|

|

市場調査レポート

商品コード

1535932

宇宙旅行の市場規模:高度別、エンドユーザー別、予測、2024年~2032年Space Tourism Market Size - By Altitude (Orbital, Sub-orbital), By End User (Government, Commercial) & Forecast, 2024 - 2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 宇宙旅行の市場規模:高度別、エンドユーザー別、予測、2024年~2032年 |

|

出版日: 2024年06月26日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

宇宙旅行の市場規模は、宇宙旅行技術の急速な進歩と非公開会社の関与の増加により、2024年から2032年にかけてCAGR36.5%以上で成長すると予想されています。

宇宙機関や民間企業が再利用可能なロケットシステムや宇宙船の開発で大きく前進しているため、宇宙旅行のコストは徐々に低下し、より多くの人々が宇宙旅行を利用しやすくなっています。スペースX、ブルーオリジン、ヴァージン・ギャラクティックといった企業の市場参入も競争と投資に拍車をかけ、宇宙旅行インフラとサービスの開拓をさらに加速させています。例えば、2024年6月、ヴァージン・ギャラクティック社は有料の乗客を宇宙の果てまで送り届けることを決定し、宇宙産業が拡大・多様化し続ける中で重要なマイルストーンとなった。

宇宙旅行が現実のものとなるにつれ、無重力を体験し、宇宙から地球を眺めることの魅力に駆られ、地球外への探検を熱望する人々にとって魅力的なものとなっています。初期の宇宙観光ミッションのマーケティング努力とメディア報道は、興奮と一般大衆の関心を喚起し、市場成長にさらに拍車をかけています。

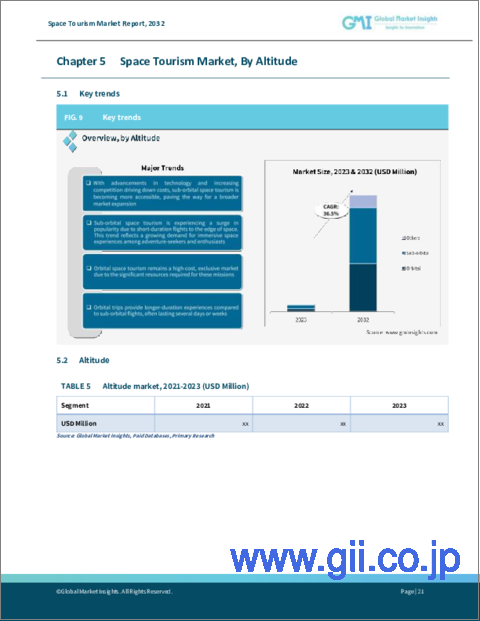

高度別に見ると、軌道セグメントによる宇宙旅行市場は、サブオービタル飛行に比べて没入感があり、格調高い体験ができることを背景に、2024年から2032年にかけて成長する見通しです。オービタル宇宙観光は、乗客に長時間の無重力状態と宇宙からの息を呑むような眺めを提供するために、宇宙への旅行と地球の周回を含みます。

エンドユーザー別に見ると、政府部門の宇宙旅行市場規模は2024年から2032年にかけて大幅なCAGRを記録すると見られています。これは、官民パートナーシップを促進し、宇宙技術の研究開発活動を支援するために、宇宙インフラへの多額の投資が行われていることが背景にあります。各国政府も商業宇宙ベンチャーの成長を促進するために資金援助や規制の枠組みを提供しており、宇宙観光企業にとってより有利な環境を作り出しています。

アジア太平洋の宇宙旅行産業は、2024年から2032年にかけて顕著な拡大を遂げると予想されています。これは、急速な経済成長と豊かさの増加により、贅沢で体験的な旅行を求める消費者層が拡大したためです。所得の増加がユニークな体験に対する需要を生み出しているため、この地域の富裕層は宇宙旅行への関心を高めています。政府と民間企業の双方による宇宙技術への多額の投資は、宇宙旅行インフラの進歩とアクセスコストの削減につながり、この地域の市場成長を刺激すると思われます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 宇宙船メーカー

- 打上げサービスプロバイダー

- 技術プロバイダー

- エンドユーザー

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- 航空宇宙の技術革新と効率化における技術の進歩

- ユニークな体験を求める富裕層からの需要の高まり

- 政府の支援政策とパートナーシップ

- 競争とイノベーションを促進する民間セクターの投資

- 業界の潜在的リスク&課題

- 高コストがアクセスの普及を阻害

- 宇宙観光事業のインフラが限定的

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:高度別、2021年~2032年

- 主要動向

- 軌道

- 準軌道

- その他

第6章 市場推計・予測:エンドユーザー別、2021年~2032年

- 主要動向

- 政府機関

- 軌道

- 準軌道

- その他

- 商業

- 軌道

- 準軌道

- その他

- その他

- 軌道

- 準軌道

- その他

第7章 市場推計・予測:地域別、2021年~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- シンガポール

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

- その他の中東・アフリカ

第8章 企業プロファイル

- Airbus

- Astroscale Holdings Inc.

- Axiom Space, Inc.

- Bigelow Aerospace

- Blue Origin Enterprises, L.P.

- Elysium Space

- Excalibur Almaz

- Isar Aerospace

- Orion Span

- Rocket Lab USA, Inc.

- Space Adventures, Inc.

- Space Island Group

- Space Perspective

- SpaceX

- The Boeing Company

- Virgin Galactic Holdings, Inc.

- World View Enterprises, Inc.

- Zero 2 Infinity

- Zero Gravity Corporation

Space tourism market size is anticipated to grow at over 36.5% CAGR between 2024 and 2032 driven by rapid advancements in space travel technology and the increasing involvement of private companies.

With space agencies and private enterprises making significant strides in developing reusable rocket systems and spacecraft, the cost of space travel is gradually decreasing, making it more accessible to a broader audience. The entry of companies like SpaceX, Blue Origin, and Virgin Galactic into the market has also spurred competition and investments, further accelerating the development of space tourism infrastructure and services. For instance, in June 2024, Virgin Galactic selected paying passengers to the edge of space, marking a significant milestone as the space industry continues to expand and diversify.

As space tourism has become a reality, it is appealing to those eager to explore beyond Earth, driven by the allure of experiencing weightlessness and viewing Earth from space. Marketing efforts and media coverage of early space tourism missions for generating excitement and public interest is further adding to the market growth.

The overall industry is segmented into altitude, end user, and region.

Based on altitude, the space tourism market from the orbital segment is poised to grow between 2024 and 2032 backed by its immersive and prestigious experience compared to suborbital flights. Orbital space tourism involves traveling to space and orbiting Earth for providing passengers with extended periods of weightlessness and breathtaking views from space.

Based on end user, the space tourism market size from the government segment is set to witness significant CAGR from 2024 to 2032. This is driven by the hefty investments in space infrastructure for fostering public-private partnerships and supporting R&D activities in space technologies. Governments are also providing funding and regulatory frameworks to facilitate the growth of commercial space ventures, creating a more favorable environment for space tourism companies.

Asia Pacific space tourism industry is expected to accrue notable expansion from 2024 to 2032. This is attributed to rapid economic growth and increasing affluence, which have expanded the consumer base for luxury and experiential travel. As rising incomes are creating the demand for unique experiences, affluent individuals in the region are increasingly interested in space tourism. The significant investments in space technology from both governments and private enterprises, leading to advancements in space travel infrastructure and reducing the cost of access will stimulate the regional market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

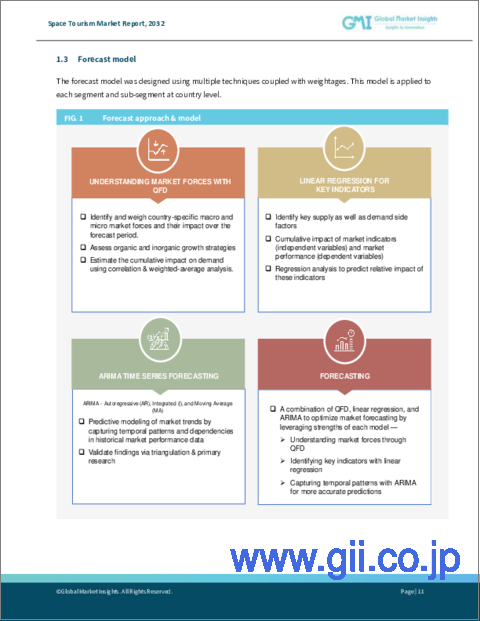

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Spacecraft manufacturers

- 3.2.2 Launch service providers

- 3.2.3 Technology provider

- 3.2.4 End user

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Technological advancements in aerospace innovation and efficiency

- 3.8.1.2 Rising demand from affluent individuals seeking unique experiences

- 3.8.1.3 Supportive government policies and partnerships

- 3.8.1.4 Private sector investments fostering competition and innovation

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High costs inhibit widespread accessibility

- 3.8.2.2 Limited infrastructure for space tourism operations

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.10.1 Supplier power

- 3.10.2 Buyer power

- 3.10.3 Threat of new entrants

- 3.10.4 Threat of substitutes

- 3.10.5 Industry rivalry

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Altitude 2021 - 2032 ($Mn, Number of Visitors)

- 5.1 Key trends

- 5.2 Orbital

- 5.3 Sub-orbital

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By End User, 2021 - 2032 ($Mn, Number of Visitors)

- 6.1 Key trends

- 6.2 Government

- 6.2.1 Orbital

- 6.2.2 Sub-orbital

- 6.2.3 Others

- 6.3 Commercial

- 6.3.1 Orbital

- 6.3.2 Sub-orbital

- 6.3.3 Others

- 6.4 Others

- 6.4.1 Orbital

- 6.4.2 Sub-orbital

- 6.4.3 Others

Chapter 7 Market Estimates & Forecast, By Region, 2021 - 2032 ($Mn, Number of Visitors)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Russia

- 7.3.7 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.4.6 Singapore

- 7.4.7 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 MEA

- 7.6.1 UAE

- 7.6.2 South Africa

- 7.6.3 Saudi Arabia

- 7.6.4 Rest of MEA

Chapter 8 Company Profiles

- 8.1 Airbus

- 8.2 Astroscale Holdings Inc.

- 8.3 Axiom Space, Inc.

- 8.4 Bigelow Aerospace

- 8.5 Blue Origin Enterprises, L.P.

- 8.6 Elysium Space

- 8.7 Excalibur Almaz

- 8.8 Isar Aerospace

- 8.9 Orion Span

- 8.10 Rocket Lab USA, Inc.

- 8.11 Space Adventures, Inc.

- 8.12 Space Island Group

- 8.13 Space Perspective

- 8.14 SpaceX

- 8.15 The Boeing Company

- 8.16 Virgin Galactic Holdings, Inc.

- 8.17 World View Enterprises, Inc.

- 8.18 Zero 2 Infinity

- 8.19 Zero Gravity Corporation