|

市場調査レポート

商品コード

1982355

宇宙ロボットの市場機会、成長要因、業界動向分析、および2026年~2035年の予測Space Robotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 宇宙ロボットの市場機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年02月18日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

概要

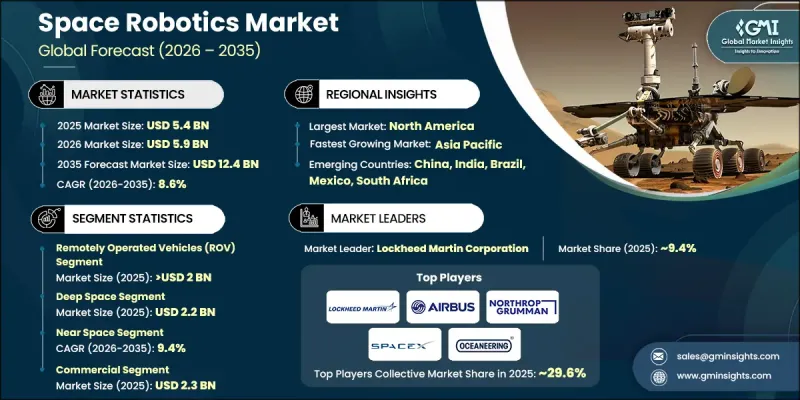

世界の宇宙ロボット市場は、2025年に54億米ドルと評価され、CAGR 8.6%で成長し、2035年までに124億米ドルに達すると推定されています。

宇宙ミッションの複雑さと規模が拡大するにつれ、この分野は拡大しており、多様な地球外環境下で動作可能な高度なロボット技術や自動化技術への需要が生まれています。宇宙機関や民間企業は、深宇宙での長期ミッションを支援し、宇宙飛行士への依存度を低減し、運用効率を向上させるためのロボットシステムを開発しています。これらのシステムは、宇宙空間での整備、組み立て、惑星探査など、多岐にわたる用途向けに設計されており、より頻繁で複雑かつ費用対効果の高いミッションを可能にします。宇宙プログラムへのロボット技術の統合により、リアルタイムの監視、タスクの自動実行、そして人的リソースに過度の負担をかけることとなるミッション支援が可能になります。政府、研究機関、民間企業が一体となってイノベーションを推進しており、ロボット技術が将来の宇宙運用において極めて重要な役割を果たすことを確実なものとしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 54億米ドル |

| 予測金額 | 124億米ドル |

| CAGR | 8.6% |

遠隔操作車両(ROV)セグメントは、宇宙探査、軌道上の点検、惑星探査ローバー、および宇宙ステーションの運用において重要な役割を果たしていることから、2025年には20億米ドルに達しました。ROVは、危険な環境やアクセス困難な環境において遠隔作業を行うことができる多目的プラットフォームとして機能し、リアルタイム制御と自律機能の両方を活用して、地表探査、サンプル採取、および軌道上でのメンテナンスを支援しています。

商業セグメントは、衛星展開、宇宙旅行、軌道上製造、および商業ステーションに従事する民間宇宙企業の急速な拡大に牽引され、2025年には23億米ドルに達しました。商業宇宙ロボット工学は、衛星管理、打ち上げ運用、点検、および保守に広く応用されており、拡張性が高くコスト効率の良い運用を可能にしています。強力な民間投資、打ち上げ頻度の増加、および技術革新により、商業ミッション全体での採用がさらに加速しています。

2025年、北米の宇宙ロボット市場は38.5%のシェアを占めました。同地域の成長は、多額の政府資金、堅調な宇宙探査プログラム、防衛関連の取り組み、および宇宙インフラへの投資によって支えられています。北米の政府機関や企業は、長期的なプログラムを活用して先進的なロボットプラットフォームを開発しており、宇宙ロボット技術における同地域のリーダーシップを強化しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 衛星コンステレーションおよび深宇宙ミッションの拡大

- 自律型およびAIを活用した宇宙運用への需要の高まり

- 宇宙観光および商業宇宙活動の成長

- 宇宙プログラムにおける官民連携の拡大

- 軌道上サービス、宇宙ゴミ除去、および衛星メンテナンスの必要性

- 業界の潜在的リスク&課題

- 高い開発コストと技術的な複雑さ

- 過酷かつ予測不可能な宇宙環境における運用リスク

- 市場機会

- 宇宙ミッションにおける自律型ロボットシステムの導入拡大

- 軌道上サービス・組立・製造(ISAM)に対する需要の高まり

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新興ビジネスモデル

- コンプライアンス要件

- 地政学的および貿易動向

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績の比較

- 売上高

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインの幅

- 技術

- イノベーション

- 地域別展開の比較

- 世界展開の分析

- サービスネットワークのカバー率

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- チャレンジャー

- フォロワー

- ニッチプレイヤー

- 財務実績の比較

- 主な発展, 2022-2025

- 合併・買収

- パートナーシップおよび提携

- 技術的進歩

- 事業拡大および投資戦略

- デジタルトランスフォーメーションの取り組み

- 新興/スタートアップ競合企業の動向

第5章 市場推計・予測:ソリューション別、2022-2035

- 遠隔操作車両(ROV)

- ローバー/宇宙船着陸機

- 宇宙探査機

- その他

- 遠隔操作システム(RMS)

- ロボットアーム/マニピュレーターシステム

- 把持・ドッキングシステム

- その他

- ソフトウェア

- サービス

第6章 市場推計・予測:技術別、2022-2035

- リモートセンシング

- 自律システム

- 遠隔操作

- ロボットソフトウェア

- 人工知能(AI)および機械学習(ML)

- 人間とロボットの相互作用

第7章 市場推計・予測:用途別、2022-2035

- 深宇宙

- 惑星探査

- 小惑星採掘

- 宇宙調査

- 近宇宙

- 衛星運用

- 宇宙ステーションの保守

- 軌道輸送

- その他

- 地上

- 打ち上げ運用

- 地上管制運用

- 宇宙調査施設

第8章 市場推計・予測:エンドユーザー別、2022-2035

- 商業用

- 政府

- 防衛

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- 世界企業

- Airbus SE

- ITT Corporation

- Lockheed Martin Corporation

- MAXAR TECHNOLOGIES

- MDA Space

- Northrop Grumman

- SpaceX

- 地域プレイヤー

- Altius Space Machine

- Astrobotic Technology

- Astroscale Holdings Inc.

- Honeybee Robotics

- Intuitive Machines, LLC.

- Ispace

- Made In Space Inc.(Redwire LLC)

- Metecs, LLC.

- Oceaneering International, Inc.

- 地域/ニッチ企業

- BluHaptics, Inc.

- Motiv Space Systems, Inc.

- Olis Robotics