める加工技術にも投資しています。

牽引力を増す家禽類

鶏肉分野は、その手頃な価格と赤身のタンパク質含有量による鶏肉と卵の世界的な需要の高さに支えられて、2024年には持続可能なシェアを維持した。市場成長の原動力となっているのは、大規模な商業的農業経営と一人当たりの鶏肉消費量の増加です。主要な業界プレーヤーは、飼料要求率を高め、疾病リスクを軽減するような飼料の配合に注力しています。戦略には、ブロイラー、レイヤー、ブリーダーの固有の要件を満たすための、酵素強化タンパク質配合や地域別栄養計画の組み込みなどが含まれます。

地域別洞察

北米が有利な地域となる見込み

北米動物飼料用タンパク質市場は、確立された畜産部門、食肉と乳製品に対する高い消費者需要、先進的な農業慣行を背景に、2024年に注目すべき収益を上げました。北米で事業を展開する企業は、飼料工場との合併、生産施設の拡張、持続可能な代替タンパク質への研究開発投資など、将来を見据えた戦略を採用しています。また、動物の成績を向上させ、投入資材の無駄を省くために、精密栄養学とデジタル飼料管理システムにも重点が置かれています。

動物飼料用タンパク質市場の主要企業は、Angel Yeast、Deep Branch Biotechnology、Archer Daniels Midland Company(ADM)、Ynsect、Nutraferma LLC、CHS Inc.、Unibio Group、Innovafeed、DuPont(E.I. DuPont De Nemours and Company)、Darling Ingredients、Kerry Group、Cargill Inc.、Lallemand Inc.、Crescent Biotech、Imcopa Food Ingredients B.V.です。

市場での存在感を高めるため、動物飼料用タンパク質セクターの企業は、イノベーション、パートナーシップ、持続可能性の組み合わせを追求しています。その多くは、藻類や昆虫タンパク質のような代替タンパク源に進出し、製品の多様化と従来の原料への依存度の低減を図っています。畜産農家や栄養研究センターとの戦略的提携は、製品開発を実社会のニーズに合わせるのに役立ちます。さらに、各社はデジタルツールを活用して、効率を最大化するデータ主導型の給餌ソリューションを提供しています。現在では、消費者や規制当局の期待に応えるため、トレーサビリティやエコ認証も重視したブランドづくりが進められています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- グローバル

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)

(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021-2034

- 主な傾向

- 植物性タンパク質

- 動物性タンパク質

- 代替タンパク質

第6章 市場推計・予測:家畜別、2021-2034

- 主要動向

- 家禽

- 豚

- 牛

- 養殖業

- ペットフード

- 馬

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東およびアフリカ

第8章 企業プロファイル

- Cargill Inc.

- Archer Daniels Midland Company(ADM)

- DuPont(E.I. DuPont De Nemours and Company)

- Kerry Group

- Nutraferma LLC

- Darling Ingredient

- Lallemand Inc.

- Angel Yeast

- Imcopa Food Ingredients B.V.

- CHS Inc.

- Crescent Biotech

- Deep Branch Biotechnology

- Unibio Group

- Innovafeed

- Ynsect