|

市場調査レポート

商品コード

1698541

発電用ガスタービン市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Power Generation Gas Turbine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 発電用ガスタービン市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月06日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

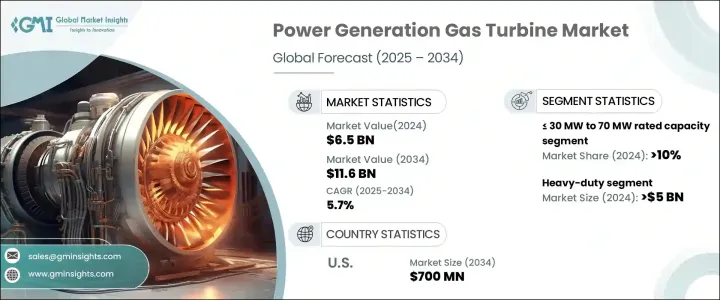

発電用ガスタービンの世界市場は、2024年に65億米ドルと評価され、2025年から2034年にかけてCAGR 5.7%で拡大すると予測されています。

よりクリーンなエネルギー源への移行と、効率的で持続可能な発電ソリューションへのニーズの高まりが、業界の成長を後押ししています。消費者の意識の高まりと、二酸化炭素排出量削減のための厳しい規制が相まって、発電用ガスタービンの需要を促進しています。ガスタービンは、送電網の信頼性と再生可能エネルギー統合のバランスを取る上で重要な役割を果たすため、石炭火力発電所から天然ガスをベースとする代替発電所へのシフトが採用を加速しています。ガスタービンによる発電の割合が高まる中、急速な都市化、産業拡大、人口増加に支えられ、市場は進化を続けています。老朽化した発電所の近代化が求められる中、先進的なガスタービン技術は世界のエネルギー需要を満たす上で不可欠なものとなっています。

ガスタービンは、その効率性と迅速な応答時間により、発電において依然として好ましい選択肢です。これらのシステムは、燃料の化学エネルギーを機械エネルギーに変換し、それを電気に変換します。再生可能エネルギー源の統合、タービン設計の進歩、水素混合タービンの導入拡大が市場の見通しを高めています。特にオフグリッドや遠隔地での分散型電源システムの拡大が、小型・中型ガスタービンの需要を促進しています。ネット・ゼロ・エミッションの達成に向けた開発の強化は、代替燃料で作動するよう開発されている次世代タービンの採用をさらに後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 65億米ドル |

| 予測金額 | 116億米ドル |

| CAGR | 5.7% |

同市場は、タービン容量に基づいて<=30 MW to 70 MW,>70MWから200MW、200MW超に分類されます。<=30MWから70MWの範囲のシステムが2024年の市場の10%以上を占め、その効率性、費用対効果、複合サイクルプラントやガス化プラントでの広範な応用が支持されています。翼やコーティングを含むタービン部品の継続的な進化は、運転性能と信頼性を高めています。

設計によって、この業界は航空転用型ガスタービンと大型ガスタービンに分けられます。大型ガスタービン・セグメントは、複合サイクル・ガスタービン(CCGT)プラントでの広範な使用と再生可能エネルギーを補完する能力によって、2024年には50億米ドルのシェアを占める。2024年に10億米ドルと評価された航空転用分野は、送電網へのアクセスが限られている地域での効率性により、牽引力を増しています。大量の電力を必要とするデータセンターの成長も、航空転用タービンの需要を促進しています。

市場はさらに、オープンサイクルとコンバインドサイクルシステムに区別されます。複合サイクルタービンは2024年に50億米ドル以上を占めるが、オープンサイクルタービンは2034年までCAGR 5%で成長すると予想されます。オープンサイクルタービンは、迅速な始動、多用途性、冷却要件の低さが好まれています。コンバインドサイクル分野は、産業の成長、エネルギー効率の義務化、排出量削減を目的とした政府政策に牽引され、2034年までのCAGRが5.5%を超えると予測されます。

米国市場は、水素燃焼技術や低炭素エネルギー源への投資の増加に支えられ、2034年までに7億米ドルを超えると予想されます。北米のガスタービン産業は、豊富な天然ガス供給と採掘技術の進歩の恩恵を受けて、2034年までCAGR 5.5%で拡大すると予測されます。複合サイクル発電所の継続的な開発とガスタービン効率の向上は、業界の拡大を促進する上で重要な役割を果たすと思われます。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 市場推計・予測パラメータ

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:容量別、2021年~2034年

- 主要動向

- 30MW~70MW

- 70MW~200MW

- 200MW超

第6章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- 航空転用

- ヘビーデューティー

第7章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- オープンサイクル

- コンバインドサイクル

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- オランダ

- フィンランド

- ギリシャ

- デンマーク

- ルーマニア

- ポーランド

- スウェーデン

- アジア太平洋

- 中国

- オーストラリア

- 日本

- 韓国

- インドネシア

- タイ

- マレーシア

- バングラデシュ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- クウェート

- オマーン

- エジプト

- トルコ

- バーレーン

- イラク

- ヨルダン

- レバノン

- 南アフリカ

- ナイジェリア

- アルジェリア

- ケニア

- ガーナ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- ペルー

- チリ

第9章 企業プロファイル

- Ansaldo Energia

- Bharat Heavy Electricals Limited(BHEL)

- Flex Energy Solutions

- GE Vernova

- Harbin Electric

- JSC United Engine

- Kawasaki Heavy Industries

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Opra Turbines

- Rolls Royce

- Siemens

- Solar Turbines

- TotalEnergies

- Wartsila

- Zorya-Mashproekt

The Global Power Generation Gas Turbine Market, valued at USD 6.5 billion in 2024, is projected to expand at a CAGR of 5.7% from 2025 to 2034. The transition toward cleaner energy sources and the rising need for efficient and sustainable power generation solutions are driving industry growth. Increasing consumer awareness, combined with stringent regulations to reduce carbon emissions, is fostering demand for gas turbines in power generation. The shift from coal-fired power plants to natural gas-based alternatives is accelerating adoption, as gas turbines play a key role in balancing grid reliability and renewable energy integration. With an increasing share of electricity generation coming from gas turbines, the market continues to evolve, supported by rapid urbanization, industrial expansion, and population growth. As aging power plants require modernization, advanced gas turbine technologies are becoming essential in meeting the global energy demand.

Gas turbines remain a preferred choice in power generation due to their efficiency and rapid response time. These systems convert the chemical energy of fuel into mechanical energy, which is then transformed into electricity. The integration of renewable energy sources, advancements in turbine designs, and the growing deployment of hydrogen-blend turbines are enhancing market prospects. The expansion of distributed power systems, especially in off-grid and remote locations, is driving demand for small and medium-sized gas turbines. Increased focus on achieving net-zero emissions is further boosting the adoption of next-generation turbines, which are being developed to operate on alternative fuels.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $11.6 Billion |

| CAGR | 5.7% |

The market is categorized based on capacity into turbines ranging from <= 30 MW to 70 MW, > 70 MW to 200 MW, and > 200 MW. Systems within the <= 30 MW to 70 MW range accounted for over 10% of the market in 2024, favored for their efficiency, cost-effectiveness, and widespread application in combined cycle and gasification plants. The continuous evolution of turbine components, including airfoils and coatings, is enhancing operational performance and reliability.

By design, the industry is divided into aeroderivative and heavy-duty gas turbines. The heavy-duty segment held a USD 5 billion share in 2024, driven by extensive use in combined cycle gas turbine (CCGT) plants and the ability to complement renewable energy. The aeroderivative segment, valued at USD 1 billion in 2024, is gaining traction due to its efficiency in regions with limited grid access. The growth of data centers, with their substantial power requirements, is also fueling demand for aeroderivative turbines.

The market further differentiates into open cycle and combined cycle systems. While combined cycle turbines accounted for over USD 5 billion in 2024, open cycle turbines are expected to grow at a CAGR of 5% through 2034. Open cycle turbines are favored for their quick startup, versatility, and lower cooling requirements. The combined cycle segment is projected to witness a CAGR of over 5.5% through 2034, driven by industrial growth, energy efficiency mandates, and government policies aimed at reducing emissions.

The U.S. market is expected to surpass USD 700 million by 2034, supported by increased investment in hydrogen combustion technologies and low-carbon energy sources. North America's gas turbine industry is projected to expand at a CAGR of 5.5% through 2034, benefiting from an abundant natural gas supply and advancements in extraction technologies. The continued development of combined cycle power plants and improvements in gas turbine efficiency will play a significant role in driving the industry's expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 – 2034 (MW & USD Million)

- 5.1 Key trends

- 5.2 ≤ 30 MW to 70 MW

- 5.3 > 70 MW to 200 MW

- 5.4 > 200 MW

Chapter 6 Market Size and Forecast, By Product, 2021 – 2034 (MW & USD Million)

- 6.1 Key trends

- 6.2 Aero-derivative

- 6.3 Heavy duty

Chapter 7 Market Size and Forecast, By Technology, 2021 – 2034 (MW & USD Million)

- 7.1 Key trends

- 7.2 Open cycle

- 7.3 Combined cycle

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (MW & USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Finland

- 8.3.8 Greece

- 8.3.9 Denmark

- 8.3.10 Romania

- 8.3.11 Poland

- 8.3.12 Sweden

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Indonesia

- 8.4.6 Thailand

- 8.4.7 Malaysia

- 8.4.8 Bangladesh

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Kuwait

- 8.5.5 Oman

- 8.5.6 Egypt

- 8.5.7 Turkey

- 8.5.8 Bahrain

- 8.5.9 Iraq

- 8.5.10 Jordan

- 8.5.11 Lebanon

- 8.5.12 South Africa

- 8.5.13 Nigeria

- 8.5.14 Algeria

- 8.5.15 Kenya

- 8.5.16 Ghana

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Peru

- 8.6.4 Chile

Chapter 9 Company Profiles

- 9.1 Ansaldo Energia

- 9.2 Bharat Heavy Electricals Limited (BHEL)

- 9.3 Flex Energy Solutions

- 9.4 GE Vernova

- 9.5 Harbin Electric

- 9.6 JSC United Engine

- 9.7 Kawasaki Heavy Industries

- 9.8 MAN Energy Solutions

- 9.9 Mitsubishi Heavy Industries

- 9.10 Opra Turbines

- 9.11 Rolls Royce

- 9.12 Siemens

- 9.13 Solar Turbines

- 9.14 TotalEnergies

- 9.15 Wartsila

- 9.16 Zorya-Mashproekt