|

市場調査レポート

商品コード

1913382

分散型ID市場:市場機会、成長促進要因、産業動向分析、将来予測(2026~2035年)Decentralized Identity Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 分散型ID市場:市場機会、成長促進要因、産業動向分析、将来予測(2026~2035年) |

|

出版日: 2025年12月18日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

概要

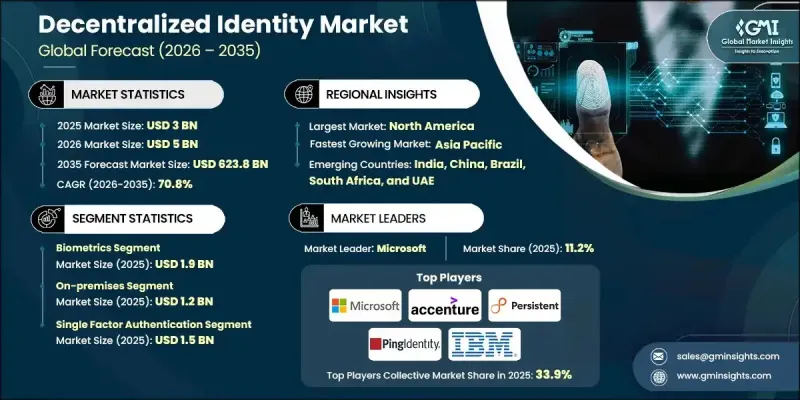

世界の分散型ID市場は、2025年に30億米ドルと評価され、2035年までにCAGR70.8%で成長し、6,238億米ドルに達すると予測されています。

この急速な成長は、プライバシー、セキュリティ、ユーザー制御を重視するデジタルIDエコシステムへの世界の移行によって推進されています。政府や企業は、公共・民間プラットフォームを横断した安全なデジタル交流を支援するため、分散型IDフレームワークの導入を加速させています。データ保護、本人確認、コンプライアンスに関連する規制要件が導入を加速させる一方、デジタルサービスの拡大は信頼性の高いIDオンボーディングソリューションへの需要を継続的に増加させています。セキュアなデジタルIDウォレットは、再利用可能で暗号的に検証された認証情報を可能にし、反復的な認証プロセスと運用上の摩擦を軽減します。これらのシステムは、ユーザーのプライバシーを保護しながらコンプライアンスコストも削減します。複数の地域にわたる規制イニシアチブがこの勢いを強化しており、国境や業界を超えたデジタルエンゲージメントを支援する標準化され相互運用可能なIDインフラストラクチャを促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026~2035年 |

| 当初の市場規模 | 30億米ドル |

| 市場規模予測 | 6,238億米ドル |

| CAGR | 70.8% |

生体認証セグメントは2025年に19億米ドルに達しました。身元情報の悪用や高度ななりすまし技術に関する懸念の高まりが、より高い保証レベルを提供する生体認証ベースの認証手段への需要を牽引しています。規制対象業界では、分散型IDシステムの基盤要素として生体認証への依存度が高まっており、安全で改ざん耐性のある検証プロセスを支えています。

オンプレミス展開モデルは2025年に12億米ドルの市場規模を生み出しました。厳格なデータガバナンスと主権要件を持つ組織は、機密情報に対する完全な管理権限を維持するため、オンプレミス型の分散型IDプラットフォームを好んで採用しています。これらのソリューションはカスタマイズ性、既存のID管理インフラとのシームレスな統合、内部セキュリティフレームワークの適用を可能にします。

米国の分散型ID市場は2025年に9億2,430万米ドルに達し、2026年から2035年にかけてCAGR66.7%で成長すると予測されています。市場成長は、ブロックチェーン対応デジタルウォレットへの投資増加や企業向けID統合イニシアチブによって支えられています。公共部門の枠組みと業界標準が、複数の規制対象分野における採用を加速させており、技術プロバイダーは先進的なクラウドベースソリューションや共同開発プログラムへの投資を促されています。

よくあるご質問

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界のエコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- 業界への影響要因

- 促進要因

- 政府主導のデジタルIDプログラム

- 増加する詐欺、データ侵害、および個人情報盗難のコスト

- 効率化とコンプライアンス対応を両立したオンボーディングに対する企業のニーズ

- Web3、トークン化された資産、デジタルウォレットエコシステムの成長

- マルチクラウドおよびゼロトラスト導入の増加

- 業界の潜在的リスクと課題

- 世界な信頼フレームワークと法的認知の欠如

- ユーザー体験の低さと相互運用性のギャップ

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターのファイブフォース分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 新興ビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 消費者心理分析

- 特許・知的財産分析

- 地政学的・貿易動向

第4章 競合情勢

- イントロダクション

- 企業別の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 市場集中度の分析

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオ比較

- 製品ラインの幅広さ

- 技術

- イノベーション

- 事業展開状況の比較:地域別

- 世界の展開状況の分析

- サービスネットワークカバレッジ

- 地域別の市場浸透率

- 競合ポジショニング・マトリックス

- リーダー

- チャレンジャー

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績比較

- 主な発展(2022~2035年)

- 企業合併・買収 (M&A)

- 事業提携・協力

- 技術進歩

- 拡大・投資戦略

- サステナビリティへの取り組み

- DX (デジタルトランスフォーメーション) の取り組み

- 新興/スタートアップ競合の動向

第5章 市場の推定・予測:IDの種類別(2022~2035年)

- 生体認証

- 非生体認証

第6章 市場の推定・予測:コンポーネント別(2022~2035年)

- ソリューション/プラットフォーム

- 分散型IDプラットフォーム

- IDウォレット

- 検証可能な認証情報管理システム

- ブロックチェーン式IDネットワーク

- サービス

- コンサルティング・導入支援

- インテグレーション・相互運用性サービス

- マネージドサービス

- IDガバナンスサービス

第7章 市場の推定・予測:展開方式別(2022~2035年)

- オンプレミス

- クラウドベース

- ハイブリッド

第8章 市場の推定・予測:認証方法別(2022~2035年)

- 単一要素認証

- 多要素認証

第9章 市場の推定・予測:企業規模別(2022~2035年)

- 大企業

- 中小企業

第10章 市場の推定・予測:業種別(2022~2035年)

- BFSI

- 小売業・eコマース

- IT・通信

- 政府・公共部門

- 医療

- 不動産

- メディア・エンターテインメント

- その他

第11章 市場の推定・予測:地域別(2022~2035年)

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- 世界の主要企業

- Accenture

- Microsoft

- IBM

- Gen Digital Inc.

- Ping Identity

- 地域別主要企業

- 北米

- 1Kosmos Inc.

- Evernym Inc.

- Civic Technologies, Inc.

- Kiva Microfunds, Inc.

- 欧州

- Datarella GmbH

- Validated ID, SL

- Nuggets

- アジア太平洋

- Finema Co., Ltd.

- Ontology

- Persistent Systems

- Wipro DICE ID

- 北米

- ニッチ/ディスラプター企業

- Affinidi

- Alchemy Insights, Inc.

- Dragonchain Inc.