|

市場調査レポート

商品コード

1928917

ケーブル故障探知機市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Cable Fault Locator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| ケーブル故障探知機市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月09日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

概要

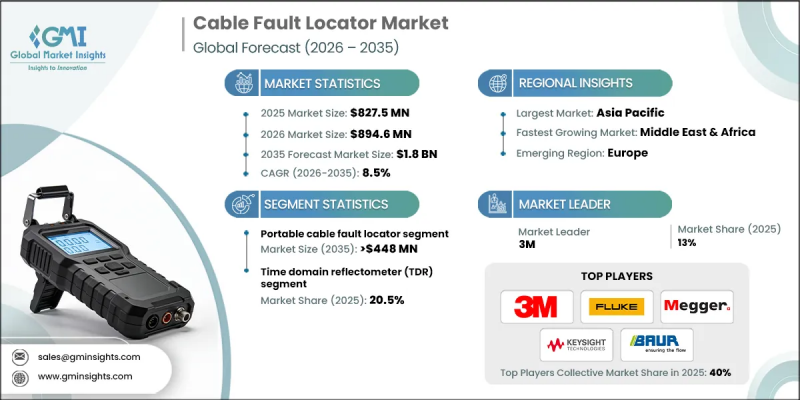

ケーブル故障探知機市場は、2025年に8億2,750万米ドルと評価され、2035年までにCAGR8.5%で成長し、18億米ドルに達すると予測されています。

市場成長の原動力は、先進国・発展途上国を問わず、信頼性が高く、耐障害性に優れ、効率的な電力ネットワークの構築が重視される傾向にあります。電力消費量の増加と送電網構造の複雑化に伴い、電力会社や産業オペレーターは、サービス中断の削減と運用継続性の向上に寄与する技術を優先的に導入しています。ケーブル故障探知機は、故障の迅速な特定・位置特定に不可欠なツールとして広く認知されており、停電時間の短縮と保守コストの削減に貢献します。電力インフラ近代化への世界の投資も市場成長をさらに後押ししており、特に電力ネットワークがより高い負荷と再生可能エネルギー統合に対応するために進化する中で顕著です。業界は、労働集約的な故障検出方法から、自動化され、デジタル技術を活用した予測型ソリューションへと移行しつつあります。こうした技術的進歩により、ケーブル故障探知機はインテリジェントな診断システムへと変貌を遂げており、精度向上、対応時間の短縮、電力網全体の性能向上を実現すると同時に、長期的な運用コストの削減に貢献しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 8億2,750万米ドル |

| 予測金額 | 18億米ドル |

| CAGR | 8.5% |

携帯型ケーブル故障探知機セグメントは、柔軟で導入が容易なソリューションに対する強い需要に支えられ、2035年までに4億4,800万米ドルに達すると予測されています。携帯型システムは、迅速な現場診断と即時トラブルシューティングを支援する能力が高く評価されており、故障後のサービス復旧を迅速に行う上で不可欠です。様々な運用環境に対応できる適応性により、効率的な保守ソリューションを求める公益事業、サービスプロバイダー、産業ユーザーの間での採用が増加しています。

時間領域反射計(TDR)技術セグメントは、2025年に20.5%のシェアを占め、2035年までCAGR8%で成長すると予測されています。都市開発の進展と地下ケーブル敷設の拡大により、正確で非侵襲的な故障検出の必要性が高まっています。この技術は物理的な掘削を伴わずに正確な故障位置を特定でき、より複雑な診断手段と比較して携帯性、コスト効率、操作の容易さが評価されています。

米国ケーブル故障位置検出器市場は、2035年までに6億3,900万米ドルに達すると予測されています。同国は広範な送配電網を有し、送電網の信頼性と耐障害性向上に継続的に注力しているため、世界の需要の主要な牽引役となっています。電力インフラの規模と複雑性は、先進的な故障検出・監視技術の強力な導入を今後も推進し続けるでしょう。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 原材料の入手可能性に関する状況

- バリューチェーンに影響を与える要因

- ディスラプション

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

- 新たな機会と動向

- 投資分析と将来展望

第4章 競合情勢

- イントロダクション

- 地域別における当社の市場シェア

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 戦略的取り組み

- 競合ベンチマーキングの図解

- 戦略ダッシュボード

- イノベーションと技術動向

第5章 市場規模・予測:タイプ別、2022-2035

- ポータブルケーブル故障探知機

- ハンドヘルドケーブル故障探知機

- 卓上型ケーブル故障探知機

- 車載型ケーブル故障探知機

- 据え置き型ケーブル故障探知機

- その他

第6章 市場規模・予測:技術別、2022-2035

- 時間領域反射計(TDR)

- ブリッジ回路

- 容量測定

- パルスエコー法

- 周波数領域反射法(FDR)

- 部分放電法

- ループ試験法

- その他

第7章 市場規模・予測:用途別、2022-2035

- 地下ケーブル

- 架空ケーブル

- 海底ケーブル

- 屋内配線

- その他

第8章 市場規模・予測:ケーブルタイプ別、2022-2035

- 電力ケーブル

- 光ファイバーケーブル

- 同軸ケーブル

- ツイストペアケーブル

- その他

第9章 市場規模・予測:最終用途別、2022-2035

- 電力産業

- 電気通信

- 鉱業

- 交通機関

- 石油・ガス

- 建設

- 航空宇宙・防衛

- 船舶

- データセンター

- 住宅用

- 商業用

- その他

第10章 市場規模・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋地域

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第11章 企業プロファイル

- 3M

- AFL

- BAUR GmbH

- Edgcumbe Instruments Ltd.

- ETL Systems

- Exfo Inc.

- Fluke Corporation

- Greenlee(Textron Inc.)

- HIOKI E.E. Corporation

- Hubbell Incorporated

- Keysight Technologies

- KomShine Technologies Limited

- Megger

- Metrotech Corporation

- Nanjing Dajiang Electronic Equipment Co., Ltd.

- Radiodetection Ltd.

- Ripley Tools LLC

- SebaKMT

- Sumitomo Electric Lightwave

- Telemetrics Equipments Private Limited

- Tempo Communications

- Tessco Technologies

- Trotec

- VIAVI Solutions Inc.

- Yokogawa Electric Corporation