|

市場調査レポート

商品コード

1716452

曲げ機市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Bending Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 曲げ機市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月25日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

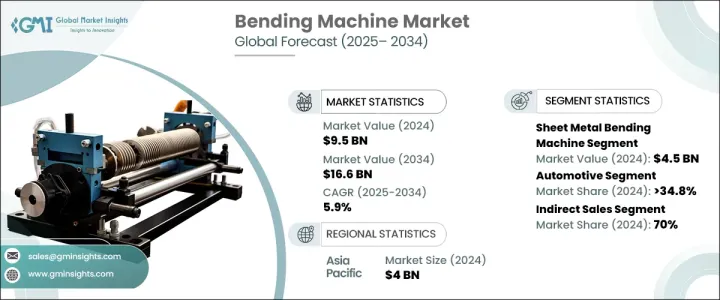

世界の曲げ機市場は、2024年に95億米ドルと評価され、2025年から2034年にかけてCAGR 5.9%で成長すると予測されています。

曲げ機は、製造、建設、自動車、航空宇宙など複数の産業で不可欠な役割を果たしています。これらの機械は、シートメタル、パイプ、チューブ、プロファイルの成形に使用され、複雑なコンポーネントや構造の生産に不可欠なものとなっています。世界の工業化の加速に伴い、特にインフラや建設プロジェクトが急拡大している新興国では、曲げ機の需要が増加しています。さまざまな分野で自動化と精密工学の導入が進んでいることが市場の成長をさらに押し上げ、複雑な設計を高精度で処理できる高度な曲げ機への需要を促進しています。

技術の進歩は曲げ機の展望を変えつつあり、CNCやロボットモデルは優れた効率と精度を提供しています。しかし、特に新興国の中小メーカーにとっては、こうした高度な機械の高い導入コストとメンテナンスコストが大きな課題となります。さらに、これらの機械は、複雑なシステムのプログラミングと管理に精通した熟練オペレーターを必要とするため、技術的専門知識の乏しい企業にとっては障壁となります。このような課題にもかかわらず、自動化プロセスやカスタマイズされた部品生産が重視されるようになり、各業界で高度な曲げ機の採用に拍車がかかっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 95億米ドル |

| 予測金額 | 166億米ドル |

| CAGR | 5.9% |

板金曲げ機セグメントは、2024年に45億米ドルを生み出し、2034年までCAGR 6.6%で成長すると予測されています。シートメタルは、建設、自動車、航空宇宙、エレクトロニクス、製造などの産業で幅広く使用されているため、これらの機械の価値は非常に高いです。複雑な形状や角度の曲げ加工に優れているため、製造業者は特定の設計要件を高精度で満たすことができます。パイプ曲げ機やチューブ曲げ機と比べ、板金曲げ機は大きな板を加工する際にコスト面で有利であり、大規模な部品生産に経済的に適しています。軽量素材の採用とカスタマイズ部品のニーズの高まりは、板金曲げ機の需要をさらに高めています。

市場は最終用途別に、航空宇宙・防衛、自動車、一般機械・設備、電気・電子、ヘルスケアや海洋用途を含むその他に区分されます。自動車分野は2024年の市場シェアの34.8%を占め、2034年までのCAGRは5.6%で成長すると予想されています。曲げ機は、排気システム、ロールケージ、シャーシ要素などの精密でカスタマイズされた部品を製造する自動車製造に不可欠です。自動車メーカーが燃費と性能の向上のためにアルミニウムや高度合金のような軽量素材を取り入れることが増えているため、曲げ機の需要は増加の一途をたどっています。

アジア太平洋地域は、2024年に曲げ機市場から40億米ドルの収益を上げました。この地域は、特に自動車、航空宇宙、建設、エレクトロニクス分野の主要な製造拠点を擁しています。中国、インド、韓国のような国々における急速な産業拡大とインフラ開発が、自動車部品、構造要素、家電製品を含む幅広い部品を生産するための曲げ機の需要を促進しています。この地域は技術革新と精密製造に重点を置いており、アジア太平洋地域が世界の曲げ機産業における支配的なプレーヤーとなり、市場成長を促進すると予想されます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤー情勢

- 価格分析

- テクノロジーとイノベーションの展望

- 主要ニュース&イニシアティブ

- 規制状況

- メーカー

- 販売業者

- 勢力への影響

- 促進要因

- 工業化の進展とインフラ開発

- 製造業の急成長

- 製造技術の進歩

- 業界の潜在的リスク&課題

- 高額な初期投資

- 熟練労働者の不足

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 板金曲げ機

- パイプ/チューブ曲げ機

- その他(プレスブレーキ、ロールフォーミング、バーベンディング)

第6章 市場推計・予測:駆動機構別、2021年~2034年

- 主要動向

- 電動

- 油圧

- 空圧

- 機械

第7章 市場推計・予測:運転技術別、2021年~2034年

- 主要動向

- 従来型

- コンピュータ数値制御(CNC)

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 航空宇宙・防衛

- 自動車

- 一般機械・設備

- 建築・建設

- その他(鉱業、海洋など)

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 間接販売

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Amada

- Amob

- Baileigh Industrial

- BLM Group

- Bystronic Group

- Euromac

- Horn Machine Tools

- Murata Machinery

- Pedax

- Prima Industrie

- Sahinler Metal Makina Industry

- Shuz Tung Machinery Industrial

- Transfluid

- Trumpf

- Wafios

The Global Bending Machine Market was valued at USD 9.5 billion in 2024 and is expected to grow at a CAGR of 5.9% from 2025 to 2034. Bending machines play an integral role across multiple industries, including manufacturing, construction, automotive, and aerospace. These machines are used to shape sheet metal, pipes, tubes, and profiles, making them indispensable in producing complex components and structures. As global industrialization accelerates, the demand for bending machines is increasing, especially in emerging economies where infrastructure and construction projects are expanding rapidly. The rising adoption of automation and precision engineering in various sectors further boosts market growth, driving demand for advanced bending machines that can handle intricate designs with high accuracy.

Technological advancements are transforming the bending machine landscape, with CNC and robotic models offering superior efficiency and precision. However, the high acquisition and maintenance costs of these advanced machines can be a significant challenge, particularly for smaller manufacturers in emerging economies. Additionally, these machines require skilled operators proficient in programming and managing complex systems, posing a barrier for companies with limited technical expertise. Despite these challenges, the growing emphasis on automated processes and customized component production is fueling the adoption of advanced bending machines across industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.5 Billion |

| Forecast Value | $16.6 Billion |

| CAGR | 5.9% |

The sheet metal bending machine segment generated USD 4.5 billion in 2024 and is projected to grow at a CAGR of 6.6% through 2034. Sheet metal is extensively used across industries such as construction, automotive, aerospace, electronics, and manufacturing, making these machines highly valuable. They excel in bending intricate shapes and angles, enabling manufacturers to meet specific design requirements with high precision. Compared to pipe or tube bending machines, sheet metal bending machines offer cost advantages when processing larger sheets, making them economically viable for large-scale component production. The growing adoption of lightweight materials and the need for customized parts further enhance the demand for sheet metal bending machines.

The market is segmented by end-use into aerospace & defense, automotive, general machinery & equipment, electrical & electronics, and others, including healthcare and marine applications. The automotive segment accounted for 34.8% of the market share in 2024 and is expected to grow at a CAGR of 5.6% through 2034. Bending machines are essential in automotive manufacturing, where they create precise and customized components such as exhaust systems, roll cages, and chassis elements. As automakers increasingly incorporate lightweight materials like aluminum and advanced alloys to improve fuel efficiency and performance, the demand for bending machines continues to rise.

Asia Pacific generated USD 4 billion in revenue from the bending machine market in 2024. The region hosts major manufacturing hubs, particularly in the automotive, aerospace, construction, and electronics sectors. Rapid industrial expansion and infrastructure development in countries like China, India, and South Korea are driving the demand for bending machines to produce a wide range of components, including automotive parts, structural elements, and consumer electronics. The region's emphasis on technological innovation and precision manufacturing is expected to propel market growth, making the Asia Pacific a dominant player in the global bending machine industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier Landscape

- 3.3 Pricing analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Manufacturers

- 3.8 Distributors

- 3.9 Impact on forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing industrialization and infrastructure development

- 3.9.1.2 Rapid growth in the manufacturing sector

- 3.9.1.3 Advancements in manufacturing technologies

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial investment

- 3.9.2.2 Shortage of skilled labor

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn) (Thousand Units)

- 5.1 Key trends

- 5.2 Sheet metal bending machine

- 5.3 Pipe/tube bending machine

- 5.4 Others (press brake, roll forming, bar bending)

Chapter 6 Market Estimates & Forecast, By Driving Mechanism, 2021 - 2034 ($Bn) (Thousand Units)

- 6.1 Key trends

- 6.2 Electric

- 6.3 Hydraulic

- 6.4 Pneumatic

- 6.5 Mechanical

Chapter 7 Market Estimates & Forecast, By Operating Technology, 2021 - 2034 ($Bn) (Thousand Units)

- 7.1 Key trends

- 7.2 Conventional

- 7.3 Computer numerically controlled (CNC)

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn) (Thousand Units)

- 8.1 Key trends

- 8.2 Aerospace & defense

- 8.3 Automotive

- 8.4 General machinery & equipment

- 8.5 Building & construction

- 8.6 Others (mining, marine, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Amada

- 11.2 Amob

- 11.3 Baileigh Industrial

- 11.4 BLM Group

- 11.5 Bystronic Group

- 11.6 Euromac

- 11.7 Horn Machine Tools

- 11.8 Murata Machinery

- 11.9 Pedax

- 11.10 Prima Industrie

- 11.11 Sahinler Metal Makina Industry

- 11.12 Shuz Tung Machinery Industrial

- 11.13 Transfluid

- 11.14 Trumpf

- 11.15 Wafios