|

市場調査レポート

商品コード

1844343

LTEと5G NRベースのCBRSネットワークの市場機会と成長促進要因、産業動向分析、2025年~2034年の予測LTE and 5G NR-based CBRS Networks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| LTEと5G NRベースのCBRSネットワークの市場機会と成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年09月17日

発行: Global Market Insights Inc.

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

概要

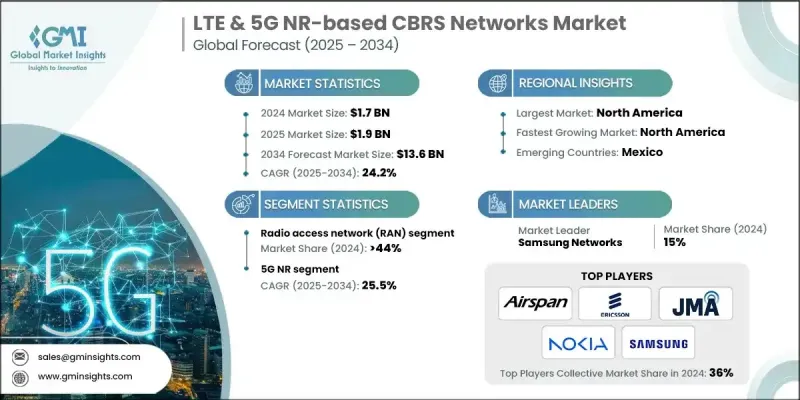

世界のLTE &5G NRベースCBRSネットワーク市場の2024年の市場規模は17億米ドルで、CAGR 24.2%で成長し、2034年には136億米ドルに達すると推定されます。

製造業、物流、港湾、大規模キャンパスなどの企業では、高速、低遅延、セキュアな通信に対するニーズの高まりに対応するため、プライベートLTEおよび5G NRネットワークへの注目が高まっています。CBRSは、3.5GHz帯(3550~3700MHz)のミッドバンド周波数へのアクセスを提供し、高価なライセンス周波数に代わる手頃な選択肢を企業に提供します。デジタルトランスフォーメーションが加速する中、CBRSを利用したプライベートセルラーネットワークの利用は拡大し続けています。企業は、キャンパスモビリティ、産業オートメーション、固定無線アクセス向けにカスタマイズされた無線ネットワークを展開することに明確なメリットを見出しています。各業界でトライアルや実運用が進んでおり、使用事例が検証され、CBRSネットワークのコスト効率が証明されています。市場の勢いは、ニュートラル・ホスト・ソリューション、屋内カバレッジ・アプリケーション、SASプロバイダーが管理する共有スペクトラム・アクセスの進化によってさらに後押しされています。連邦政府の調整、干渉リスク、コストに関する課題はあるもの、市場の見通しは依然として強いです。業界と規制当局の取り組みがこれらの障壁に対処し続ける一方、技術の進歩がより迅速な展開と幅広い企業採用を可能にしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 17億米ドル |

| 予測金額 | 136億米ドル |

| CAGR | 24.2% |

2024年、無線アクセスネットワーク(RAN)セグメントのシェアは44%。スモールセルやマクロセルの無線を含むRANコンポーネントは、屋内外で一貫したカバレッジを提供しながら、ユーザーデバイスをコアネットワークに接続するために不可欠です。サムスン、ノキア、エリクソンなどのベンダーが提供するハードウェアは、ビームフォーミングや動的な周波数割り当てなどの機能をサポートし、遅延を減らしながらネットワーク性能を向上させます。企業はRANシステムを利用して、集中的なトラフィックや低遅延アプリケーションに対応できるスケーラブルでセキュアなネットワークを構築しています。

5G NRセグメントは2034年までCAGR 25.5%で成長すると予測されています。このセグメントの好調な業績は、超低遅延、大容量、ネットワークスライシングのサポートを提供できることに起因しています。企業は、自律型システム、拡張現実、ロボット工学、スマートオートメーションなどの新技術のために、LTEよりも5G NRを好むようになっています。5G NRはまた、集中管理による効率的な周波数利用や、複数サイトにわたるシームレスなスケーリングもサポートしています。このため、将来対応可能なアーキテクチャを備えたパフォーマンス主導型のネットワークを求める業界にとって、特に魅力的なものとなっています。

米国LTE &5G NRベースのCBRSネットワーク市場は、2024年に7億2,550万米ドルを創出。FCCの構造化された周波数共有フレームワークは、3つのアクセス階層の下で連邦政府と商用ユーザーの共存を可能にしている:現職、優先アクセス・ライセンス(PAL)、一般認可アクセス(GAA)です。このモデルは、重要なユーザーの保護を維持しながら、企業がより柔軟に周波数を利用できるようにすることで、技術革新を促進します。大手通信事業者は、ネットワークのカバレッジを改善し、サービスの柔軟性を高め、共有周波数帯が容易に利用できる需要の高い地域のモバイルトラフィックをオフロードするために、CBRSベースのインフラを拡大するための投資を続けています。

LTE &5G NRベースのCBRSネットワーク市場を形成する主要企業には、Commscope、Nokia、Airspan、Comcast、JMA Wireless、Amazon Web Services、Cisco、Radisys、Samsung、Ericssonなどがあります。これらのプレーヤーは、ターンキー・プライベート・ネットワーク・ソリューションの立ち上げ、エッジ・コンピューティングとAI機能の統合、エコシステム・パートナーシップの拡大など、市場ポジションを強化するために的を絞った戦略を用いています。これらの企業は、集中管理と企業ITシステムとのシームレスな相互運用性を提供するソフトウェア定義プラットフォームに投資しています。また、干渉を最小限に抑え、配備を合理化することを目的として、周波数政策に影響を与え、SASの調整を改善するために、規制当局との協力に取り組んでいる企業もあります。各社の焦点は、進化する企業接続の需要に対応できる、堅牢でスケーラブル、かつアプリケーションにとらわれないCBRSソリューションの開発に変わりはないです。

よくあるご質問

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- グローバル

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予報

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- プライベートLTEおよび5G NRネットワークの採用増加

- ケーブル事業者によるCBRSスモールセルの導入増加

- ポータブルプライベート5Gソリューションへの投資

- SASとCBRS 2.0の進歩

- プライベートワイヤレスネットワークに対する企業の関心の高まり

- 業界の潜在的リスク&課題

- 連邦現職者への干渉

- 調整の複雑さと運用コスト

- 市場機会

- 成長する産業用IoTとエンタープライズキャンパスネットワーク

- MVNOオフロードとセカンダリキャリアアグリゲーション

- プライベート5Gソリューションとの統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術成熟度評価フレームワーク

- 現在の技術動向

- 新興技術

- コスト構造分析

- 特許分析

- 地域別特許出願(2021-2025)

- CBRS固有のSEPカテゴリ

- 主なニュースと取り組み

- 持続可能性とESG影響評価

- 環境影響分析と指標

- 社会的影響の考慮と指標

- ガバナンスとコンプライアンスのフレームワーク

- ESG投資の影響と財務への影響

- ユースケースとアプリケーション

- 最良のシナリオ

- 投資と資金調達の情勢

- CBRS/プライベート5Gにおけるベンチャーキャピタルおよびプライベートエクイティ投資

- 政府の助成金、優遇措置、補助金

- 資金提供が展開速度とイノベーションに与える影響

- 市場開拓と商業戦略

- サービスバンドル戦略(FWA、IoT、エンタープライズパッケージ)

- マーケティングと顧客獲得戦略

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:インフラサブマーケット別、2021年~2034年

- 主要動向

- 無線アクセスネットワーク(RAN)

- モバイルコア

- 交通網

- スモールセルRU(無線ユニット)

- 分散型および集中型ベースバンドユニット(DU/CU)

第6章 市場推計・予測:エアインターフェース技術, 2021-2034

- 主要動向

- LTE

- 5G NR

第7章 市場推計・予測:細胞別、2021年~2034年

- 主要動向

- 屋内スモールセル

- 屋外スモールセル

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- モバイルネットワークの高密度化

- 固定無線アクセス(FWA)

- ケーブル事業者と新規参入者

- 中立宿主

- プライベートセルラーネットワーク

- 教育

- 政府および地方自治体

- ヘルスケア

- 製造業

- 軍隊

- 鉱業

- 石油・ガス

- 小売・ホスピタリティ

- その他

第9章 市場推計・予測:周波数帯域別、2021年~2034年

- 主要動向

- 2.3GHz以下

- 2.3~2.6GHz

- 3.3~3.6GHz

- 3.55~3.7GHz

- 3.7~3.8GHz

- 3.8~4.2GHz

- 4.6~4.9GHz

- 20GHz以上

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- グローバル企業

- Airspan

- Amazon Web Services

- AT&T

- Charter Communications

- Cisco Systems

- Comcast

- CommScope

- Ericsson

- HPE

- Huawei

- Intel

- JMA Wireless

- Microsoft Azure

- NEC

- Nokia

- Qualcomm

- Samsung

- Sony

- T-Mobile

- Verizon Communications

- 地域有力企業

- ZTE

- Baicells

- Fujitsu

- 新興企業/破壊的イノベーション

- Altiostar

- Federated Wireless

- Mavenir

- Radisys