|

市場調査レポート

商品コード

1797839

採血の市場機会、成長促進要因、産業動向分析、2025~2034年予測Blood Collection Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 採血の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年07月17日

発行: Global Market Insights Inc.

ページ情報: 英文 133 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

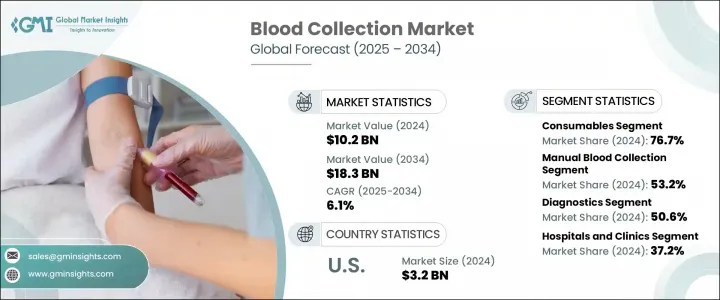

採血の世界市場規模は、2024年に102億米ドルとなり、CAGR 6.1%で成長し、2034年には183億米ドルに達すると推定されます。

市場拡大の原動力となっているのは、慢性疾患や感染症の負担増、急速な技術革新、手術件数の増加、高齢者人口の増加などです。ヘルスケアプロバイダーは、診断、治療、研究のために安全、正確、効率的なサンプル収集を優先するため、高度な採血ソリューションへの需要が増加しています。採血デバイスは、臨床ワークフローにおける重要なツールであり、患者の安全を考慮した正確な血液サンプルの採取を保証します。これらの機器は病院、診断研究所、血液バンクで広く使用されており、様々な医療検査プロセスのバックボーンとして機能しています。同市場はまた、業務を合理化し、汚染リスクを低減し、患者体験を向上させるシステムへの投資が拡大しており、長期的な成長軌道をさらに強化しています。

製品タイプ別に見ると、市場はシステムと消耗品に分けられます。消耗品セグメントは2024年に76.7%の最大シェアを占め、一貫性のある正確なサンプル採取に不可欠な役割を果たすことがその原動力となっています。この分野は、予測期間中にCAGR 6%で成長し、2034年には139億米ドル以上に達すると予測されています。一方、システムは、業務効率と患者の快適性を向上させる統合ソリューションの採用増加に支えられ、2025~2034年のCAGRは6.3%とやや高い成長が予測されています。ヘルスケアプロバイダーは、診断精度を高め、手技リスクを低減するように設計されたシステムをますます好むようになっており、このセグメントの勢いに拍車をかけています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 102億米ドル |

| 予測金額 | 183億米ドル |

| CAGR | 6.1% |

市場セグメンテーションは、手法別に手動型と自動型に区分されます。手動の採血は2024年の市場全体の53.2%を占め、費用対効果、可用性、さまざまな臨床環境での使いやすさが成長を支えています。このアプローチは、正確なサンプル抽出を行うために訓練を受けた専門家に頼る、世界中のヘルスケア診療の重要な要素であり続けています。このプロセスでは通常、特定の患者や検査の要件に合わせて、針や真空システムなど独自の装置を使用し、多様な環境での信頼性を確保しています。

アプリケーションの観点から、市場は診断、治療、調査に分類されます。診断分野は2024年も50.6%のシェアで支配的であり、疾病の検出、モニタリング、予防のために血液サンプルに依存する検査が増加していることがその要因となっています。健康状態の早期かつ正確な特定に対する需要の高まりが、先進的な採血システムの必要性に拍車をかけており、それがこのセグメントの成長を加速させています。

地域別では、北米が2024年のシェア35.4%で世界の採血市場をリードしており、強力なヘルスケアインフラ、慢性疾患の症例増加、診断検査量の多さに支えられています。同地域はまた、革新的な採血技術の急速な採用や、診断スピードと精度の向上に重点を置いていることも利点となっています。同地域では米国が依然として主要な貢献国であり、市場規模は2023年の31億米ドルから2024年には32億米ドルに拡大します。調査手法の継続的な改善に支えられた高品質の診断サービスに対する一貫した需要は、予測期間を通じて同国の主導的地位を維持するとみられます。

競合情勢を左右する主要企業には、サーモフィッシャーサイエンティフィック、テルモ、マッケソン、ヘモネティクス、アボットラボラトリーズ、QIAGEN、フレゼニウスSE&Co、サーステットAG&Co、グライナー、FLメディカル、ベクトン・ディッキンソン&カンパニー、カーディナルヘルス、F.ホフマン・ラ・ロシュ、シュトレック、シーメンス・ヘルスィニアーズ、ニプロなどがあります。これらの企業は一貫して、製品イノベーションを推進し、世界展開を強化し、世界中の医療従事者の変化する要求に応えるソリューションを提供することに注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患および感染症の発生率の上昇

- 採血技術の進歩

- 外科手術の増加

- 高齢化人口の増加

- 業界の潜在的リスク&課題

- 輸血に伴うリスク

- 熟練したヘルスケア専門家の不足

- 市場機会

- 政府主導による献血と疾病検査の促進キャンペーンの拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- システム

- 自動化システム

- 手動システム

- 消耗品

- 静脈

- 針と注射器

- 両端針

- 翼のある採血セット

- 標準的な皮下注射針

- その他の採血針

- 採血チューブ

- 血清分離

- EDTA

- ヘパリン

- 血漿分離

- 血液バッグ

- その他の静脈製品

- 針と注射器

- 毛細血管

- ランセット

- マイクロコンテナチューブ

- マイクロヘマトクリットチューブ

- 加温装置

- その他の毛細血管製品

- 静脈

第6章 市場推計・予測:方法別、2021-2034

- 主要動向

- マニュアル採血

- 自動化された採血

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 診断

- 治療

- 調査

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院と診療所

- 診断センター

- 血液銀行

- 学術研究機関

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Abbott Laboratories

- Becton, Dickinson, and Company

- Cardinal Health

- F. Hoffmann-La Roche

- FL MEDICAL

- Fresenius SE &Co

- Greiner

- Haemonetics Corporation

- McKesson Corporation

- Nipro Corporation

- QIAGEN

- Sarstedt AG &Co

- Siemens Healthineers

- Streck

- Terumo Corporation

- Thermo Fisher Scientific

The Global Blood Collection Market was valued at USD 10.2 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 18.3 billion by 2034. Market expansion is being driven by the growing burden of chronic and infectious diseases, rapid technological innovation, a higher volume of surgical procedures, and a rising elderly population. The demand for advanced blood collection solutions is increasing as healthcare providers prioritize safe, accurate, and efficient sample collection for diagnostics, treatment, and research. Blood collection devices are critical tools in clinical workflows, ensuring that blood samples are obtained with precision and patient safety in mind. These devices are widely used in hospitals, diagnostic laboratories, and blood banks, serving as the backbone of various medical testing processes. The market is also witnessing greater investment in systems that streamline operations, reduce contamination risk, and improve patient experience, further reinforcing its long-term growth trajectory.

By product type, the market is divided into systems and consumables. The consumables segment held the largest share at 76.7% in 2024, driven by its essential role in consistent and accurate sample collection. This segment is expected to reach over USD 13.9 billion by 2034, advancing at a CAGR of 6% during the forecast period. Systems, on the other hand, are forecast to grow at a slightly higher CAGR of 6.3% between 2025 and 2034, supported by the rising adoption of integrated solutions that improve operational efficiency and patient comfort. Healthcare providers are increasingly favoring systems designed to enhance diagnostic accuracy and reduce procedural risks, adding to the segment's momentum.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.2 billion |

| Forecast Value | $18.3 billion |

| CAGR | 6.1% |

Based on method, the market is segmented into manual and automated blood collection. Manual blood collection accounted for 53.2% of the total market in 2024, with growth supported by its cost-effectiveness, availability, and ease of use in various clinical environments. This approach continues to be a key component of healthcare practices worldwide, relying on trained professionals to perform accurate sample extraction. The process typically involves using tailored devices such as needles or vacuum systems to meet specific patient and test requirements, ensuring reliability in diverse settings.

In terms of application, the market is categorized into diagnostics, treatment, and research. Diagnostics remained the dominant segment in 2024 with a 50.6% share, fueled by the growing number of tests that depend on blood samples for disease detection, monitoring, and prevention. Rising demand for early and precise identification of health conditions is spurring the need for advanced blood collection systems, which in turn is accelerating the segment's growth.

Regionally, North America led the global blood collection market with a 35.4% share in 2024, underpinned by a strong healthcare infrastructure, increasing cases of chronic illnesses, and a high volume of diagnostic testing. The region also benefits from the rapid adoption of innovative blood collection technologies and an emphasis on improving diagnostic speed and accuracy. Within the region, the United States remains the primary contributor, with the market size growing from USD 3.1 billion in 2023 to USD 3.2 billion in 2024. Consistent demand for high-quality diagnostic services, supported by continuous improvements in blood collection methodologies, is expected to sustain the country's leadership position throughout the forecast period.

Key players influencing the competitive landscape include Thermo Fisher Scientific, Terumo Corporation, McKesson Corporation, Haemonetics Corporation, Abbott Laboratories, QIAGEN, Fresenius SE & Co, Sarstedt AG & Co, Greiner, FL MEDICAL, Becton, Dickinson and Company, Cardinal Health, F. Hoffmann-La Roche, Streck, Siemens Healthineers, and Nipro Corporation. These companies are consistently focused on driving product innovation, strengthening their global reach, and delivering solutions that meet the changing requirements of healthcare providers across the world.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Method

- 2.2.4 Application

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of chronic and infectious diseases

- 3.2.1.2 Advancements in blood collection technologies

- 3.2.1.3 Increasing number of surgical procedures

- 3.2.1.4 Rising geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risks associated with blood transfusions

- 3.2.2.2 Lack of skilled healthcare professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Rising government-led campaigns for promoting blood donation and disease screening

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 System

- 5.2.1 Automated systems

- 5.2.2 Manual systems

- 5.3 Consumables

- 5.3.1 Venous

- 5.3.1.1 Needles and syringes

- 5.3.1.1.1 Double-ended needles

- 5.3.1.1.2 Winged blood collection sets

- 5.3.1.1.3 Standard hypodermic needles

- 5.3.1.1.4 Other blood collection needles

- 5.3.1.2 Blood collection tubes

- 5.3.1.2.1 Serum-separating

- 5.3.1.2.2 EDTA

- 5.3.1.2.3 Heparin

- 5.3.1.2.4 Plasma-separating

- 5.3.1.3 Blood bags

- 5.3.1.4 Other venous products

- 5.3.1.1 Needles and syringes

- 5.3.2 Capillary

- 5.3.2.1 Lancets

- 5.3.2.2 Micro-container tubes

- 5.3.2.3 Micro-hematocrit tubes

- 5.3.2.4 Warming devices

- 5.3.2.5 Other capillary products

- 5.3.1 Venous

Chapter 6 Market Estimates and Forecast, By Method, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Manual blood collection

- 6.3 Automated blood collection

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Diagnostics

- 7.3 Treatment

- 7.4 Research

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 1.1 Key trends

- 1.2 Hospitals and clinics

- 1.3 Diagnostic centers

- 1.4 Blood banks

- 1.5 Academic and research institutes

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 1.5.1 U.S.

- 1.5.2 Canada

- 9.3 Europe

- 1.5.3 Germany

- 1.5.4 UK

- 1.5.5 France

- 1.5.6 Spain

- 1.5.7 Italy

- 1.5.8 Netherlands

- 9.4 Asia Pacific

- 1.5.9 China

- 1.5.10 Japan

- 1.5.11 India

- 1.5.12 Australia

- 1.5.13 South Korea

- 9.5 Latin America

- 1.5.14 Brazil

- 1.5.15 Mexico

- 1.5.16 Argentina

- 9.6 Middle East and Africa

- 1.5.17 South Africa

- 1.5.18 Saudi Arabia

- 1.5.19 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 Becton, Dickinson, and Company

- 10.3 Cardinal Health

- 10.4 F. Hoffmann-La Roche

- 10.5 FL MEDICAL

- 10.6 Fresenius SE & Co

- 10.7 Greiner

- 10.8 Haemonetics Corporation

- 10.9 McKesson Corporation

- 10.10 Nipro Corporation

- 10.11 QIAGEN

- 10.12 Sarstedt AG & Co

- 10.13 Siemens Healthineers

- 10.14 Streck

- 10.15 Terumo Corporation

- 10.16 Thermo Fisher Scientific