|

市場調査レポート

商品コード

1716665

エンジンバルブ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Engine Valve Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| エンジンバルブ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月26日

発行: Global Market Insights Inc.

ページ情報: 英文 161 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

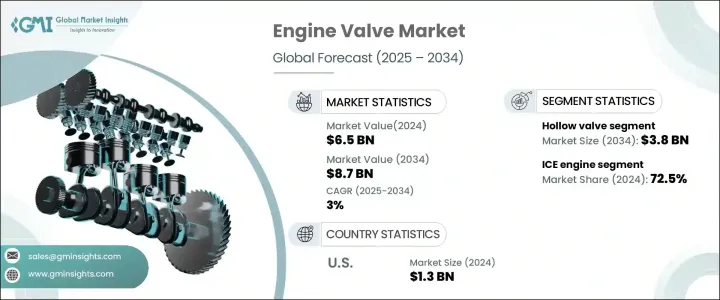

エンジンバルブの世界市場は、2024年には65億米ドルとなり、2025年から2034年にかけてCAGR 3%で拡大すると予測され、着実な成長が見込まれています。

低燃費車に対する世界の需要の高まりが、市場拡大に影響を与える主な要因です。世界各国政府が燃費・排ガス規制を強化する中、自動車メーカーは先進エンジン技術を急速に導入しています。このため、高性能エンジン部品、特に燃焼効率と排ガス制御で極めて重要な役割を果たすバルブの需要が急増しています。ターボ過給や可変バルブタイミングなど、エンジン設計の革新が進むにつれ、燃料燃焼を最適化し、車両全体の性能を高める精密工学バルブのニーズがさらに高まっています。自動車メーカーが厳しい規制要件を満たすために軽量で耐久性のあるエンジン部品に注力する中、エンジンバルブ市場は材料科学と製造プロセスにおいて著しい進歩を遂げています。

市場はバルブタイプによって、中空バルブ、モノメタルバルブ、バイメタルバルブに区分されます。中空バルブセグメントは2024年に29億米ドルを占め、その優れた軽量特性により牽引力を増しています。中空バルブはソリッドバルブに比べ、より高速で正確なバルブの動きを可能にすることで、エンジン効率を高めるという大きな利点があります。これらのバルブは、スピードと熱管理が重要な高性能エンジンやレーシングエンジンにおいて特に有益です。熱放散を改善する中空バルブの能力は、エンジンが最適な温度で作動することを保証し、それによって高いストレスや過酷な条件にさらされるエンジン部品の寿命を延ばします。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 65億米ドル |

| 予測金額 | 87億米ドル |

| CAGR | 3% |

エンジンタイプ別に見ると、市場は内燃エンジン(ICE)と電気エンジンに分類されます。2024年のシェアはICEエンジンが72.5%を占め、2034年までのCAGRは2.8%と予測されます。電気自動車が自動車業界を徐々に再構築しつつある一方で、内燃機関車は、そのインフラの普及と継続的な技術進歩により、引き続きリードしています。自動車メーカーは、ガソリンエンジンの効率を高めるために、直接燃料噴射や気筒休止などの低燃費技術を導入しています。同時に、排ガス規制の厳格化により、性能を損なうことなく排ガスを最小限に抑える軽量で耐熱性のあるエンジンバルブの開発が推進されています。

米国のエンジンバルブ市場は2024年に13億米ドルを生み出し、2025年から2034年にかけてCAGR 2.4%で拡大すると予測されています。自動車の電動化へのシフトが加速しているにもかかわらず、エンジンバルブを含む内燃機関車部品の需要は引き続き堅調です。米国の自動車メーカーは、高性能ガソリン車に対する消費者の需要に応えつつ、厳しい排ガス規制への適合を確保するため、耐久性と効率を高める高度なバルブ材料とコーティングに投資しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 市場洞察

- エコシステム分析

- 原材料分析

- 主要ニュースと取り組み

- パートナーシップ/提携

- 合併/買収

- 投資

- 製品上市とイノベーション

- 規制状況

- 影響要因

- 促進要因

- 自動車生産の増加

- バルブ技術の革新

- 厳しい排ガス規制の増加

- 促進要因

- 業界の潜在的リスク&課題

- 自動車用バルブの製造工程における環境問題

- 成長可能性分析

- ポーター分析

- PESTEL分析

- 貿易分析

- 輸出データ

- 輸入データ

第4章 競合情勢

- イントロダクション

- 各社の市場シェア

- 主要市場企業の競合分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:バルブタイプ別、2021年~2034年

- 主要動向

- 中空

- モノメタルバルブ

- バイメタル

第6章 市場推計・予測:目的別、2021年~2034年

- 主要動向

- 吸気バルブ

- 排気バルブ

第7章 市場推計・予測:エンジンタイプ別、2021年~2034年

- 主要動向

- ICE

- 電動

第8章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- ニッケル合金

- クロムメッキ

- ステンレス鋼

- その他(硝酸塩、ステライト合金など)

第9章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 空気圧式

- 油圧式

- 電気式

第10章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 自動車

- 商用車

- 乗用車

- 二輪車

- 船舶用

- 天然ガスエンジン

- 軍事・防衛用途

- 農業・土木機械

- 鉄道・機関車

- 発電機・産業用エンジン

- その他

第11章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第12章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- マレーシア

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- UAE

- 南アフリカ

第13章 企業プロファイル

- AVR(Vikram)Valves

- Bosch

- Continental AG

- Denso

- Eaton Corporation

- Federal-Mogul

- Fuji Oozx

- Grindtech

- Hitachi Ltd

- Rane

The Global Engine Valve Market, valued at USD 6.5 billion in 2024, is set to experience steady growth, projected to expand at a CAGR of 3% between 2025 and 2034. The increasing global demand for fuel-efficient vehicles is a major factor influencing market expansion. With governments worldwide enforcing stricter fuel economy and emissions regulations, automakers are rapidly adopting advanced engine technologies. This has led to a surge in demand for high-performance engine components, particularly valves, which play a pivotal role in combustion efficiency and emission control. Ongoing innovations in engine design, including turbocharging and variable valve timing, are further boosting the need for precision-engineered valves that optimize fuel combustion and enhance overall vehicle performance. As automakers focus on lightweight and durable engine components to meet stringent regulatory requirements, the engine valve market is witnessing significant advancements in material science and manufacturing processes.

The market is segmented based on valve type into hollow, monometallic, and bimetallic valves. The hollow valve segment accounted for USD 2.9 billion in 2024, gaining traction due to its superior lightweight characteristics. Hollow valves offer a significant advantage over solid valves by enabling faster and more precise valve movement, which enhances engine efficiency. These valves are particularly beneficial in high-performance and racing engines where speed and thermal management are crucial. The ability of hollow valves to improve heat dissipation ensures that engines operate at optimal temperatures, thereby extending the lifespan of engine components subjected to high stress and extreme conditions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $8.7 Billion |

| CAGR | 3% |

In terms of engine type, the market is categorized into internal combustion engines (ICE) and electric engines. ICE engines held a dominant 72.5% share in 2024 and are projected to grow at a CAGR of 2.8% through 2034. While electric vehicles are gradually reshaping the automotive landscape, ICE vehicles continue to lead due to their widespread infrastructure and ongoing technological advancements. Automakers are integrating fuel-efficient technologies such as direct fuel injection and cylinder deactivation to enhance the efficiency of gasoline-powered engines. At the same time, stricter emission norms are driving the development of lightweight, heat-resistant engine valves that minimize emissions without compromising performance.

U.S. Engine Valve Market generated USD 1.3 billion in 2024 and is forecasted to expand at a CAGR of 2.4% from 2025 to 2034. Despite the accelerating shift toward vehicle electrification, the demand for ICE components, including engine valves, remains strong. Automakers in the U.S. are investing in advanced valve materials and coatings that enhance durability and efficiency, ensuring compliance with stringent emission regulations while meeting consumer demand for high-performance gasoline-powered vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Market 3600 synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Regional trends

- 2.4 Product type trends

- 2.5 End use trends

- 2.6 Distribution channel trends

Chapter 3 Market Insights

- 3.1 Industry ecosystem analysis

- 3.2 Raw material analysis

- 3.3 Key news and initiatives

- 3.3.1 Partnership/Collaboration

- 3.3.2 Merger/Acquisition

- 3.3.3 Investment

- 3.3.4 Product launch & innovation

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Increase production of vehicles

- 3.5.1.2 Increase innovation in valve technology

- 3.5.1.3 Rise in stringent emission regulations

- 3.5.1 Growth drivers

- 3.6 Industry pitfalls & challenges

- 3.6.1.1 Manufacturing process of automotive valves involves environmental concerns

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade analysis

- 3.10.1 Export data

- 3.10.2 Import data

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share, 2024

- 4.3 Competitive analysis of major market players, 2024

- 4.4 Competitive positioning matrix, 2024

- 4.5 Strategic outlook matrix, 2024

Chapter 5 Market Estimates & Forecast, By Valve Type 2021 - 2034, (USD Billion)

- 5.1 Key trends

- 5.2 Hollow

- 5.3 Monometallic

- 5.4 Bimetallic

Chapter 6 Market Estimates & Forecast, By Purpose 2021 - 2034, (USD Billion)

- 6.1 Key trends

- 6.2 Intake valves

- 6.3 Exhaust valves

Chapter 7 Market Estimates & Forecast, By Engine type 2021 - 2034, (USD Billion)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric

Chapter 8 Market Estimates & Forecast, By Material 2021 - 2034, (USD Billion)

- 8.1 Key trends

- 8.2 Nickel alloy

- 8.3 Chrome plated

- 8.4 Stainless steel

- 8.5 Others (Nitrate, Stellite Alloy, etc.)

Chapter 9 Market Estimates & Forecast, By Technology 2021 - 2034, (USD Billion)

- 9.1 Key trends

- 9.2 Pneumatic

- 9.3 Hydraulic

- 9.4 Electric

Chapter 10 Market Estimates & Forecast, By Application 2021 - 2034, (USD Billion)

- 10.1 Key trends

- 10.2 Automotive

- 10.2.1 Commercial vehicle

- 10.2.2 Passenger vehicle

- 10.2.3 Two wheelers

- 10.3 Marine applications

- 10.4 Natural gas engines

- 10.5 Military & defense applications

- 10.6 Agricultural & earth moving machinery

- 10.7 Railway & locomotive applications

- 10.8 Generators & industrial engines

- 10.9 Others

Chapter 11 Market Estimates & Forecast, By Distribution Channel 2021 - 2034, (USD Billion)

- 11.1 Key trends

- 11.2 OEM

- 11.3 Aftermarket

Chapter 12 Market Estimates & Forecast, By Region 2021 - 2034, (USD Billion)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Malaysia

- 12.4.7 Indonesia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.6 MEA

- 12.6.1 Saudi Arabia

- 12.6.2 UAE

- 12.6.3 South Africa

Chapter 13 Company Profiles

- 13.1 AVR (Vikram) Valves

- 13.2 Bosch

- 13.3 Continental AG

- 13.4 Denso

- 13.5 Eaton Corporation

- 13.6 Federal-Mogul

- 13.7 Fuji Oozx

- 13.8 Grindtech

- 13.9 Hitachi Ltd

- 13.10 Rane