マスフローコントローラー市場における機会、成長要因、業界動向分析、および2026年から2035年までの予測

Mass Flow Controller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1959604

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

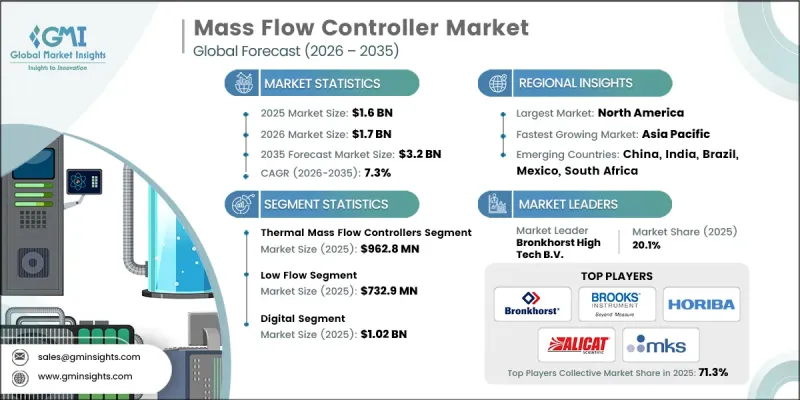

世界のマスフローコントローラー市場は、2025年に16億米ドルと評価され、2035年までにCAGR 7.3%で成長し、32億米ドルに達すると予測されています。

この成長は、半導体、航空宇宙、化学、エネルギー、製造などの産業分野における自動化および精密制御技術の採用拡大によって推進されています。工業プロセスがより複雑化し、生産量の需要が高まるにつれ、精密で信頼性の高い流量測定システムの必要性が強まっています。マスフローコントローラーは、ガスや液体の流量を正確に調節し、プロセスの安定性、品質の一貫性、安全基準の遵守を確保するために不可欠です。半導体製造および先進的な製造オペレーションの拡大が、市場をさらに加速させています。成膜、エッチング、化学気相成長などの重要プロセスでは、高い再現性とコンパクトな統合性が求められます。さらに、インダストリー4.0やスマート製造への移行が、デジタル対応かつIIoT互換のマスフローコントローラーの需要を牽引しており、リアルタイム監視、ダウンタイムの削減、運用効率の向上を実現することで、高精度産業全体におけるMFC導入の価値を最終的に強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 16億米ドル |

| 予測金額 | 32億米ドル |

| CAGR | 7.3% |

熱式質量流量コントローラー(Thermal MFC)セグメントは、2025年に9億6,280万米ドルの市場規模を生み出しました。これらのコントローラーは、半導体製造、化学製品生産、クリーンテクノロジー運用において精密な流量測定を維持できる能力により、市場を独占しています。熱式MFCは、厳しいプロセス環境下においても、迅速な応答時間、一貫した再現性、長期的な耐久性を提供します。様々な条件下でガス流量を正確に制御する能力は、重要なアプリケーションにおけるプロセス安定性と運用効率を維持するために不可欠です。

低流量セグメントは2025年に7億3,290万米ドルを占め、半導体製造、医薬品、分析プロセスにおける重要な用途により最大の市場シェアを維持しました。低流量MFCは高精度作業に好まれ、少量の液体やガスを調節する際の高速応答性、精度、再現性を提供します。これらの特性により、わずかな偏差でも品質や歩留まりに影響するプロセスにおいて不可欠な存在となっています。

北米マスフローコントローラ市場は、自動化、スマート製造、デジタルプロセス制御の高い導入率に牽引され、2025年に31.4%のシェアを占めました。半導体、化学、エネルギー、製薬などの産業セクターでは、IIoT対応MFC、予知保全、高度な分析を活用し、操業の最適化、ダウンタイムの削減、プロセス安定性の維持を図っています。エネルギー効率、持続可能性、規制順守への関心の高まりが、地域全体で信頼性の高い高精度マスフローコントローラーの需要をさらに押し上げております。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 半導体および電子機器製造の拡大

- デジタル化とインダストリー4.0技術の統合

- 再生可能エネルギーおよびクリーンテクノロジー応用分野の成長

- 医薬品、化学処理、バイオテクノロジー分野における拡大

- 地域別産業化と製造投資

- 業界の潜在的リスク&課題

- 高度なMFCの高コスト

- 既存システムとの複雑な統合

- 市場機会

- IoT対応およびスマートMFCソリューション

- 新興市場における拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新興ビジネスモデル

- コンプライアンス要件

- 地政学的・貿易動向

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオ比較

- 製品ラインの広さ

- 技術

- イノベーション

- 地理的プレゼンス比較

- 世界展開分析

- サービスネットワークのカバー率

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー企業

- 課題者

- フォロワー

- ニッチプレイヤー

- 財務実績比較

- 主な発展, 2022-2025

- 合併・買収

- 提携および共同事業

- 技術的進歩

- 拡大と投資戦略

- デジタルトランスフォーメーションの取り組み

- 新興/スタートアップ競合の動向

第5章 市場推計・予測:技術別、2022-2035

- 熱式質量流量計

- コリオリ式質量流量計

- 差圧式質量流量コントローラー

- 超音波式/新興マスフローコントローラー

第6章 市場推計・予測:接続方式別、2022-2035

- アナログ

- デジタル

第7章 市場推計・予測:媒体タイプ別、2022-2035

- ガス

- 液体

第8章 市場推計・予測:流量容量別、2022-2035

- 低流量

- 中流量

- 高流量

第9章 市場推計・予測:最終用途別、2022-2035

- 半導体・エレクトロニクス

- 化学気相成長(CVD)

- 物理的気相成長法(PVD)

- 熱処理・拡散

- その他

- 化学品・特殊化学品

- 化学反応制御

- スプレー・コーティングプロセス

- ガス混合・攪拌

- その他

- 環境・ユーティリティ

- 水処理・廃水処理

- 大気質モニタリング・排出ガス管理

- その他

- 医薬品・バイオテクノロジー

- エネルギー・先端材料

- 金属・鉱業

- 食品・飲料

- 航空宇宙・防衛

- 医療・ヘルスケア

- その他

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Alicat Scientific, Inc.

- Azbil Corporation

- Bronkhorst High-Tech B.V.

- Brooks Instrument

- Christian Burkert GmbH &Co. KG

- Fujikin Incorporated

- HORIBA Ltd.

- KOFLOC Corporation

- MKS Instruments, Inc.

- Parker Hannifin Corporation

- Sensirion AG

- Sierra Instruments, Inc.

- Teledyne Hastings Instruments

- Tokyo Keiso Co., Ltd.

- Vogtlin Instruments GmbH

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日