|

市場調査レポート

商品コード

1913431

診断用超音波の市場機会、成長要因、業界動向分析、および2026年から2035年までの予測Diagnostic Ultrasound Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 診断用超音波の市場機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月21日

発行: Global Market Insights Inc.

ページ情報: 英文 149 Pages

納期: 2~3営業日

|

概要

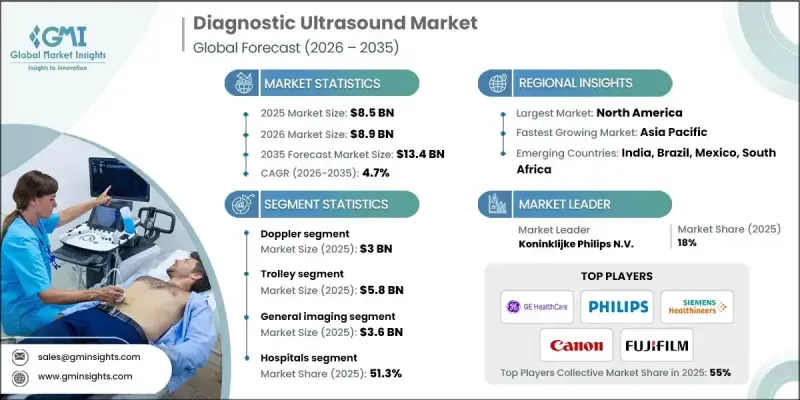

世界の診断用超音波市場は、2025年に85億米ドルと評価され、2035年までにCAGR 4.7%で成長し、134億米ドルに達すると予測されています。

市場成長は、先進国・新興国双方における高齢人口の増加、慢性疾患の蔓延拡大、特定国における出生率の上昇、超音波装置の継続的な技術革新など、複数の要因によって牽引されています。診断用超音波は、超高周波音波を用いて内臓の高解像度画像を生成する非侵襲的画像技術です。腹部、心臓、筋骨格系、その他の身体部位の検査に広く活用されています。特に妊娠中の胎児モニタリングや生検などの低侵襲処置のガイドとして高く評価されています。心血管疾患、がん、その他の慢性疾患の増加により、安全で費用対効果の高い画像診断ソリューションへの需要が高まっています。携帯型およびポイントオブケア超音波システムの開発により、病院や外来診療環境でのアクセス性が向上し、迅速なリアルタイム診断が可能となり、効率性と患者アウトカムの両方が向上しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 85億米ドル |

| 予測金額 | 134億米ドル |

| CAGR | 4.7% |

ドップラーセグメントは2025年に30億米ドルに達しました。ドップラー超音波は、音波の周波数変化を検出することで血管内の血流を測定する特殊なモダリティです。カラードップラー、パワードップラー、スペクトルドップラーなどの形式があり、心血管、血管、産科分野で広く使用され、重要なリアルタイムの血行動態情報を提供します。心血管疾患の診断、胎児の健康状態のモニタリング、血管状態の評価におけるその役割が、診断用超音波市場における優位性を支えています。

トロリーセグメントは2025年に58億米ドルに達しました。トロリーベースの超音波システムは、病院や診断センターでの包括的な使用を目的とした、従来の台車搭載型装置です。複数のトランスデューサーと、ドップラー、3D/4D、造影超音波などの高度な画像機能を備えており、詳細な画像診断とシームレスなワークフロー統合を必要とする高負荷環境において理想的なシステムです。

北米診断用超音波市場は2025年に33.8%のシェアを占めました。同地域のシェアは、先進的な医療インフラ、革新的な画像技術の早期導入、主要メーカーの存在によって支えられています。確立された償還政策、画像診断施設への継続的な投資、そして心臓病学、産科、救急医療における超音波の活用拡大が、同地域の強固な市場ポジションに寄与しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 先進国および発展途上地域における高齢人口の増加傾向

- 慢性疾患の発生率増加

- 発展途上国における出生率の増加

- 診断用超音波装置における技術革新と進歩

- 業界の潜在的リスク&課題

- 特に発展途上地域および未開発地域における熟練専門家の不足

- 発展途上経済圏における診断用超音波検査の普及を阻害する障壁

- 市場機会

- 人工知能(AI)と先進的画像技術の統合

- 予防医療および一次医療における応用拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術的進歩

- 現在の技術動向

- 新興技術

- サプライチェーン分析

- 償還シナリオ

- 価格分析、2025

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携および共同事業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:技術別、2022-2035

- 2D

- 3Dおよび4D

- ドップラー

第6章 市場推計・予測:携帯性別、2022-2035

- トロリー

- コンパクト/ハンドヘルド

第7章 市場推計・予測:用途別、2022-2035

- 一般画像診断

- 心臓病学

- 産婦人科

- その他のアプリケーション

第8章 市場推計・予測:最終用途別、2022-2035

- 病院

- 産科センター

- その他の用途

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Alpinion Medical Systems

- Butterfly Network

- Canon Medical Systems Corporation

- CHISON Medical Technologies

- Clarius Mobile Health

- Esaote SpA

- FujiFilm Holdings Corporation

- General Electric Company(GE Healthcare)

- Hologic, Inc.

- Konica Minolta Inc.

- Koninklijke Philips N.V.(BioTelemetry, Inc.)

- Samsung Electronics Co. Ltd.

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- Siemens Healthineers AG

- SonoScape