整形外科用ソフトウェア市場の機会、成長要因、業界動向分析、および2026年~2035年の予測

Orthopedic Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 2038713

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

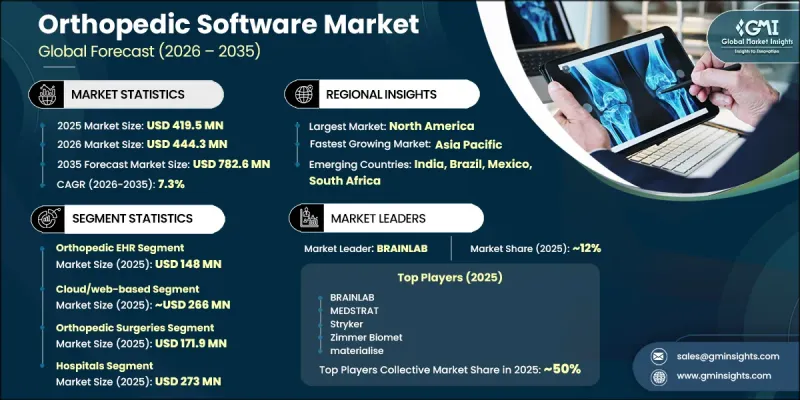

世界の整形外科用ソフトウェア市場は、2025年に4億1,950万米ドルと評価され、CAGR 7.3%で成長し、2035年までに7億8,260万米ドルに達すると予測されています。

この成長は、整形外科疾患の発生率の上昇と、低侵襲手術への志向の高まりによって支えられています。整形外科用ソフトウェアは、高度なデジタルツールを通じて、臨床医が筋骨格系の疾患を診断、計画、管理することを支援するように設計されています。これらのプラットフォームは、画像診断の詳細な分析、手術シミュレーション、および効率的な患者データ管理を可能にすることで、臨床判断の精度を高めます。手術の精度向上、患者アウトカムの改善、再手術の削減に対する需要の高まりが、導入をさらに後押ししています。高齢化やスポーツ・身体活動への参加増加に後押しされた筋骨格系疾患の負担増大が、市場の拡大に大きく寄与しています。医療のデジタル化とワークフローの効率化への関心の高まりにより、医療提供者は、整形外科ケアの提供を合理化し、医療施設全体の運営パフォーマンスを向上させる統合型ソフトウェアソリューションの導入を促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時点の市場規模 | 4億1,950万米ドル |

| 予測額 | 7億8,260万米ドル |

| CAGR | 7.3% |

整形外科用ソフトウェア市場も、デジタル医療システムの統合が進み、相互運用可能なプラットフォームへの需要が高まっていることから、拡大しています。医療提供者は、高度なソフトウェアソリューションを通じて、臨床、管理、診断の各ワークフロー間の連携強化に注力しています。継続的な技術革新により、データへのアクセス性の向上、画像診断の統合化、および治療計画策定能力の強化が可能になっています。価値に基づく医療モデルへの認識の高まりは、効率性を向上させ、治療のばらつきを低減するデジタル整形外科ソリューションの導入をさらに後押ししています。医療インフラの拡大とデジタルヘルス技術への投資増加も、世界各地域における市場の持続的な成長に寄与しています。

整形外科用電子健康記録(EHR)セグメントは、2025年に1億4,800万米ドルを占めました。その優位性は、臨床記録の効率化と、整形外科診療全体におけるワークフロー効率の向上を実現する能力に支えられています。これらのシステムは、筋骨格系ケア向けにカスタマイズされており、怪我の追跡、インプラント記録、治療結果のモニタリングなどの機能をサポートしているため、広く採用されています。統合された患者記録や、画像診断システムおよび請求システムとのシームレスな連携に対する需要の高まりが、このセグメントの成長をさらに後押ししています。データ駆動型の医療提供への移行は、整形外科医療環境におけるその重要性を引き続き高めています。

クラウド/ウェブベースのセグメントは、2025年に2億6,600万米ドルに達しました。このセグメントは、その拡張性、コスト効率、および規模の異なる医療施設全体での導入の容易さにより、強い勢いを見せています。これにより、リアルタイムでのデータアクセス、遠隔での共同作業、および他の医療システムとの円滑な統合が可能になります。サブスクリプション型モデルへの嗜好の高まりや、インフラ要件の低減が、導入をさらに加速させています。強化されたデータセキュリティ対策や継続的なソフトウェア更新も、クラウドベースの整形外科ソリューションの普及を支えています。

北米の整形外科ソフトウェア市場は、2025年に1億6,460万米ドルの規模に達しました。同地域は、先進的な医療インフラ、デジタル技術の積極的な導入、および統合型臨床システムへの需要の高まりという恩恵を受けています。同地域の医療提供者は、業務効率の向上と患者アウトカムの改善を図るため、デジタル整形外科ソリューションを急速に導入しています。クラウドベースのプラットフォームへの移行が進んでいることに加え、電子カルテの導入やデータの相互運用性に対する規制面の支援も相まって、病院、クリニック、手術センター全体での市場成長がさらに強化されています。

よくあるご質問

目次

第1章 調査手法

- 調査アプローチ

- 品質に関する取り組み

- GMI AIポリシーおよびデータ完全性に関する取り組み

- 情報源の一貫性に関するプロトコル

- GMI AIポリシーおよびデータ完全性に関する取り組み

- 調査の経緯と信頼度スコアリング

- 調査の経緯の構成要素

- スコアリングの構成要素

- データ収集

- 一次情報の一部リスト

- データマイニング情報源

- 有料情報源

- 地域別情報源

- 有料情報源

- 基本推定および算出方法

- 各アプローチにおける基準年の算出

- 予測モデル

- 定量化された市場影響分析

- 成長パラメータが予測に与える数学的影響

- 定量化された市場影響分析

- 調査の透明性に関する補足

- 情報源の帰属フレームワーク

- 品質保証指標

- 信頼への取り組み

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 整形外科疾患の有病率の増加

- 整形外科用ソフトウェアにおける技術的進歩

- 低侵襲手術への需要の高まり

- 手術成果の向上、効率化、および再手術率の低減に対する需要の高まり

- 業界の潜在的リスク&課題

- ソフトウェアの誤動作による潜在的なリスク

- 高い導入・保守コスト

- 市場機会

- AI搭載の術前計画・意思決定支援ソフトウェアに対する需要の高まり

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術動向

- 現在の技術動向(1次調査に基づく)

- 新興技術

- 将来の市場動向(1次調査に基づく)

- 特許動向(1次調査に基づく)

- AIおよび生成AIが市場に与える影響(1次調査に基づく)

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携および協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:製品タイプ別、2022年~2035年

- 整形外科用EHR

- 整形外科用PACS

- 整形外科RCM

- 整形外科診療管理

- デジタルテンプレート/術前計画ソフトウェア

第6章 市場推計・予測:配信形態別、2022年~2035年

- クラウド/Webベース

- オンプレミス

第7章 市場推計・予測:用途別、2022年~2035年

- 整形外科手術

- 骨折治療

- 関節置換術

- その他の用途

第8章 市場推計・予測:最終用途別、2022年~2035年

- 病院

- 外来手術センター

- その他のエンドユーザー

第9章 市場推計・予測:地域別、2022年~2035年

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- BRAINLAB

- Carestream

- Esaote

- GE HealthCare

- intellijoint surgical

- materialise

- McKESSON

- MEDSTRAT

- merative

- Philips

- Siemens Healthineers

- Stryker

- Surgimap

- Zimmer Biomet

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日