|

市場調査レポート

商品コード

1797838

外来手術センターの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Ambulatory Surgical Centers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 外来手術センターの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年07月28日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

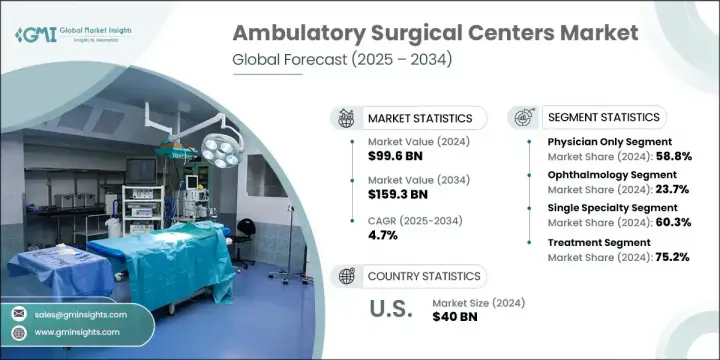

世界の外来手術センター市場は、2024年に996億米ドルと評価され、CAGR 4.7%で成長し、2034年には1,593億米ドルに達すると推定されています。

この堅調な成長は、ASCで実施される外科手術の増加、がん、糖尿病、肥満などの慢性疾患の有病率の上昇、支援的な償還政策など、いくつかの主要な要因に起因しています。ASCは外来患者向けのヘルスケア施設で、患者に即日手術という利便性を提供し、人気の高い選択肢となっています。費用対効果に優れ、利用しやすく、利便性の高いヘルスケアソリューションへの需要が高まるにつれ、これらのセンターは医師にとって魅力的な選択肢となりつつあります。

外来手術センター(ASC)市場の成長には、がん、糖尿病、肥満などの慢性疾患の増加が大きく寄与しています。これらの疾患は定期的な外科的介入を必要とし、外来手術に対する安定した需要を生み出しています。これと並行して、診療報酬体系の改善や外来診療に対するインセンティブなど、政府の好意的な政策がこの分野の成長を後押ししています。費用対効果が高く効率的なヘルスケアサービスを奨励する政策は、従来の病院環境からより手頃なASC代替施設へのシフトをさらに加速させています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 996億米ドル |

| 予測金額 | 1,593億米ドル |

| CAGR | 4.7% |

2024年に市場の58.8%を占めた医師主導型セグメントは、ヘルスケア専門家に自律性を提供するため、依然として圧倒的な強さを誇っています。医師は、手術のスケジューリング、機器の選択、施設の管理など、診療の重要な側面をコントロールできるメリットがあります。このような自由度の高さは、医療の質を高めるだけでなく、医師に副収入をもたらすため、多くの医療従事者にとって非常に魅力的な選択肢となっています。

さらに、眼科分野は23.7%と最大のシェアを占めており、これは眼科手術、特に白内障除去に対する需要の高まりに牽引されています。レーシックや網膜手術のような一般的な眼科手術を受けるためにASCを選ぶ患者も多く、より手頃で効率的な外来治療へのシフトがこの成長をさらに後押ししています。

米国外来手術センター2024年の市場規模は400億米ドルで、2034年までのCAGRは3.5%と予想されています。この成長の主な原動力となっているのは、手術が外来に移行する傾向が強まっていることであり、従来の病院を拠点とする手術と比較して、費用対効果が高く便利な選択肢を患者に提供しています。この移行は、ヘルスケアの効率化をサポートするだけでなく、個別化されたタイムリーなケアに対する需要の高まりにも合致しています。

世界外来手術センター市場の主なプレーヤーとしては、AMSURG、ASD MANAGEMENT、Community Health Systems、Cura Day Surgery、Endeavor Health、HCA Healthcare、Mednation、Nova Medical Centers、Pediatrix、Physicians Endoscopy、Pinnacle III、Proliance SURGEONS、Ramsay Sante、Regent Surgical、SCA HEALTH、SURGCENTER DEVELOPMENT、SURGERY PARTNERS、Surgical Management Professionals、Tenet Health、Trias MDなどが挙げられます。外来手術センター分野の企業は、市場での地位を強化するため、ネットワークの拡大と業務効率の向上に注力しています。戦略としては、ヘルスケアプロバイダーとのパートナーシップの構築、患者ケア向上のための先端技術への投資、特殊な外科手術の統合によるサービス提供の強化などが挙げられます。さらに企業は、患者の転帰を改善しながら費用対効果の高い治療を重視する、価値に基づくケアモデルの活用を目指しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患の有病率の増加

- 外科手術件数の増加

- 有利な償還と政府の政策

- ASCでは病院よりも感染リスクが低い

- 業界の潜在的リスク&課題

- 医療機器の高コスト

- 医師と患者の比率が低い

- 市場機会

- 入院から外来への移行

- ASC手術におけるAIとロボットの統合

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- ASCの歴史的タイムライン

- 将来の市場動向

- 消費者行動分析

- 償還シナリオ

- ポーター分析

- PESTEL分析

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 米国

- 欧州

- 世界のその他の地域(RoW)

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:所有権別、2021-2034

- 主要動向

- 医師のみ

- 病院のみ

- 法人のみ

- 医師と病院

- 医師と企業

- その他の所有権の種類

第6章 市場推計・予測:手術の種類別、2021-2034

- 主要動向

- 眼科

- 内視鏡検査

- 整形外科

- 神経学

- 疼痛管理

- 形成外科

- 足病学

- 耳鼻科

- 産科・婦人科

- 歯科

- その他の手術の種類

第7章 市場推計・予測:専門分野別、2021-2034

- 主要動向

- 単一の専門分野

- 多専門分野

第8章 市場推計・予測:サービス別、2021-2034

- 主要動向

- 治療

- 診断

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AMSURG

- ASD MANAGEMENT

- Community Health Systems

- Cura Day Surgery

- Endeavor Health

- HCA Healthcare

- Mednation

- Nova Medical Centers

- Pediatrix

- Physicians endoscopy

- Pinnacle III

- Proliance SURGEONS

- Ramsay Sante

- Regent Surgical

- SCA HEALTH

- SURGCENTER DEVELOPMENT

- SURGERY PARTNERS

- Surgical Management Professionals

- Tenet Health

- Trias MD

The Global Ambulatory Surgical Centers Market was valued at USD 99.6 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 159.3 billion by 2034. This robust growth can be attributed to several key factors, including the increasing number of surgical procedures conducted in ASCs, the rising prevalence of chronic diseases such as cancer, diabetes, and obesity, and supportive reimbursement policies. ASCs are outpatient healthcare facilities that offer patients the convenience of same-day surgeries, making them a popular choice. As the demand for cost-effective, accessible, and convenient healthcare solutions increases, these centers are becoming an attractive option for physicians, as they not only provide a source of additional income but also enable better control over care delivery.

The increasing prevalence of chronic diseases, such as cancer, diabetes, and obesity, is significantly contributing to the growth of the ambulatory surgical center (ASC) market. These conditions require regular surgical interventions, creating a steady demand for outpatient procedures. Alongside this, favorable government policies, including improved reimbursement structures and incentives for outpatient care, are bolstering the sector's growth. Policies that encourage cost-effective and efficient healthcare services are further accelerating the shift from traditional hospital settings to more affordable ASC alternatives.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $99.6 Billion |

| Forecast Value | $159.3 Billion |

| CAGR | 4.7% |

The physician-led segment, which captured 58.8% of the market in 2024, remains a dominant force due to the autonomy it offers healthcare professionals. Physicians benefit from the ability to control essential aspects of their practice, such as surgical scheduling, equipment selection, and facility management. This level of flexibility not only enhances the quality of care but also provides physicians with an additional income stream, making it a highly attractive option for many in the medical field.

Furthermore, the ophthalmology segment holds the largest share of 23.7%, driven by the growing demand for eye surgeries, particularly cataract removal. The shift towards more affordable and efficient outpatient treatments is further fueling this growth, with many patients opting for ASCs to undergo common eye procedures like LASIK and retinal surgeries.

United States Ambulatory Surgical Centers Market was valued at USD 40 billion in 2024 and is expected to grow at a CAGR of 3.5% through 2034. The key driver behind this growth is the increasing trend of surgeries moving to outpatient settings, which provides patients with more cost-effective and convenient alternatives compared to traditional hospital-based surgeries. This transition not only supports healthcare efficiency but also aligns with the growing demand for personalized, timely care.

Key players in the Global Ambulatory Surgical Centers Market include AMSURG, ASD MANAGEMENT, Community Health Systems, Cura Day Surgery, Endeavor Health, HCA Healthcare, Mednation, Nova Medical Centers, Pediatrix, Physicians Endoscopy, Pinnacle III, Proliance SURGEONS, Ramsay Sante, Regent Surgical, SCA HEALTH, SURGCENTER DEVELOPMENT, SURGERY PARTNERS, Surgical Management Professionals, Tenet Health, and Trias MD. To strengthen their position in the market, companies in the ambulatory surgical centers sector focus on expanding their networks and improving operational efficiency. Strategies include forging partnerships with healthcare providers, investing in advanced technologies to improve patient care, and enhancing their service offerings by integrating specialized surgical procedures. Additionally, firms aim to leverage value-based care models, which emphasize cost-effective treatment while improving patient outcomes.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Ownership trends

- 2.2.3 Surgery type trends

- 2.2.4 Specialty type trends

- 2.2.5 Service trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Rise in number of surgical procedures

- 3.2.1.3 Favorable reimbursements and government policies

- 3.2.1.4 Lower risk of infections in ASCs than hospitals

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs of medical devices

- 3.2.2.2 Low physician-to-patient ratio

- 3.2.3 Market opportunities

- 3.2.3.1 Shift from inpatient to outpatient settings

- 3.2.3.2 Integration of AI and robotics in ASC surgeries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Historical timeline of ASCs

- 3.7 Future market trends

- 3.8 Consumer behaviour analysis

- 3.9 Reimbursement scenario

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.2.1 U.S.

- 4.2.3 Europe

- 4.2.4 Rest of the world (RoW)

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Ownership, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Physician only

- 5.3 Hospital only

- 5.4 Corporate only

- 5.5 Physician and hospital

- 5.6 Physician and corporate

- 5.7 Other ownership types

Chapter 6 Market Estimates and Forecast, By Surgery Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Ophthalmology

- 6.3 Endoscopy

- 6.4 Orthopedic

- 6.5 Neurology

- 6.6 Pain management

- 6.7 Plastic Surgery

- 6.8 Podiatry

- 6.9 Otolaryngology

- 6.10 Obstetrics / Gynecology

- 6.11 Dental

- 6.12 Others surgery types

Chapter 7 Market Estimates and Forecast, By Specialty Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Single specialty

- 7.3 Multi specialty

Chapter 8 Market Estimates and Forecast, By Service, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Treatment

- 8.3 Diagnosis

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AMSURG

- 10.2 ASD MANAGEMENT

- 10.3 Community Health Systems

- 10.4 Cura Day Surgery

- 10.5 Endeavor Health

- 10.6 HCA Healthcare

- 10.7 Mednation

- 10.8 Nova Medical Centers

- 10.9 Pediatrix

- 10.10 Physicians endoscopy

- 10.11 Pinnacle III

- 10.12 Proliance SURGEONS

- 10.13 Ramsay Sante

- 10.14 Regent Surgical

- 10.15 SCA HEALTH

- 10.16 SURGCENTER DEVELOPMENT

- 10.17 SURGERY PARTNERS

- 10.18 Surgical Management Professionals

- 10.19 Tenet Health

- 10.20 Trias MD