|

市場調査レポート

商品コード

1750555

網膜障害治療の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Retinal Disorder Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 網膜障害治療の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月09日

発行: Global Market Insights Inc.

ページ情報: 英文 138 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

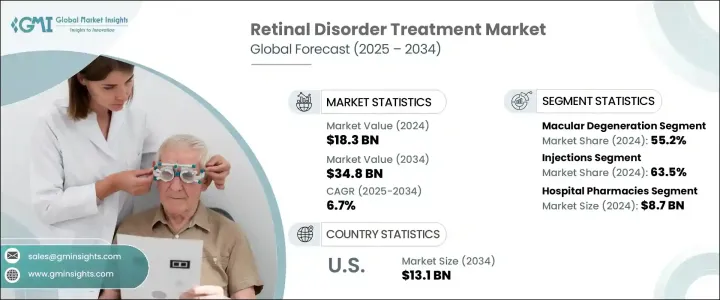

世界の網膜障害治療市場は、2024年に183億米ドルと評価され、糖尿病網膜症(DR)や糖尿病黄斑浮腫(DME)などの合併症とともに糖尿病の有病率の増加に牽引され、CAGR 6.7%で成長し、2034年には348億米ドルに達すると推定されています。

網膜障害の治療には、抗VEGF注射、レーザー治療、コルチコステロイド治療、硝子体手術など、内科的、外科的、薬学的介入が含まれます。これらの治療の主な目的は、網膜障害の拡大を防ぎ、視力を維持または回復することです。治療法の選択は、症状の重症度、障害の段階、患者さんの眼全体の健康状態によって異なります。DMEは、特に2型糖尿病患者の視力低下の主な原因であり、タイムリーな介入と専門的治療の必要性が強調されています。

徐放性眼内治療薬など最近の治療法の進歩は、注射の頻度を減らすことで患者のコンプライアンスを向上させています。例えば、ある種の注射器はドラッグデリバリーを持続するように設計されており、頻繁な眼球注射から解放されます。このような技術革新は、網膜疾患のより効果的な解決策を提供すると同時に、治療負担を最小限に抑えるのに役立っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 183億米ドル |

| 予測金額 | 348億米ドル |

| CAGR | 6.7% |

2024年の市場は、黄斑変性症、特に加齢黄斑変性症(AMD)が55%のシェアを占めました。AMDは主に60歳以上に発症し、この年齢層における視力低下の主な原因の一つです。世界人口の高齢化に伴い、高血圧や肥満などの合併症がAMDの有病率をさらに悪化させ、継続的な調査と治療革新の必要性を促しています。

注射分野は市場の主要な牽引役であり、2024年には63.5%のシェアを占める。硝子体内注射は、AMD、網膜静脈閉塞症、DMEなどの網膜疾患の治療に一般的に使用されています。抗VEGF療法は迅速な治療効果をもたらすため、これらの疾患の治療において有望な結果を示しています。Avastin、Eylea、Lucentisなどの薬剤は、網膜浮腫や新生血管の減少に有効であることが証明されており、最終的には患者の視力を改善しています。

米国網膜障害治療網膜疾患に罹患しやすい人口の高齢化と高度な硝子体内注射療法の普及により、米国市場は2024年の71億米ドルから2034年には131億米ドルに成長する見通しです。さらに、有利な償還政策と主要製薬メーカーの強力なプレゼンスが引き続き市場拡大に拍車をかけています。

世界網膜障害治療市場の主要企業には、Regeneron Pharmaceuticals、Bayer、AbbVie、Novartis、Pfizer、F. Hoffmann-La Rocheなどがあります。これらの企業は、競合情勢で優位に立つため、研究開発や新製品開発に投資しています。網膜障害治療市場における地位を強化するため、各社は製品ポートフォリオの拡充と治療技術の進歩に注力しています。主な発展戦略としては、医薬品開発や流通における補完的な専門知識を活用するためのパートナーシップの形成が挙げられます。さらに、企業は革新的なドラッグデリバリーシステムや償還構造の改善を通じて、患者の治療を強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 糖尿病の有病率の増加

- 高齢化人口の増加

- 技術的進歩

- 意識向上とスクリーニングプログラムの強化

- 業界の潜在的リスク&課題

- 治療費が高め

- 副作用と安全性の懸念

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 国別の対応

- 業界への影響

- 供給側の影響(製造コスト)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(消費者へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(製造コスト)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 技術的情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- 黄斑変性

- 湿性黄斑変性症

- 乾性黄斑変性

- 糖尿病網膜症

- 遺伝性網膜疾患(IRD)

- 糖尿病黄斑浮腫

- 網膜静脈閉塞症

- その他のタイプ

第6章 市場推計・予測:剤形別、2021-2034

- 主要動向

- カプセルと錠剤

- 目薬

- 目のソリューション

- ゲル

- 軟膏

- 注射

第7章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 病院薬局

- 小売薬局

- オンライン薬局

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- AbbVie

- Alimera Sciences

- Amgen

- Apellis Pharmaceuticals

- Astellas Pharma

- Bayer

- Biogen

- Bausch+Lomb

- Celltrion

- F. Hoffmann-La Roche

- Novartis

- Pfizer

- Regeneron Pharmaceutical

- Santen Pharmaceuticals

- Sandoz Group

The Global Retinal Disorder Treatment Market was valued at USD 18.3 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 34.8 billion by 2034, driven by the increasing prevalence of diabetes, along with its complications such as diabetic retinopathy (DR) and diabetic macular edema (DME). Retinal disorder treatments encompass a range of medical, surgical, and pharmaceutical interventions, including anti-VEGF injections, laser therapy, corticosteroid treatments, and vitrectomy. The primary goal of these treatments is to prevent further retinal damage and preserve or restore vision. The selection of a treatment depends on the severity of the condition, the stage of the disorder, and the overall health of the patient's eye. DME is a leading cause of vision loss, particularly among individuals with type 2 diabetes, highlighting the need for timely interventions and specialized care.

Recent advancements in treatment methods, such as sustained-release intraocular therapies, enhance patient compliance by reducing the frequency of injections. For example, certain injectable devices are designed for continuous drug delivery, offering relief from frequent eye injections. These innovations are helping to minimize the treatment burden while providing more effective solutions for retinal disorders.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.3 Billion |

| Forecast Value | $34.8 Billion |

| CAGR | 6.7% |

Macular degeneration, particularly age-related macular degeneration (AMD), dominated the market in 2024, accounting for a 55% share. AMD, which primarily affects individuals over 60 years old, is one of the leading causes of vision loss in this age group. As the global population ages, comorbidities such as hypertension and obesity further exacerbate the prevalence of AMD, driving the need for continued research and treatment innovation.

The injection segment is a key driver in the market, accounting for 63.5% share in 2024. Intravitreal injections are commonly used for treating retinal conditions like AMD, retinal vein occlusion, and DME. Anti-VEGF therapies have shown promising results in treating these conditions, as they offer rapid therapeutic responses. Drugs such as Avastin, Eylea, and Lucentis are proving effective in reducing retinal edema and neovascularization, ultimately improving visual acuity for patients.

United States Retinal Disorder Treatment Market is poised to grow from USD 7.1 billion in 2024 to USD 13.1 billion by 2034, driven by the aging population susceptible to retinal conditions and the widespread availability of advanced intravitreal injection therapies. Moreover, favorable reimbursement policies and the strong presence of key pharmaceutical manufacturers continue to fuel market expansion.

Key players in the Global Retinal Disorder Treatment Market include Regeneron Pharmaceuticals, Bayer, AbbVie, Novartis, Pfizer, and F. Hoffmann-La Roche. These companies are investing in R&D and new product development to stay ahead in the competitive landscape. To strengthen their position in the retinal disorder treatment market, companies are focusing on expanding their product portfolios and advancing treatment technologies. Key strategies include forming partnerships to leverage complementary expertise in drug development and distribution. Furthermore, companies are enhancing patient treatment through innovative drug delivery systems and improved reimbursement structures.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of diabetes

- 3.2.1.2 Rising geriatric population

- 3.2.1.3 Technological advancements

- 3.2.1.4 Rising awareness and screening programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment cost

- 3.2.2.2 Side effects and safety concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Macular degeneration

- 5.2.1 Wet macular degeneration

- 5.2.2 Dry macular degeneration

- 5.3 Diabetic retinopathy

- 5.4 Inherited retinal diseases (IRDs)

- 5.5 Diabetic macular edema

- 5.6 Retinal vein occlusion

- 5.7 Other types

Chapter 6 Market Estimates and Forecast, By Dosage Form, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Capsules and tablets

- 6.3 Eye drops

- 6.4 Eye solutions

- 6.5 Gels

- 6.6 Ointments

- 6.7 Injections

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 Online pharmacies

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AbbVie

- 9.2 Alimera Sciences

- 9.3 Amgen

- 9.4 Apellis Pharmaceuticals

- 9.5 Astellas Pharma

- 9.6 Bayer

- 9.7 Biogen

- 9.8 Bausch + Lomb

- 9.9 Celltrion

- 9.10 F. Hoffmann-La Roche

- 9.11 Novartis

- 9.12 Pfizer

- 9.13 Regeneron Pharmaceutical

- 9.14 Santen Pharmaceuticals

- 9.15 Sandoz Group