|

|

市場調査レポート

商品コード

1616733

シリコーンエラストマーの機会と促進要因、業界動向分析、2024~2032年予測Silicone Elastomers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 - 2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| シリコーンエラストマーの機会と促進要因、業界動向分析、2024~2032年予測 |

|

出版日: 2024年09月10日

発行: Global Market Insights Inc.

ページ情報: 英文 165 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

シリコーンエラストマーの世界市場規模は2023年に128億米ドルとなり、2024~2032年のCAGRは6.4%と予測されています。

この成長の主要要因は、自動車、エレクトロニクス、医療、建設など、さまざまなセグメントでの需要の急増にあります。さらに、大手産業企業間の協力関係の高まりが、市場の需要をさらに後押ししています。2032年、シリコーンエラストマーの医療機器や医療用途への採用が急増していることが主要要因となって、産業は力強い成長を遂げる展望です。この動向が主要産業の生産拡大に拍車をかけ、市場需要を押し上げています。

シリコーンエラストマー固有の生体適合性、耐薬品性、柔軟性は、インプラント、カテーテル、シールなど多様な医療用途に理想的です。医療セグメントでは先進的で耐久性のある材料が重視されているため、シリコーンエラストマーの需要は大幅に増加する見込みです。さらに、ウェアラブル技術や3Dプリンティングなどのセグメントでシリコーンエラストマーの用途が急増していることも、市場の成長をさらに加速させています。産業全体は、製品、用途、地域によって分類されます。

2032年までに80億米ドルを超えると予測される液状シリコーンゴム(LSR)セグメントは、その汎用性と加工の容易さにより、2024~2032年にかけて大きな勢いを増すとみられています。LSRは精密成形が可能なため、医療機器、自動車部品、電子機器に選ばれています。医療や自動車セグメントでは、高品質で耐久性のある材料への需要が高まっており、LSRの優れた特性が活かされています。2032年までに37億米ドルに達すると予想される電気・電子機器用途セグメントは、2024~2032年にかけて顕著な成長を遂げようとしています。この急成長の背景には、絶縁、シール、電子部品の保護など、シリコーンエラストマーへの依存度が高まっていることがあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2023年 |

| 予測年 | 2024~2032 |

| 開始価格 | 128億米ドル |

| 予想価格 | 235億米ドル |

| CAGR | 6.4% |

シリコーンエラストマーの需要は、熱安定性、電気絶縁性、湿気や化学品などの環境問題に対する回復力を備えた材料へのニーズによって支えられています。北米のシリコーンエラストマー市場は、2032年までに42億米ドルを超えると予測され、2024~2032年のCAGRは6%を記録するとみられています。同地域の自動車、医療、エレクトロニクスの各セグメントは確立されており、シリコーンエラストマーの需要を牽引する極めて重要な役割を担っています。北米、特に米国におけるシリコーンエラストマー市場の成長を後押ししている重要な要因は、先進医療機器や生体適合材料への注目によって、医療セグメントでのシリコーンエラストマーの採用が加速していることです。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- 主要メーカー

- 流通業者

- 産業全体の利益率

- 産業への影響要因

- 促進要因

- 市場課題

- 市場機会

- 新たな機会

- 成長可能性分析

- 原料情勢

- 製造動向

- 技術の進化

- サステイナブル製造

- グリーンプラクティス

- 脱炭素化

- サステイナブル製造

- 原料の持続可能性

- 価格動向(地域別)(米ドル/トン)

- 規制と市場への影響

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 企業シェア分析

- 企業のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場規模・予測:製品別、2021~2032年

- 主要動向

- HTV

- RTV

- LSR

第6章 市場規模・予測:用途別、2021~2032年

- 主要動向

- 電気・電子

- 自動車・輸送機器

- 産業機械

- 消費財

- 建設

- その他

第7章 市場規模・予測:地域別、2021~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他の中東・アフリカ

第8章 企業プロファイル

- China National BlueStar(Group)Co., Ltd.

- The Dow Chemical Company

- KCC Corporation

- Mesgo S.P.A.

- Momentive Performance Materials Inc.

- Shin-Etsu Chemical Co., Ltd.

- Reiss Manufacturing Inc.

- Wacker Chemie AG

- Zhejiang Xinan Chemical Industrial Group Co., Ltd.

- Stockwell Elastomerics

- Specialty Silicone Products, Inc.

- Elkem ASA

- Avantor, Inc.

- Nano Tech Chemical Brothers Pvt. Ltd.

- Silicone Engineering Ltd.

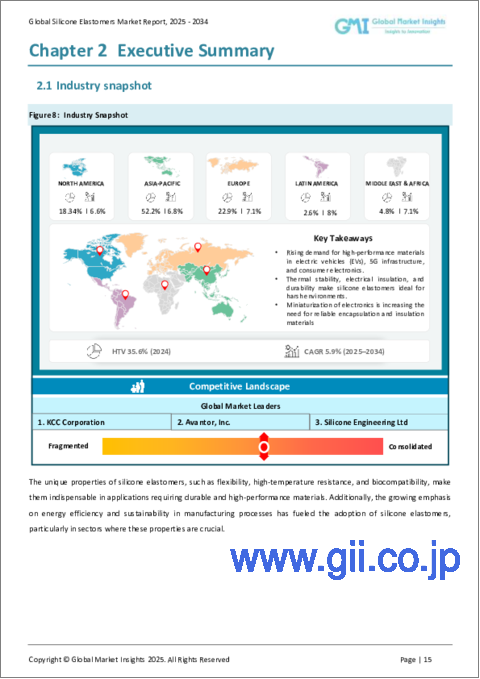

The Global Silicone Elastomers Market was valued at USD 12.8 billion in 2023, and projections indicate a CAGR of 6.4% from 2024 to 2032. This growth is largely attributed to surging demand across diverse sectors, notably automotive, electronics, healthcare, and construction. Additionally, heightened collaborations among major industry players further bolster market demand. Through 2032, the industry is set to experience robust growth, primarily fueled by the escalating adoption of silicone elastomers in medical devices and healthcare applications. This trend is spurring leading industries to ramp up production, thereby bolstering market demand.

The inherent biocompatibility, chemical resistance, and flexibility of silicone elastomers render them ideal for diverse medical applications, spanning implants, catheters, and seals. Given the healthcare sector's emphasis on advanced, durable materials, a significant uptick in demand for silicone elastomers is on the horizon. Moreover, the burgeoning applications of silicone elastomers in areas like wearable technology and 3D printing further amplify market growth. The overall industry is classified based on product, application, and region.

Forecasted to surpass USD 8 billion by 2032, the liquid silicone rubber (LSR) segment is set to gain substantial momentum from 2024 to 2032, thanks to its versatility and processing ease. LSR's precision molding capabilities make it a preferred choice for medical devices, automotive components, and electronics. This segment's expansion is further fueled by the healthcare and automotive sectors' growing appetite for high-quality, durable materials, where LSR's distinct properties shine. Anticipated to hit USD 3.7 billion by 2032, the electricals and electronics application segment is gearing up for notable growth from 2024 to 2032. This surge is driven by the escalating dependence on silicone elastomers for insulation, sealing, and safeguarding electronic components.

| Market Scope | |

|---|---|

| Start Year | 2023 |

| Forecast Year | 2024-2032 |

| Start Value | $12.8 Billion |

| Forecast Value | $23.5 Billion |

| CAGR | 6.4% |

The sector's demand for silicone elastomers is underpinned by the need for materials boasting thermal stability, electrical insulation, and resilience against environmental challenges like moisture and chemicals. Projected to surpass USD 4.2 billion by 2032, the North America silicone elastomers market is set to register a 6% CAGR from 2024 to 2032. The region's automotive, healthcare, and electronics sectors, being well-established, play a pivotal role in driving the demand for silicone elastomers. A significant factor propelling this market growth in North America, especially in the U.S., is the heightened adoption of silicone elastomers in healthcare, spurred by a focus on advanced medical devices and biocompatible materials.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Key manufacturers

- 3.1.2 Distributors

- 3.1.3 Profit margins across the industry

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Market challenges

- 3.2.3 Market opportunity

- 3.2.3.1 New opportunities

- 3.2.3.2 Growth potential analysis

- 3.3 Raw material landscape

- 3.3.1 Manufacturing trends

- 3.3.2 Technology evolution

- 3.3.2.1 Sustainable manufacturing

- 3.3.2.1.1 Green practices

- 3.3.2.1.2 Decarbonization

- 3.3.2.1 Sustainable manufacturing

- 3.3.3 Sustainability in raw materials

- 3.3.4 Pricing trend, by Region (USD/Ton)

- 3.3.4.1 North America

- 3.3.4.2 Europe

- 3.3.4.3 Asia Pacific

- 3.3.4.4 Latin America

- 3.3.4.5 Middle East & Africa

- 3.4 Regulations & market impact

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Company market share analysis

- 4.2 Company positioning matrix

- 4.3 Strategy outlook matrix

Chapter 5 Market Size and Forecast, By Product, 2021-2032 (USD Million, Kilo Tons)

- 5.1 Key trends

- 5.2 HTV

- 5.3 RTV

- 5.4 LSR

Chapter 6 Market Size and Forecast, By Application, 2021-2032 (USD Million, Kilo Tons)

- 6.1 Key trends

- 6.2 Electrical & electronics

- 6.3 Automotive & transportation

- 6.4 Industrial machinery

- 6.5 Consumer goods

- 6.6 Construction

- 6.7 Others

Chapter 7 Market Size and Forecast, By Region, 2021-2032 (USD Billion, Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 MEA

- 7.6.1 Saudi Arabia

- 7.6.2 UAE

- 7.6.3 South Africa

- 7.6.4 Rest of MEA

Chapter 8 Company Profiles

- 8.1 China National BlueStar (Group) Co., Ltd.

- 8.2 The Dow Chemical Company

- 8.3 KCC Corporation

- 8.4 Mesgo S.P.A.

- 8.5 Momentive Performance Materials Inc.

- 8.6 Shin-Etsu Chemical Co., Ltd.

- 8.7 Reiss Manufacturing Inc.

- 8.8 Wacker Chemie AG

- 8.9 Zhejiang Xinan Chemical Industrial Group Co., Ltd.

- 8.10 Stockwell Elastomerics

- 8.11 Specialty Silicone Products, Inc.

- 8.12 Elkem ASA

- 8.13 Avantor, Inc.

- 8.14 Nano Tech Chemical Brothers Pvt. Ltd.

- 8.15 Silicone Engineering Ltd.