|

|

市場調査レポート

商品コード

1859010

物流ロボットの市場機会と促進要因、業界動向分析、2025年~2034年予測Logistics Robots Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 物流ロボットの市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年10月01日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

概要

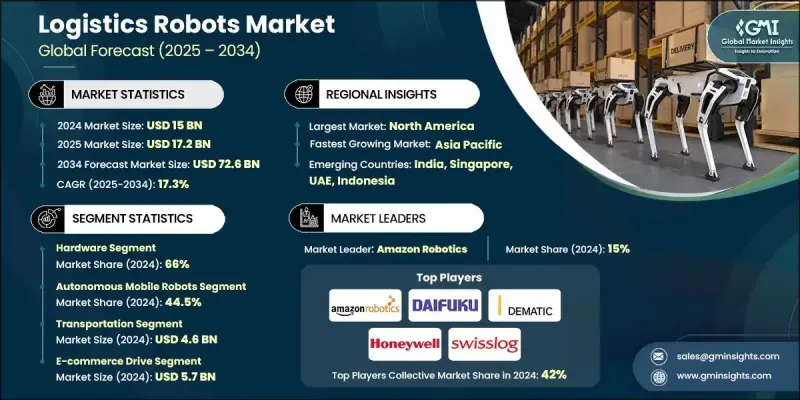

物流ロボットの世界市場規模は、2024年に150億米ドルとなり、CAGR 17.3%で成長し、2034年には726億米ドルに達すると予測されています。

この分野は、自動化への需要の高まり、納期の厳格化、サプライチェーンの高度なデジタル化によって形成され、急速に進化しています。この業界は、地理的な集積、戦略的サプライヤーとの関係、強力な垂直統合を特徴とする複雑なエコシステムによって定義されています。ロボット技術が成熟するにつれ、ロジスティクス企業は消費者の期待の高まりに応え、オペレーションの非効率性を削減するため、自律型システムへの移行を加速させています。ROIの加速化と投資回収期間の短縮が、倉庫や配送センターへのインテリジェント・ロボット・システムの幅広い導入を促しています。この自動化の波は、より高いスループット、精度の向上、労働力のスリム化を可能にすることで、ロジスティクス・インフラを再構築し、最終的に先進国市場と新興国市場の成長を促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 150億米ドル |

| 予測金額 | 726億米ドル |

| CAGR | 17.3% |

2024年、ハードウェア分野のシェアは66%を占め、2034年までのCAGRは16.4%と予想されます。ロボットプラットフォーム、機械部品、移動システムは、物流ロボットソリューションの基礎レイヤーを形成し、倉庫やラストマイル環境でのシームレスな運用を可能にします。ロボット動力システムに関する技術の進歩と研究イニシアチブは、ハードウェアのコスト構造を再構築しているが、物流業務における人間の関与は依然として総費用の大部分を占めています。

自律移動ロボット(AMR)セグメントは2024年に44.5%のシェアを占め、2025年から2034年にかけてCAGR 17.9%で成長すると予測されています。AMRは、人工知能、視覚SLAM、適応センサー技術による高度なナビゲーションシステムにより、従来の自動誘導車よりも大幅な効率向上を実現します。これらの機能は、複雑で動的な環境におけるリアルタイムの意思決定を可能にし、この分野をパイロット段階から大規模な商業展開へと移行させる。

米国は2024年に65%のシェアを占め、46億米ドルを創出。世界のベンチマークと比較すると普及率は比較的低いが、米国の成長は労働力不足、技術的準備、自動化に対する連邦政府の支援によって支えられています。強固なインフラと政府出資のイノベーション・プログラムは、世界のロボット事情における同国の地位を引き続き強化し、物流におけるロボットソリューションの大規模導入に有利な環境を作り出しています。

世界物流ロボット市場の競合情勢を形成している主な業界プレイヤーは、ABB、安川電機、トヨタ/バスティアン、オムロン、ダイフク、Amazon Robotics、KUKA/Swisslog、KION/Dematic、Honeywell、AutoStoreなどです。その地位を強化するため、物流ロボット企業はAIを活用した自動化、リアルタイムのデータ分析、様々な物流のユースケースに合わせたモジュラーシステム設計を優先しています。戦略的な合併やパートナーシップは、技術の共有と地理的な拡大を可能にし、研究開発投資は、マルチアプリケーション機能のためのスケーラブルなプラットフォームを生み出しています。大手企業はまた、eコマース、サードパーティロジスティクス、小売倉庫の環境に合わせてロボットフリートもカスタマイズしており、長期的な顧客維持と運用ROIの向上を実現しています。グローバル・プレーヤーは、現地生産、サービス・ネットワークの拡大、シームレスなロジスティクス・オーケストレーションと予知保全を可能にする統合デジタル・プラットフォームを通じて、その存在感をさらに高めています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 自律移動ロボットメーカー

- 自動保管・検索システムプロバイダー

- ロボティクス・ソフトウェア&AIプラットフォーム開発者

- 倉庫インフラ&マテリアルハンドリング機器サプライヤー

- システムインテグレーター&ソリューションプロバイダー

- コスト構造

- 利益率

- 各段階における付加価値

- サプライチェーンに影響を与える要因

- ディスラプター

- サプライヤーの情勢

- 影響要因

- 促進要因

- ピッキング用途におけるeコマース分野の発展

- ロボット技術の進歩

- 普及が進む自律型倉庫

- 物流における持続可能性への意識の高まり

- 業界の潜在的リスク&課題

- 購入・導入コストの高さ物流ロボット

- 高度なロボットシステムを運用・保守する従業員のスキル不足

- 市場機会

- 物流ロボットにおけるAIとIoTの融合物流ロボット

- 協働ロボットの導入

- 促進要因

- 技術動向とイノベーション・エコシステム

- 現在のテクノロジー

- コンピュータビジョンと物体認識

- 予測分析とメンテナンス

- 多機能ロボット開発

- 人間とロボットの協働の進展

- 新たなテクノロジー

- 5Gコネクティビティ&通信システム

- デジタルツイン&シミュレーション技術

- ブロックチェーンとサプライチェーンの透明性

- サステナビリティとグリーンテクノロジーの統合

- 現在のテクノロジー

- 成長可能性分析

- 規制情勢

- 連邦安全基準の枠組み

- ANSI/RIA R15.06要求事項

- ANSI R15.08移動ロボット規格

- ISO 10218グローバルハーモナイゼーション

- OSHAコンプライアンス要件

- 一般義務条項の適用

- 機械・機械警備基準

- 電気安全要件

- 業界特有の規制要件

- FDAヘルスケア規制

- 食品安全とHACCPコンプライアンス

- 自動車業界標準

- 国際標準の調和

- ISO技術委員会299

- 欧州規格の統合

- 地域適応要件

- 連邦安全基準の枠組み

- コスト内訳分析

- ハードウェアコスト構成要素

- ソフトウェア&インテグレーション費用

- インフラ改造要件

- メンテナンス&サービスコスト

- ポーター分析

- PESTEL分析

- 持続可能性と環境側面

- 環境影響評価とライフサイクル分析

- 社会的影響と地域社会との関係

- ガバナンスと企業責任

- 持続可能な技術開発

- リスク評価フレームワーク

- 相互運用性と標準化のギャップ

- レガシーシステム互換性の課題

- 規制・コンプライアンスリスク

- 財務リスク軽減戦略

- 性能・品質基準

- リスク評価手法

- 精度基準

- 業界特有の品質要件

- 安全試験要件

- 使用事例

- アマゾンのロボット導入モデル

- マルチSKUハンドリング&ソーティング

- 自動車製造の統合

- ヘルスケア&製薬アプリケーション

- サードパーティー・ロジスティクスの最適化

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- パートナーシップとコラボレーション

- 新製品発表

- 拡張計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ハードウェア

- ロボットプラットフォーム&シャーシ

- センサー&知覚システム

- アクチュエータとマニピュレーションシステム

- その他

- ソフトウェア

- ロボットオペレーティングシステム

- フリート管理ソフトウェア

- 倉庫管理統合

- その他

- サービス

- プロフェッショナル

- マネージド

第6章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- 無人搬送車

- 自律移動ロボット

- ロボットアーム

- その他

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- パレタイジング&デパレタイジング

- ピック&プレース

- 交通機関

- その他

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- eコマース

- ヘルスケア

- 小売り

- 飲食品

- 自動車

- その他

第9章 市場推計・予測:地域別、2021-2034

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベルギー

- オランダ

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- シンガポール

- 韓国

- ベトナム

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- グローバルプレーヤー

- ABB

- Amazon Robotics

- AutoStore

- Daifuku

- Honeywell

- KION/Dematic

- KUKA/Swisslog

- Omron

- Toyota/Bastian

- Yaskawa Electric

- 地域プレーヤー

- Bastian Solutions

- Geek+

- GreyOrange

- Locus Robotics

- Vecna Robotics

- 新興プレーヤー

- VisionNav Robotics

- Berkshire Grey

- Covariant

- Exotec

- River Systems