|

市場調査レポート

商品コード

1892900

自動車用トルクコンバーター市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Automotive Torque Converter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用トルクコンバーター市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月09日

発行: Global Market Insights Inc.

ページ情報: 英文 230 Pages

納期: 2~3営業日

|

概要

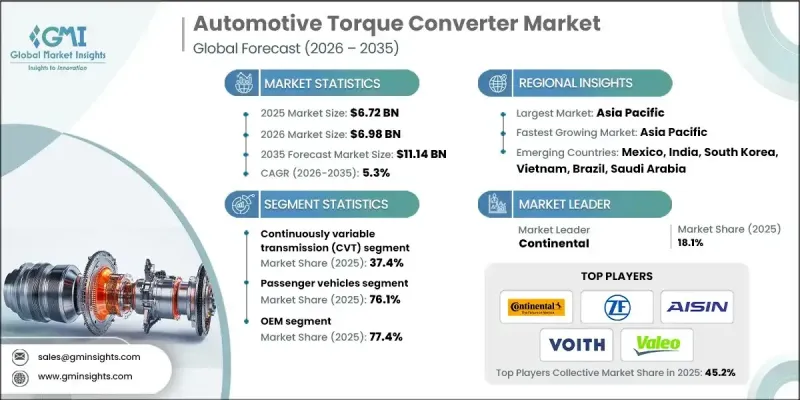

世界の自動車用トルクコンバーター市場は、2025年に67億2,000万米ドルと評価され、2035年までにCAGR 5.3%で成長し、111億4,000万米ドルに達すると予測されています。

この成長は、特に都市部においてより滑らかで容易な運転体験を提供する自動変速機の採用増加によって牽引されています。トルクコンバーターは、複雑なクラッチやギア機構を油圧流体ベースのシステムに置き換えることで従来型車両を変革し、クラッチペダルなしでの車両運転を可能にしております。乗用車および商用車フリート双方における自動変速機への消費者嗜好の高まりが、市場需要を押し上げております。トルクコンバーターはまた、マニュアル変速機と比較して燃費効率を向上させるため、その採用をさらに促進しております。米国や英国など、自動変速車の普及率が高い市場では、新車生産とアフターマーケット部品交換の両面で、引き続き大きな機会が生まれています。世界の都市化とハイブリッド車の普及が進む中、トルクコンバーターは、シームレスで効率的な車両運転に不可欠なものとなりつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 67億2,000万米ドル |

| 予測金額 | 111億4,000万米ドル |

| CAGR | 5.3% |

無段変速機(CVT)セグメントは、優れた燃費効率とエンジンを最適な回転数で動作させる能力により、2025年に37.4%のシェアを占めました。CVTは滑らかでシームレスな運転体験を提供し、都市環境においてますます好まれるようになっています。

乗用車セグメントは2025年に51億1,000万米ドルの市場規模を記録し、自動変速機搭載車への高い需要を反映しています。ハイブリッド電気自動車(HEV)の台頭と、メーカーによる先進的な自動変速機技術の推進が、このセグメントの成長を牽引しています。

米国自動車用トルクコンバーター市場は、2024年の17億5,000万米ドルから増加し、2025年には18億2,000万米ドルに達しました。技術進歩により、米国OEMメーカーは企業平均燃費基準(CAFE)達成に貢献する高効率トルクコンバーターの採用を促進しております。バッテリー式電気自動車(BEV)はトルクコンバーターを必要としない場合が多い一方、HEVおよびプラグインハイブリッド車(PHEV)は効率と性能を最大化するため、先進的でコンパクトなコンバーターに依存しております。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 世界のオートマチックトランスミッションの普及拡大

- 乗用車生産の成長

- 商用車およびオフハイウェイ車両の成長

- アフターマーケット及びサービス市場の成長

- 業界の潜在的リスク&課題

- 電気自動車の普及による自動変速機需要の減少

- 価格に敏感な市場におけるマニュアルトランスミッションの選好

- 市場機会

- ハイブリッド電気自動車(HEV)セグメントの成長

- OEMとのシステムレベル最適化に関する提携

- 持続可能性と循環型経済の統合

- アフターマーケット性能及びレーシング分野

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 米国:米国企業平均燃費基準(CAFE)

- カナダ:カナダの連邦軽自動車基準

- 欧州

- ドイツ:ドイツ道路交通法(StVZO)ライセンシング規定

- フランス:フランスにおける自動車型式認定の枠組み

- 英国:英国車両認証機関(VCA)

- アジア太平洋地域

- 中国:中国VI自動車排出ガス規制

- 日本:日本自動車型式認定(JATA)規制

- インド:バーラト排出ガス規制基準

- ラテンアメリカ

- ブラジル:ブラジル自動車排出ガス規制プログラム(PROCONVE)

- アルゼンチン:アルゼンチン国家自動車安全基準

- メキシコ:メキシコ国家規格(NOM)自動車排出ガス及び安全基準

- 中東・アフリカ

- UAE:アラブ首長国連邦連邦自動車安全・排出ガス規制

- 南アフリカ:南アフリカ共和国道路交通法

- サウジアラビア:SASO燃費基準および車両安全基準

- 北米

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出入

- コスト内訳分析

- 製造コスト構造

- 運営コスト分析

- インフラコスト分析

- コスト最適化戦略

- 特許分析

- 持続可能性と環境影響

- トルクコンバーター生産におけるカーボンフットプリント

- 材料リサイクル可能性分析

- 環境に配慮した製造手法

- ライフサイクルアセスメント

- 最良のシナリオ

- 将来展望と機会

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:送電方式別、2022-2035

- 自動化マニュアルトランスミッション(AMT)

- デュアルクラッチトランスミッション(DCT)

- 無段変速機(CVT)

- その他

第6章 市場推計・予測:コンバーター別、2022-2035

- 単段式

- 多段式

- ロックアップ

- その他

第7章 市場推計・予測:車両別、2022-2035

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 軽商用車(LCV)

- MCV

- 大型商用車(HCV)

第8章 市場推計・予測:販売チャネル別、2022-2035

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- ベネルクス

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ANZ

- シンガポール

- マレーシア

- インドネシア

- ベトナム

- タイ

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- 世界企業

- ZF Friedrichshafen

- Schaeffler

- Valeo

- EXEDY

- Aisin

- BorgWarner

- Yutaka Giken

- Allison Transmission

- JATCO

- Punch Powertrain

- Voith

- Delphi Technologies

- 地域企業

- Zhejiang Torch Auto Parts

- Hubei Aviation Precision Machinery Technology

- Zhejiang Wanliyang

- Transtar Industries

- Florida Torque Converter

- RevMax Converters

- TCI Automotive

- 新興企業

- Circle D Specialties

- Coan Engineering

- Hughes Performance

- Hays Performance(Holley)

- Sonnax Transmission Company