|

市場調査レポート

商品コード

1892814

超高精細パネル4K市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Ultra-High-Definition Panel 4K Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 超高精細パネル4K市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月15日

発行: Global Market Insights Inc.

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

概要

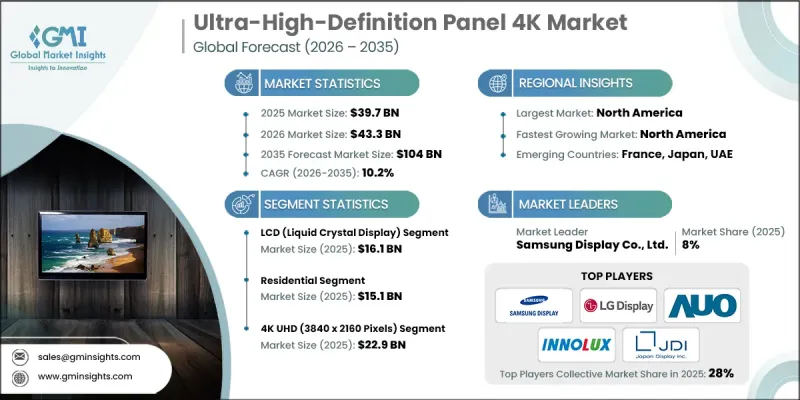

世界の超高精細パネル4K市場は、2025年に397億米ドルと推定され、2035年までにCAGR10.2%で成長し、1,040億米ドルに達すると予測されています。

市場の勢いは、消費者向けおよび商業環境において、より豊かな画質と没入感のあるデジタル体験を求める世界の潮流によって牽引されています。ディスプレイ技術における継続的な革新と、より鮮明な解像度や色精度への期待の高まりが相まって、需要パターンを再構築しています。メーカー各社は、大規模な製造工場と柔軟な地域密着型組立オペレーションの両方への投資を拡大し、生産サイクルの短縮とカスタマイズされたパネルソリューションの提供を進めています。この変革により、大量生産と精密さを追求した製造を可能とする先進的な製造システムへの需要が高まっています。ディスプレイ性能の基準値が上昇し続ける中、市場は次世代パネル構造と高効率コンポーネントの統合による恩恵も受けています。これらは輝度、コントラスト、電力最適化を向上させます。サプライチェーン全体における物流の効率化とモジュール式ディスプレイユニットの迅速な移動は、重要な競争上の差別化要因となりつつあります。これらの要因が相まって、4K UHDパネルは現代のデジタル視聴、エンターテインメント、プロフェッショナルディスプレイエコシステムを支える中核技術としての地位を確立しつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 397億米ドル |

| 予測金額 | 1,040億米ドル |

| CAGR | 10.2% |

液晶ディスプレイ(LCD)セグメントは2025年に161億米ドルの市場規模を記録しました。製造の拡張性、安定した視覚出力、コスト効率の高さがその優位性を支えており、幅広い画面サイズにおける大量生産の選択肢として引き続き選ばれています。

住宅セグメントは2025年に151億米ドルに達しました。日常の視聴体験やインタラクティブ体験を向上させる先進的なディスプレイソリューションの家庭への普及が需要を支えています。ホームエンターテインメント環境の継続的なアップグレードと旧式ディスプレイの買い替えが、長期的な成長を持続させています。

米国における超高精細パネル4K市場は、2025年に83%のシェアを占め、122億米ドル規模に達すると予測されます。同地域は、プレミアム消費者向け、ホスピタリティ、商業用途における堅調な需要に牽引され、2026年から2035年にかけて世界で最も高いCAGR11%を記録すると見込まれています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 4K/UHDコンテンツ及びストリーミングサービスの普及

- プレミアムおよび大型ディスプレイの急速な成長

- ゲーミングおよびeスポーツ市場の拡大

- スマートホームとAI機能の統合

- 業界の潜在的リスク&課題

- 先進的な製造工場における高額な設備投資(CapEx)

- 汎用LCDにおける過剰生産能力と価格下落

- 機会

- 先進パネル技術(OLED、QD-OLED、mini-LED)

- 新たな応用分野(自動車、IT)

- 促進要因

- 成長可能性分析

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 技術別

- 規制情勢

- 規格およびコンプライアンス要件

- 地域別規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:用途別、2022-2035

- 主要動向

- 民生用電子機器

- テレビ

- モニター

- ノートパソコン

- スマートフォン

- タブレット

- 商業用

- デジタルサイネージ

- ディスプレイウォール

- 広告ディスプレイ

- ヘルスケア

- 医療用画像表示装置

- 教育

- インタラクティブホワイトボード

- プロジェクター

- 自動車

- 車載ディスプレイ

- インフォテインメントシステム

- その他

第6章 市場推計・予測:技術別、2022-2035

- 主要動向

- 液晶ディスプレイ(LCD)

- LEDバックライト式液晶ディスプレイ

- 量子ドット(QLED)

- 有機EL(有機発光ダイオード)

- フレキシブルOLED

- リジッドOLED

- マイクロLED

- 直視型LED

- Mini LED

- その他

第7章 市場推計・予測:解像度別、2022-2035

- 主要動向

- 4K UHD(3840×2160ピクセル)

- 8K UHD(7680×4320ピクセル)

第8章 市場推計・予測:サイズ別、2022-2035

- 主要動向

- 40インチ未満

- 40~60インチ

- 60インチ以上

第9章 市場推計・予測:最終用途別、2022-2035

- 主要動向

- 住宅用

- 商業用

- 産業用

第10章 市場推計・予測:流通チャネル別、2022-2035

- 主要動向

- オンライン

- オフライン

第11章 市場推計・予測:地域別、2022-2035

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- ロシア

- ベルギー

- ポーランド

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- インドネシア

- マレーシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- Century Plyboards

- AU Optronics Corp.(AUO)

- BOE Technology Group Co., Ltd.

- Changhong Electric Co., Ltd.

- CSOT(China Star Optoelectronics Technology Co., Ltd.)

- Haier Group

- Hisense Group

- Innolux Corporation

- Japan Display Inc.

- LG Display Co., Ltd.

- Panasonic Corporation

- Philips(TPV Technology)

- Samsung Display Co., Ltd.

- Sharp Corporation

- Skyworth Group

- Sony Corporation

- TCL Technology

- Tianma Microelectronics Co., Ltd.

- ViewSonic Corporation

- Vizio Inc.

- Xiaomi Corporation