|

市場調査レポート

商品コード

1892881

スペアパーツ物流市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Spare Parts Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| スペアパーツ物流市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月09日

発行: Global Market Insights Inc.

ページ情報: 英文 230 Pages

納期: 2~3営業日

|

概要

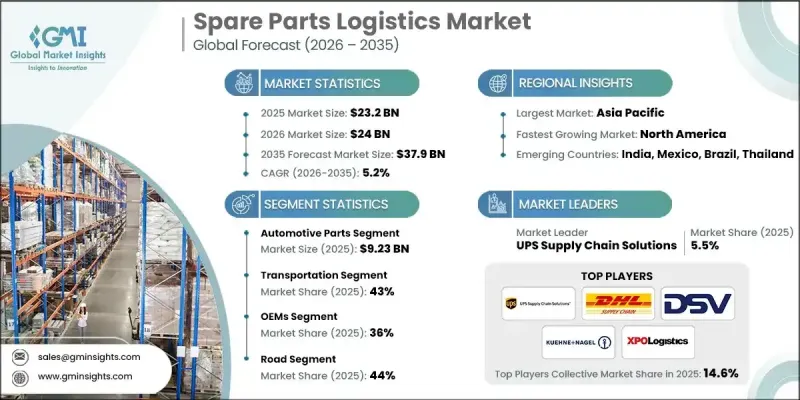

世界のスペアパーツ物流市場は、2025年に232億米ドルと評価され、2035年までにCAGR5.2%で成長し、379億米ドルに達すると予測されております。

この成長は、世界的に拡大する自動車、産業用、電子機器のフリート(車両・設備群)に起因しており、定期・不定期のメンテナンス需要の増加を生み出しています。企業、フリート運営者、エンドユーザーは、大量のSKU(在庫管理単位)、時間厳守の配送、多層的な流通システムを効率的に処理し、稼働停止時間を最小限に抑えるため、効率的なスペアパーツ物流ネットワークへの依存度を高めています。OEM(オリジナル・エクイップメント・メーカー)や物流プロバイダーは、可視性、追跡、予測能力を強化するため、デジタルトランスフォーメーション(変革)を推進しています。クラウドプラットフォーム、IoTセンサー、リアルタイム分析により、在庫管理の最適化、注文処理の迅速化、エラー削減が実現されます。B2BおよびB2Cマーケットプレースの台頭は顧客の期待を再構築し、プロバイダーは小口・高頻度・地理的に分散した配送に注力するよう促されています。これらの進展はサービスレベル契約を強化し、稼働時間の保証を確保するとともに、サプライチェーン全体の効率性を高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 232億米ドル |

| 予測金額 | 379億米ドル |

| CAGR | 5.2% |

自動車部品セグメントは2025年に92億3,000万米ドルを占め、2035年までCAGR 4.5%で成長すると予測されています。この成長は、自動車台数の増加、旧型車への需要拡大、オンライン販売の加速によって支えられています。デジタルソリューションは、出荷の迅速化、効率的なラストマイル配送、複数倉庫戦略を推進しています。OEMメーカーとアフターマーケットサプライヤーは、進化する流通ニーズに対応するため、自動倉庫システムと統合物流プラットフォームに多額の投資を行っています。

輸送セグメントは2025年に43%のシェアを占め、2026年から2035年にかけてCAGR 6.4%で成長すると予測されています。スペアパーツ物流はトラック、鉄道、航空、海上輸送に大きく依存しています。電子商取引の成長、迅速な配送への期待、そしてより効率的な在庫戦略が、高度な輸送ネットワークの必要性を高めています。貨物コストの変動や地政学的混乱といった課題があるにもかかわらず、プロバイダーは回復力と対応力を確保するため、経路最適化やキャパシティ管理システムを備えたマルチモーダルネットワークを開発しています。

米国スペアパーツ物流市場は2025年に86%のシェアを占め、48億7,000万米ドルの規模となりました。電子商取引の成長に伴い、追加のフルフィルメントセンター、都市部におけるマイクロフルフィルメントハブ、当日配送、高度な追跡システムへの需要が高まっており、これにより複数産業にわたるアフターマーケットサービス能力の向上が図られています。

よくあるご質問

目次

第1章 調査手法

- 市場範囲と定義

- 調査設計

- 調査アプローチ

- データ収集方法

- データマイニングの情報源

- 世界

- 地域別/国別

- 基本推定値と計算

- 基準年計算

- 市場推定における主要な動向

- 1次調査と検証

- 一次情報

- 予測

- 調査前提条件と制限事項

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 予知保全の導入状況

- 電子商取引部品の拡大

- OEM垂直統合

- 物流の自動化とロボティクス

- 設備の電化と部品の複雑化が進んでいます

- 業界の潜在的リスク&課題

- 在庫管理の高度な複雑性

- 輸送コストの変動性

- 市場機会

- 地域密着型生産のための積層造形技術

- AIを活用した需要予測

- デジタルマーケットプレースの拡大

- 持続可能性とグリーンロジスティクス

- 促進要因

- 成長可能性分析

- 規制情勢

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現行技術

- 新興技術

- 特許分析

- 価格分析

- 地域別

- 製品別

- コスト内訳分析

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主なニュースと取り組み

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:部品別、2022-2035

- 主要動向

- 自動車部品

- エンジン部品

- ピストン

- フィルター

- その他

- トランスミッションおよび駆動系部品

- ブレーキ

- サスペンション

- ステアリングシステム

- ボディおよび外装部品

- 電気・電子システム

- アフターマーケット消耗品

- エンジン部品

- 産業機械・設備部品

- 製造機械部品

- モーター

- 歯車

- ベルト

- 建設機械部品

- 掘削機

- ローダー

- 農業機械部品

- トラクター

- 収穫機

- マテリアルハンドリングおよび物流機器の構成部品

- 油圧、空圧、および機械式サブシステム

- 製造機械部品

- 航空宇宙・防衛用スペアパーツ

- 航空機部品

- 防衛車両部品

- 地上支援・整備機器

- 電子部品・半導体部品

- 半導体デバイス

- 通信機器部品

- エネルギー・公益事業向け部品

- その他

第6章 市場推計・予測:サービス別、2022-2035

- 主要動向

- 輸送

- 倉庫保管

- 流通

- 在庫管理

第7章 市場推計・予測:最終用途別、2022-2035

- 主要動向

- OEMメーカー(オリジナル・エクイップメント・メーカー)

- アフターマーケット供給業者

- 販売店

- 電子商取引プラットフォーム

- その他

第8章 市場推計・予測:輸送手段別、2022-2035

- 主要動向

- 道路

- 鉄道

- 航空

- 海上輸送

第9章 市場推計・予測:地域別、2022-2035

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- オランダ

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- ANZ

- シンガポール

- タイ

- ベトナム

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- 世界プレイヤー

- Agility Logistics

- Bollore Logistics

- C.H. Robinson

- CEVA Logistics

- DB Schenker

- DHL Supply Chain

- DSV Panalpina

- Expeditors International

- FedEx Supply Chain

- Hellmann Worldwide Logistics

- Kuehne+Nagel

- UPS Supply Chain Solutions

- XPO Logistics

- 地域プレイヤー

- Ryder System

- Penske Logistics

- J.B. Hunt Transport Services

- BLG Logistics

- Nippon Express

- Kerry Logistics

- Yusen Logistics

- Kintetsu World Express

- COSCO Shipping Logistics

- 新興企業とディスラプター

- Overhaul

- FourKites

- Shippeo

- Convoy

- Transfix

- Shippo

- Locus Robotics

- Imperial Logistics