|

市場調査レポート

商品コード

1822613

聴覚デバイスの市場機会と促進要因、産業動向分析、2025年~2034年予測Audiology Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 聴覚デバイスの市場機会と促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年08月29日

発行: Global Market Insights Inc.

ページ情報: 英文 165 Pages

納期: 2~3営業日

|

概要

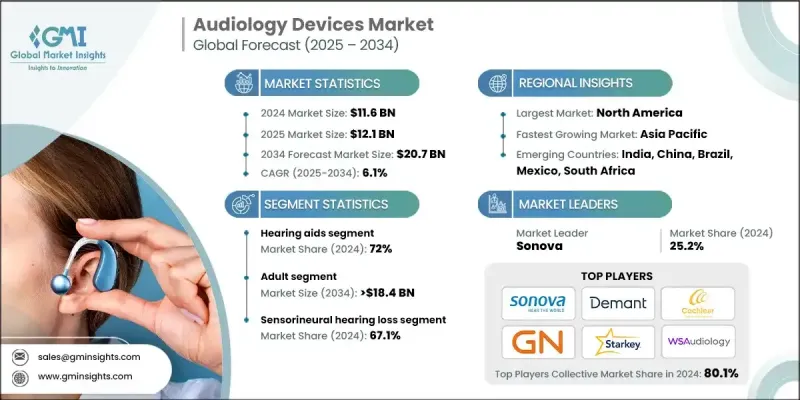

Global Market Insights Inc.が発行した最新レポートによると、聴覚デバイスの世界市場は2024年に116億米ドルと推定され、CAGR 6.1%で2025年の121億米ドルから2034年には207億米ドルに成長すると予測されています。

世界的な難聴罹患率の増加は、聴覚デバイス市場の主要促進要因です。平均寿命が延び、世界人口の高齢化が進むにつれて、老眼としても知られる加齢による聴覚障害がますます一般的になってきています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 116億米ドル |

| 予測金額 | 207億米ドル |

| CAGR | 6.1% |

補聴器需要の高まり

補聴器分野は、継続的な技術革新と、目立たず使いやすい製品に対する需要の高まりにより、2024年に注目すべきシェアを占めました。最近の補聴器は、Bluetooth接続、AIによる音質向上、ノイズキャンセリング、充電式電池などの高度な機能を備えています。これらの機能は、デジタルライフスタイルとのシームレスな統合を求める技術に精通した消費者にアピールしています。

成人が牽引役に

成人向けセグメントは、加齢に伴う難聴の有病率の高さから、2024年に大きな収益を上げました。より多くの成人がアクティブなライフスタイルをサポートするソリューションを求める中、自然な音質と長い電池寿命を提供する、高性能でメンテナンスの少ない機器への需要が高まっています。また、成人は定期的な聴力検査を受ける傾向が高く、診断率や治療率の向上につながります。メーカーはこの層をターゲットに、自立、コミュニケーション、生活の質を強調したマーケティングを行っています。

感音性難聴の有病率の増加

感音性難聴分野は2024年に持続可能な収益を上げました。感音性難聴は、一般的に内耳や聴神経の損傷によって引き起こされ、多くの場合回復不能であり、長期的な機器サポートが必要です。補聴器と人工内耳が主な解決策であり、機器の性能は重症度に応じて調整されます。各社は、より自然な聴こえを模倣し、複雑な音環境に適応する機器を開発するため、研究開発に多額の投資を行っています。音声認識とリアルタイム音声処理における革新は、騒がしい環境でも明瞭さと快適さを向上させるのに役立っています。

地域別洞察

北米が推進力のある地域として台頭

北米聴覚デバイス市場は、高度なヘルスケアインフラ、有利な償還政策、早期難聴診断の強固な文化に牽引され、2024年に大きなシェアを占めました。米国は、高齢化と消費者意識の高まりに後押しされ、30億米ドルを超える金額で毎年着実に成長しており、この地域市場を独占しています。企業は、聴覚クリニック・ネットワークの拡大、オンライン小売プラットフォームの強化、聴覚ケアの旅への遠隔医療ソリューションの統合により、北米での地位を強化しています。

聴覚デバイス市場の主要企業は、EARGO、Demant、NUROTRON、ENVOY MEDICAL、WS Audiology、Medtronic、GN Store Nord、MAICO、RION、EARTECHNIC、MED-EL Medical、Starkey、Cochlear、American Diagnostic Corporation、Sonovaです。

聴覚デバイス市場の主要企業は、その存在感を確固たるものにするため、多方面からのアプローチを採用しています。革新は依然として中心であり、進化するユーザーの期待に応えるため、小型化、AIベースの音声処理、ワイヤレス接続への投資を継続しています。多くの企業は、遠隔医療プロバイダーや小売薬局チェーンと戦略的提携を結び、販売網を広げています。さらに、パーソナライズされたフィッティング技術、デバイスコントロールのためのモバイルアプリ、生涯サービスプランを通じて、顧客体験が優先されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 世界的に難聴の有病率が増加

- eコマースチャネルの好感度が高まっている

- 聴覚デバイスにおける技術の進歩

- 先進国における有利な償還政策

- 業界の潜在的リスク&課題

- 高度な聴覚デバイスの高コスト

- 低所得国における意識の欠如

- 市場機会

- 補聴器におけるAIと機械学習の統合

- 遠隔聴覚検査と遠隔聴覚サービスに対する需要の増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 米国

- 欧州

- テクノロジーの情勢

- 払い戻しシナリオ

- 地域別の価格分析

- 消費者経路

- 従来の経路

- 新たな道筋の必要性

- ハイブリッド経路

- 消費者洞察

- 政策の情勢

- ギャップ分析

- リスク管理分析

- 研究開発

- オペレーション

- マーケティングと販売

- 品質

- 知的財産権

- 規制

- 情報技術

- 気候

- 金融

- ポーター分析

- PESTEL分析

- 将来の市場動向

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 地域別

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 補聴器

- タイプ別

- 耳かけ型(BTE)

- 耳内受信機/外耳道受信機(RITE/RIC)

- 完全に根管内にある/根管内に見えない(CIC/IIC)

- 耳の中に装着するタイプ(ITE)

- 耳道内(ITC)

- 流通チャネル別

- 店舗

- eコマース

- タイプ別

- 人工内耳

- 片側インプラント

- 両側インプラント

- 診断装置

- ティンパノメーター

- 聴力計

- 耳鏡

- 骨伝導補聴器(BAHA)

- 中耳インプラント(MEI)

第6章 市場推計・予測:患者別、2021-2034

- 主要動向

- 成人用

- 小児

第7章 市場推計・予測:難聴別、2021-2034

- 主要動向

- 感音難聴

- 伝音性難聴

- 混合性難聴

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- American Diagnostic Corporation

- Cochlear

- Demant

- EARGO

- EARTECHNIC

- ENVOY MEDICAL

- GN Store Nord

- MAICO

- MED-EL Medical

- Medtronic

- NUROTRON

- RION

- sonova

- Starkey

- WS Audiology