|

|

市場調査レポート

商品コード

1572441

低電圧用複合碍子市場、機会、成長促進要因、産業動向分析と予測、2024年~2032年Low Voltage Composite Insulators Market, Opportunity, Growth Drivers, Industry Trend Analysis and Forecast, 2024-2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 低電圧用複合碍子市場、機会、成長促進要因、産業動向分析と予測、2024年~2032年 |

|

出版日: 2024年08月16日

発行: Global Market Insights Inc.

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

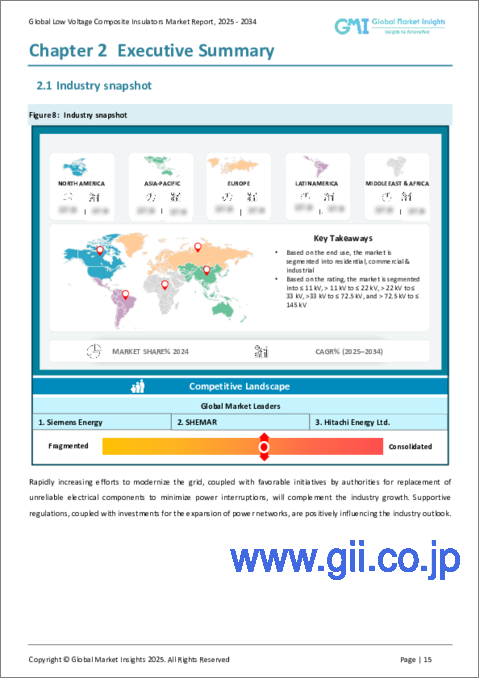

低電圧用複合碍子の世界市場規模は、2023年に5億8,780万米ドルと評価され、2024年から2032年にかけてCAGR 7.3%で成長すると予測されています。

送電網の近代化に向けた取り組みが急速に進んでいることに加え、停電を最小限に抑えるために信頼性の低い電気部品の交換に対する当局の好意的な取り組みが、業界の成長を補完しています。電力網拡張のための投資と相まって、支持的な規制が業界の見通しにプラスの影響を与えています。

例えば、2024年4月、欧州投資銀行は、ドイツの配電システムの強化を含むクリーンエネルギーへの取り組みに焦点を当てた8億500万ユーロの多額の投資を割り当てた。さらに、信頼性の高い碍子ユニットに対する需要の増加や、運用強化のために既存の電気部品をアップグレードする取り組みが、事業ダイナミクスを増大させると思われます。

低電圧用複合碍子産業は、電力需要の増加と送配電網の拡大により成長すると予想されます。スマートグリッド展開の拡大と相まって、電気インフラ改善に向けた投資の加速が業界の展望を補完します。例えば、2024年8月、カリフォルニア州は米国エネルギー省から6億米ドルの助成金を受け、100マイルの送電線の改良に資金を提供します。このイニシアチブは、信頼性を向上させ、クリーンで安価なエネルギーの供給を促進することを目的としています。

世界の低電圧用複合碍子産業は、最終用途、定格、地域によって分類されます。

商業・産業セグメントは、2032年までに7億7,000万米ドルを超えると予測されています。電力需要の増加と送電網の拡大が進み、信頼性の高い送電・配電網の必要性が高まっています。急速に拡大する商業・工業施設は、エネルギー消費の急増とともに都市化の急速な進展に牽引され、事業ダイナミクスにプラスの影響を与えています。

>11 kV~22 kVのセグメントでは、2032年までのCAGRが7%を超えると見られています。低電圧用複合碍子市場は、電力およびインフラ分野での多様な用途によって活性化しています。商業施設や住宅に信頼性の高い電力を供給するために配電網を強化することを目的とした投資の増加は、事業環境にプラスの影響を与えると思われます。効率的で信頼性の高い絶縁ソリューションが必要なマイクログリッド・ネットワークの急速な展開は、エネルギー効率の高いインフラに対する政府の支援とともに、業界の成長を大幅に後押しします。

アジア太平洋の低電圧用複合碍子市場は、2032年までに5億6,000万米ドル以上の成長が見込まれています。人口増加、都市化、様々な分野での電力需要の増大が、ビジネスの展望を補完します。電力網の拡張や再生可能エネルギーと統合された送電網の展開に向けた投資の加速は、事業環境を強化します。

例えば、2024年1月、中国国家電網公司(State Grid Corp of China)は、今年696億米ドル以上を投資する計画を発表しました。この投資は、送電網とトランスミッション・配電網を強化し、安定した電力供給を確保し、グリーンエネルギー消費を促進することを目的としています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:用途別、2021年~2032年

- 主要動向

- 住宅用

- 商業用および産業用

第6章 市場規模・予測:定格別、2021年~2032年

- 主要動向

- 11 kV以下

- 11 kV~22 kV

- 22 kV~33 kV

- 33 kV~72.5 kV

- 72.5 kV超

第7章 市場規模・予測:地域別、2021年~2032年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- CYG Insulator

- Dalian Hivolt Power System

- DECCAN ENTERPRISES PRIVATE LIMITED

- ENSTO

- Hitachi Energy

- Jiangxi Johnson Electric

- KUVAG

- Nooa electric

- PFISTERER Holding

- SAA Grid Technology

- SAVER

- SHEMAR

- Siemens Energy

- Taporel Electrical Insulation Technology

- Vexila

The Global Low Voltage Composite Insulators Market size was valued at USD 587.8 million in 2023 and is set to grow at 7.3% CAGR between 2024 and 2032. Rapidly increasing efforts to modernize the grid, coupled with favourable initiatives by authorities for replacement of unreliable electrical components to minimize power interruptions, will complement the industry growth. Supportive regulations, coupled with investments for the expansion of power networks, are positively influencing the industry outlook.

For instance, in April 2024, The European Investment Bank allotted a substantial EUR 805 million investment focused on clean energy initiatives, including enhancement of Germany's electricity distribution system. Furthermore, increasing demand for reliable insulator units and initiatives to upgrade existing electrical components for enhanced operations, will augment the business dynamics.

The low voltage composite insulators industry is anticipated to grow on account of increasing electricity demand, coupled with the expansion of transmission and distribution grid networks. Accelerating investment toward improving the electrical infrastructure coupled with growing smart grids deployment will complement the industry outlook. For instance, in August 2024, California received a USD 600 million grant from the U.S. Department of Energy, which will fund upgrades on 100 miles of transmission lines. The initiative aims to improve reliability and expedite the delivery of clean and affordable energy.

The Global Low Voltage Composite Insulators Industry is classified based on end-use, rating, and region.

Commercial and industrial segment is anticipated to surpass over USD 770 million through 2032. Increasing electricity demand along with ongoing expansion of grid networks, have accelerated the need for a reliable transmission and distribution network further shaping the business dynamics. Rapidly expanding commercial and industrial establishments driven rapidly increasing urbanization along with rapidly increasing energy consumption have positively influenced the business dynamics.

> 11 kV to <= 22 kV segment is set to witness a CAGR of over 7% through 2032. The low voltage composite insulators market for these insulators is fueled by their diverse applications in the power and infrastructure sectors. Growing investments aimed at enhancing electrical distribution networks to deliver reliable power across commercial and residential establishments will positively influence the business landscape. Rapid deployment of micro-grid networks, which necessitate efficient and reliable insulation solutions, along with government support for energy-efficient infrastructures will significantly boost the industry growth.

Asia Pacific low voltage composite insulators market is set to grow over USD 560 million by 2032. Rising population growth, urbanization, and growing demand for power across various sectors will complement the business landscape. Accelerating investments for expansion of electrical networks and deployment of renewable-integrated grid networks, will augment the business landscape.

For instance, In January 2024, State Grid Corp of China unveiled plans to invest over USD 69.6 billion this year. The investment aims to bolster the grid and transmission and distribution (T&D) network, ensuring stable power supply and promoting green energy consumption.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market definitions

- 1.2 Base estimates and calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls and challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic outlook

- 4.2 Innovation and sustainability landscape

Chapter 5 Market Size and Forecast, By End-Use, 2021 - 2032, (USD Million)

- 5.1 Key trends

- 5.2 Residential

- 5.3 Commercial and industrial

Chapter 6 Market Size and Forecast, By Rating, 2021 - 2032, (USD Million)

- 6.1 Key trends

- 6.2 <= 11 kV

- 6.3 > 11 kV to <= 22 kV

- 6.4 > 22 kV to <= 33 kV

- 6.5 > 33 kV to <= 72.5 kV

- 6.6 > 72.5 kV

Chapter 7 Market Size and Forecast, By Region, 2021 - 2032, (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East and Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 CYG Insulator

- 8.2 Dalian Hivolt Power System

- 8.3 DECCAN ENTERPRISES PRIVATE LIMITED

- 8.4 ENSTO

- 8.5 Hitachi Energy

- 8.6 Jiangxi Johnson Electric

- 8.7 KUVAG

- 8.8 Nooa electric

- 8.9 PFISTERER Holding

- 8.10 SAA Grid Technology

- 8.11 SAVER

- 8.12 SHEMAR

- 8.13 Siemens Energy

- 8.14 Taporel Electrical Insulation Technology

- 8.15 Vexila