|

市場調査レポート

商品コード

1913355

アーク溶接機器市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Arc Welding Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| アーク溶接機器市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月16日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

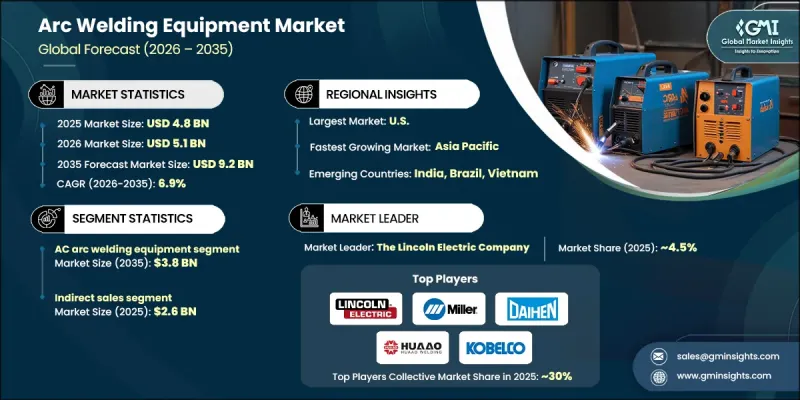

世界のアーク溶接機器市場は、2025年に48億米ドルと評価され、2035年までにCAGR6.9%で成長し、92億米ドルに達すると予測されています。

職場の安全と設備設計を規定する規制枠組みは、アーク溶接作業に依存する業界全体の需要を大きく左右しております。電圧閾値、電気絶縁、接地プロトコル、気流基準に関する厳格な要件により、規制に準拠した溶接システムと安全対策ソリューションの導入が進んでおります。溶接に関連する健康リスクへの認識の高まりは、適切な換気、排気管理、呼吸保護の必要性をさらに強めております。労働安全規制では、耐熱性・耐火性・耐電気暴露性を備えた保護具の使用が義務付けられるとともに、視認性や顔面保護に関する性能基準も規定されています。これらの規則は、機器設計、施設改修、購買判断に総合的に影響を及ぼします。メーカーとエンドユーザーがコンプライアンス、作業安全、労働者保護を優先する中、先進的なアーク溶接機器への需要は引き続き増加しています。市場の成長は、生産性を支えつつ長期的な職業リスクを低減する、より安全で規制に準拠した技術への持続的な投資を反映しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 48億米ドル |

| 予測金額 | 92億米ドル |

| CAGR | 6.9% |

2025年、交流アーク溶接装置は40.3%のシェアを占め、2035年までCAGR7%で成長が見込まれます。このセグメントは、コスト競争力と、様々な電気的条件下でも安定した性能を支える動作特性という利点があります。開放電圧レベルに対する規制制限は製品設計に直接影響し、メーカーは手動および自動アプリケーションの両方において、確立された安全基準に準拠した装置開発を促されています。

間接販売チャネルは2025年に26億米ドルを生み出し、55%のシェアを占めました。このルートは標準化製品、交換部品、消耗品の広範な流通を支えると同時に、メーカーが直接対応していない地域や顧客層へのリーチを拡大します。間接チャネルは、特に二次市場や小規模な運用環境において、拡張性、柔軟性、コスト効率を提供します。

北米アーク溶接機器市場は2025年に38.2%のシェアを占め、2035年までCAGR7.1%で成長すると予測されています。強力な製造能力、安全基準の厳格な施行、継続的な機器アップグレードが地域の優位性を支えています。規制要件により詳細な技術要件が定められており、これが購買行動や機器の交換サイクルに直接影響を与えています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 厳格な安全規制

- 持続的な鉄鋼生産とインフラ整備

- 健康リスクへの意識の高まりが安全な技術の促進につながっています

- 業界の潜在的リスク&課題

- 高い資本コストと統合コスト

- 技術者不足とコンプライアンス負担

- 機会

- 再生可能エネルギーおよびグリーンインフラプロジェクトの拡大

- AI駆動型およびIoT対応溶接ソリューションの開発

- 促進要因

- 成長可能性分析

- 将来の市場動向

- 価格動向分析

- 地域と溶接技術

- 技術とイノベーションの動向

- 現行技術

- 新興技術

- 規制の枠組み

- 地域別

- ポーターのファイブフォース分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 製品ポートフォリオのベンチマーク

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:溶接技術別2022-2035

- シールドメタルアーク溶接(SMAW)

- ガス金属アーク溶接(GMAW/MIG)

- フラックス入りアーク溶接(FCAW)

- ガス・タングステン・アーク溶接(GTAW)

- サブマージアーク溶接(SAW)

- その他(プラズマアーク溶接(PAW)など)

第6章 市場推計・予測:電源別、2022-2035

- 交流アーク溶接装置

- 直流アーク溶接装置

- その他

第7章 市場推計・予測:最終用途産業別、2022-2035

- 自動車・輸送機器

- 重工業・製造

- 建設・インフラ

- 造船・海洋産業

- 航空宇宙・防衛産業

- エネルギーおよび電力

- 石油・ガス

- その他

第8章 市場推計・予測:流通チャネル別、2022-2035

- 直接販売

- 間接販売

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Ador Welding

- Amada Miyachi America

- Arcon Welding Equipment

- CLOOS Welding Equipment

- Daihen

- Denyo

- ESAB

- Fronius International

- Illinois Tool Works(ITW Welding)

- Jinan Huaao Electric Welding Machine

- Kobe Steel(Kobelco)

- Miller Electric Mfg.(part of ITW Welding)

- OTC Daihen

- Panasonic Welding Systems

- The Lincoln Electric Company