|

|

市場調査レポート

商品コード

1573693

遠隔てんかん市場、機会、成長促進要因、産業動向分析と予測、2024年~2032年Tele-epilepsy Market, Opportunity, Growth Drivers, Industry Trend Analysis and Forecast, 2024-2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 遠隔てんかん市場、機会、成長促進要因、産業動向分析と予測、2024年~2032年 |

|

出版日: 2024年08月26日

発行: Global Market Insights Inc.

ページ情報: 英文 230 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

遠隔てんかんの世界市場は、2023年に4億810万米ドルと評価され、2024年から2032年にかけて15.9%のCAGRで成長すると予測されています。

この成長の主な要因は、てんかんの有病率の上昇と遠隔管理ソリューションに対する需要の増加です。

遠隔医療に対する認識と受容の高まりに加え、政府の支援政策や有利な償還の枠組みが、遠隔てんかんサービスの採用を加速させると思われます。特に、メディケア・メディケイド・サービスセンター(CMS)は、てんかんを含む慢性疾患の遠隔医療受診が過去5年間で64%も急増したことを強調しており、遠隔医療への依存が高まっていることを裏付けています。

てんかんを発症しやすい高齢者層が拡大していることに加え、てんかん症例の一般的な増加も相まって、遠隔ヘルスケアソリューションへの需要が高まるにつれ、市場の成長が促進される見通しです。世界保健機関(WHO)は2023年、世界で約5,000万人がてんかんに罹患していると報告し、その中でも高齢者の割合が顕著であるとしました。この広範な有病率は、継続的なモニタリングと管理の必要性を際立たせ、効果的なケアを確保する上で高度な遠隔てんかん技術が極めて重要な役割を果たすことを強調しています。

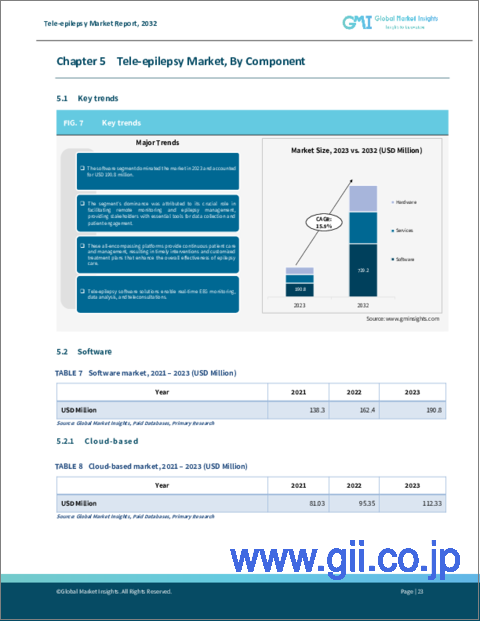

市場を構成要素別に分類すると、ソフトウェア、サービス、ハードウェアがあります。市場を独占するソフトウェア分野は、予測期間中にCAGR 16.2%で成長すると予測されています。ソフトウェア分野では、クラウドベースのソリューションとオンプレミスのソリューションが区別されます。ソフトウェアの市場優位性は、遠隔モニタリングとてんかん管理におけるその重要な機能に起因しており、利害関係者はデータ収集と患者参加に不可欠なツールを装備しています。これらのソフトウェアソリューションは、脳波のリアルタイムモニタリング、データ分析、遠隔コンサルティングを容易にし、継続的な患者ケア、タイムリーな介入、てんかん管理の有効性を高めるオーダーメイドの治療計画を実現します。

遠隔てんかん市場は、てんかんタイプ別に局所発作、全般発作、複合発作のカテゴリーに分類されます。2023年には、全般発作分野が59.7%のシェアを占め、市場を牽引しました。これは、全般発作の高い有病率と複雑な管理ニーズによるものです。全般発作は両脳半球に同時に影響を及ぼすため、継続的なモニタリングと定期的な治療調整が必要となることが多いです。

米国の遠隔てんかん市場は2023年に2億1,870万米ドルと評価され、2032年末までに7億9,550万米ドルに急増すると予測されています。この堅調な成長は、米国におけるてんかんの有病率の高さが、高度な管理ソリューションの需要を促進していることに起因しています。米国の優位性は、確立されたヘルスケアインフラと、遠隔診断から遠隔相談プラットフォームに至るまで、遠隔医療技術が広く受け入れられていることにあります。さらに、政府の支援策、有利な償還政策、絶え間ない技術の進歩により、米国は遠隔てんかん市場における優位な地位をさらに強固なものにしています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- てんかん有病率の上昇

- 遠隔モニタリングサービスへの需要の高まり

- 遠隔医療サービスの技術的進歩

- 患者や介護者の意識の高まり

- 業界の潜在的リスク&課題

- データセキュリティとプライバシーに関する懸念

- 促進要因

- 成長可能性分析

- 今後の市場動向

- 規制状況

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:コンポーネント別、2021年~2032年

- 主要動向

- ソフトウェア

- クラウドベース

- オンプレミス

- サービス

- 遠隔相談サービス

- 遠隔モニタリング・スクリーニング・サービス

- 遠隔教育およびトレーニング

- その他のサービス

- ハードウェア

第6章 市場推計・予測:てんかんタイプ別、2021年~2032年

- 主要動向

- 局所発作

- 全般発作

- 複合発作

第7章 市場推計・予測:年齢層別、2021年~2032年

- 主要動向

- 小児

- 成人

第8章 市場推計・予測:エンドユーザー別、2021年~2032年

- 主要動向

- ヘルスケアプロバイダー

- 病院・クリニック

- てんかん専門センター

- 在宅ケア環境

- 患者

- その他のエンドユーザー

第9章 市場推計・予測:地域別、2021年~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東とアフリカ

第10章 企業プロファイル

- Bioserenity SAS

- Ceribell, Inc.

- CortiCare, Inc.

- Epitel, Inc.

- Empatica Inc.

- MedaSync.

- Medtronic plc

- NeuroPace, Inc.

- Ovation Healthcare

- Real Time Tele-Epilepsy Consultants.

- ScienceSoft USA Corporation

- Seer Medical

- Teladoc Health, Inc.

- UCB S.A.

- Vidyo, Inc.

The Global Tele-Epilepsy Market was valued at USD 408.1 million in 2023 and is projected to grow at a CAGR of 15.9% from 2024 to 2032. This growth is primarily driven by the rising prevalence of epilepsy and an increasing demand for remote management solutions.

Heightened awareness and acceptance of telehealth, along with supportive government policies and favorable reimbursement frameworks, are set to accelerate the adoption of tele-epilepsy services. Notably, the Centers for Medicare and Medicaid Services (CMS) highlighted a significant 64% surge in telehealth visits for chronic conditions, including epilepsy, over the last five years, underscoring the growing reliance on remote healthcare.

The expanding elderly demographic, more prone to epilepsy, combined with a general uptick in epilepsy cases, is poised to drive market growth as the demand for remote healthcare solutions intensifies. The World Health Organization (WHO) reported in 2023 that around 50 million people globally are affected by epilepsy, with a notable portion being elderly. This widespread prevalence accentuates the necessity for ongoing monitoring and management, underscoring the pivotal role of advanced tele-epilepsy technologies in ensuring effective care.

The overall industry is divided into component, epilepsy type, age group, end-user, and region.

The market, segmented by component, includes software, services, and hardware. Dominating the market, the software segment is projected to grow at a CAGR of 16.2% during the forecast period. Within the software category, there is a distinction between cloud-based and on-premises solutions. The software's market dominance stems from its crucial function in remote monitoring and epilepsy management, equipping stakeholders with essential tools for data collection and patient engagement. These software solutions facilitate real-time EEG monitoring, data analysis, and teleconsultations for ensuring continuous patient care, timely interventions, and tailored treatment plans that bolster the effectiveness of epilepsy management.

Segmented by epilepsy type, the tele-epilepsy market includes focal seizure, generalized seizure, and combined seizure categories. In 2023, the generalized seizure segment led the market with a 59.7% share, driven by the high prevalence and intricate management needs of these seizures. Given that generalized seizures impact both brain hemispheres simultaneously, they often necessitate continuous monitoring and regular treatment adjustments.

U.S. tele-epilepsy market was valued at USD 218.7 million in 2023 and is projected to soar to USD 795.5 million by the end of 2032. This robust growth is attributed to the high prevalence of epilepsy in the U.S., driving demand for advanced management solutions. The U.S. advantage lies in its established healthcare infrastructure and the widespread embrace of telehealth technologies, from remote diagnostics to teleconsultation platforms. Moreover, supportive government initiatives, favorable reimbursement policies, and relentless technological advancements further cement the U.S.'s dominant position in the tele-epilepsy market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of epilepsy

- 3.2.1.2 Growing demand for remote monitoring services

- 3.2.1.3 Technological advancement in telehealth services

- 3.2.1.4 Rising awareness among patients and caregivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data security and privacy concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Regulatory landscape

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2032 ($ Mn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Cloud-based

- 5.2.2 On-premises

- 5.3 Services

- 5.3.1 Tele-consultation services

- 5.3.2 Tele-monitoring and screening services

- 5.3.3 Tele-education and training

- 5.3.4 Other services

- 5.4 Hardware

Chapter 6 Market Estimates and Forecast, By Epilepsy Type, 2021 - 2032 ($ Mn)

- 6.1 Key trends

- 6.2 Focal seizure

- 6.3 Generalized seizure

- 6.4 Combined seizure

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 - 2032 ($ Mn)

- 7.1 Key trends

- 7.2 Pediatrics

- 7.3 Adults

Chapter 8 Market Estimates and Forecast, By End-user, 2021 - 2032 ($ Mn)

- 8.1 Key trends

- 8.2 Healthcare providers

- 8.2.1 Hospitals and clinics

- 8.2.2 Specialized epilepsy centers

- 8.2.3 Homecare settings

- 8.3 Patients

- 8.4 Other end-users

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2032 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Bioserenity SAS

- 10.2 Ceribell, Inc.

- 10.3 CortiCare, Inc.

- 10.4 Epitel, Inc.

- 10.5 Empatica Inc.

- 10.6 MedaSync.

- 10.7 Medtronic plc

- 10.8 NeuroPace, Inc.

- 10.9 Ovation Healthcare

- 10.10 Real Time Tele-Epilepsy Consultants.

- 10.11 ScienceSoft USA Corporation

- 10.12 Seer Medical

- 10.13 Teladoc Health, Inc.

- 10.14 UCB S.A.

- 10.15 Vidyo, Inc.