|

市場調査レポート

商品コード

1833642

データセンターサービスの市場機会、成長促進要因、業界動向分析、2025年~2034年予測Data Center Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| データセンターサービスの市場機会、成長促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年09月05日

発行: Global Market Insights Inc.

ページ情報: 英文 230 Pages

納期: 2~3営業日

|

概要

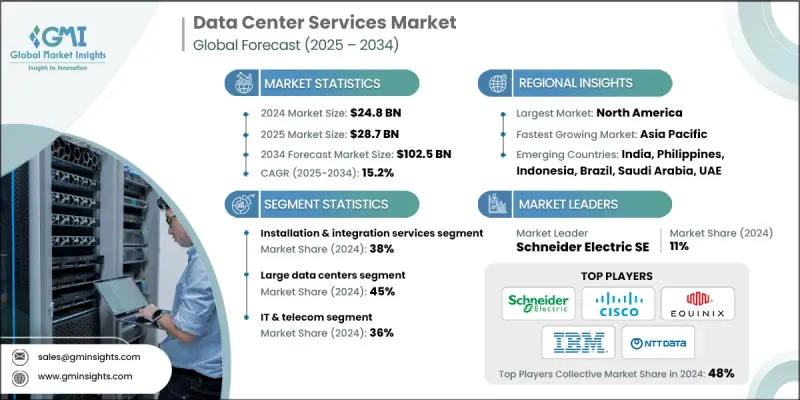

データセンターサービスの世界市場は、2024年に248億米ドルと推定され、CAGR 15.2%で成長し、2034年には1,025億米ドルに達すると推定されます。

成長を牽引しているのは、クラウドコンピューティングとデータストレージソリューションに対する需要の高まりです。さまざまな分野の企業が拡張性、俊敏性、コスト削減を実現するためにクラウドベースのプラットフォームへの移行を進めるなか、信頼性が高く、パフォーマンスの高いデータセンターへの需要が高まり続けています。これらの施設はクラウドサービスプロバイダーの基盤を形成し、拡張性と耐障害性に優れたデジタルソリューションを顧客に提供することを可能にしています。規制の枠組みが強化され、サイバー脅威やデータ漏洩に対する意識が高まっていることを受け、企業は堅牢なセキュリティ・プロトコル、ビルトイン冗長性、業界標準への完全準拠を組み込んだデータセンターを優先するようになっています。さらに、事業継続性、災害復旧、運用回復力への注目の高まりにより、最大限の稼働時間、強力なフェイルオーバー機能、安全なバックアップインフラを確保するデータセンターサービスへのニーズが加速しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 248億米ドル |

| 予測金額 | 1,025億米ドル |

| CAGR | 15.2% |

設置・統合サービス分野は2024年に38%のシェアを占め、2034年までのCAGRは15%と予測されます。このセグメントは、ハイパースケールインフラ、コロケーションサイト、エンタープライズグレードのITフレームワークの展開に不可欠です。これらのサービスは、既存システムとの互換性を確保しながら、サーバー、電源システム、冷却機構、ネットワーク機器のシームレスな展開を可能にします。こうしたサービスの重要性が高まっている背景には、ハイブリッド・クラウド環境、AI主導型コンピューティング、高密度ワークロードの採用が増加していることがあり、こうした環境では正確な構成と高度な統合技術が要求されます。

2024年、大規模データセンター・セグメントは45%のシェアを占め、2025年から2034年にかけて15.3%のCAGRで成長すると予測されています。これらの施設は、ハイパースケールやコロケーション展開の要として機能し、比類のない容量、次世代冷却ソリューション、高度な相互接続性を提供します。これらのインフラは、AI、エンタープライズ・ワークロード、クラウドネイティブ・アプリケーションに効率性と柔軟性をもって対応できるよう設計されています。マルチテナントの要件を満たす拡張性の高い高性能インフラに対する需要の高まりは、グローバルなデジタルトランスフォーメーション戦略における大規模データセンターの重要性を高めています。

米国データセンターサービス産業は85%のシェアを占め、2024年には77億米ドルを生み出しました。このリーダーシップは、ハイパースケールクラウド事業者の広範な存在、堅牢なデジタルインフラ、企業全体でのハイブリッドITシステムの広範な採用によってもたらされます。人工知能、エッジコンピューティング、デジタルツインテクノロジーの革新は、ビジネスの運営方法を再構築し、高度なデータセンターの新たなユースケースを生み出しています。5Gネットワークの拡大、クラウドプラットフォームへの移行の加速、サイバーセキュリティに対する要求の高まりはすべて、安全で拡張性が高く、パフォーマンスが最適化されたデータセンター環境への投資を企業に促しています。

データセンターサービス業界で事業を展開する主要企業には、シュナイダーエレクトリック、イートン、NTTデータ、デジタルリアルティ、IBM、シスコシステムズ、デル、エクイニクス、シーメンス、ABBなどがあります。データセンターサービス市場の主要プレーヤーは、持続可能性、デジタルオートメーション、戦略的グローバル展開を取り入れ、市場での存在感を高めています。企業は、環境規制を満たし、運用コストを削減するために、エネルギー効率の高いモジュール式施設を建設しています。AIを活用したモニタリング、遠隔管理、予知保全の統合により、性能と稼働率が向上しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- グローバル

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- クラウドコンピューティングソリューションの採用拡大

- データストレージと処理能力に対する需要の増加

- 企業全体でデジタル変革の取り組みが増加

- エッジデータセンターの導入拡大

- 業界の潜在的リスク&課題

- 初期設定コストが高め

- セキュリティとコンプライアンスに関する懸念

- 市場機会

- 環境に優しく持続可能なデータセンターへの注目が高まる

- データセンター運用におけるAIと自動化の統合の拡大

- 5GとIoT主導のインフラの導入増加

- 新興国における機会の拡大

- 促進要因

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 成長可能性分析

- コスト内訳分析

- ポーター分析

- PESTEL分析

- 特許分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 技術革新とインフラの進化

- 次世代冷却技術

- 電力インフラとエネルギー管理

- モジュール式およびプレハブ式ソリューション

- ソフトウェア定義のインフラストラクチャと自動化

- サイバーセキュリティとゼロトラストアーキテクチャ

- データセンターのセキュリティ脅威の情勢

- データセンターにおけるゼロトラストの実装

- コンプライアンスと監査の枠組み

- コスト最適化と財務インテリジェンス

- 総所有コスト(TCO)分析

- 電力コストインテリジェンスと最適化

- 不動産と敷地選定の経済学

- 財務モデルと価格戦略

- サプライチェーンのリスク管理とレジリエンス

- グローバルサプライチェーンの脆弱性評価

- サプライチェーン多様化戦略

- ベンダー関係管理

- 人材開発とスキルギャップ分析

- スキル不足の危機と影響評価

- 人材開発戦略

- 自動化と人間とAIのコラボレーション

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:サービス別2021-2032

- 主要動向

- インストールおよび統合サービス

- トレーニングサービス

- コンサルティングサービス

- メンテナンスとサポート

- その他

第6章 市場推計・予測:データセンター規模別、2021-2032

- 主要動向

- 小規模データセンター

- 中規模データセンター

- 大規模データセンター

第7章 市場推計・予測:用途別、2021-2032

- 主要動向

- BFSI

- コロケーション

- エネルギー

- 政府

- ヘルスケア

- 製造業

- ITおよび通信

- その他

第8章 市場推計・予測:展開モード別、2021-2034

- 主要動向

- オンプレミス

- クラウド

- ハイブリッド

第9章 市場推計・予測:ティア別、2021-2034

- 主要動向

- ティア1

- ティア2

- ティア3

- ティア4

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- フィリピン

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- グローバルプレーヤー

- ABB

- Amazon Web Services

- Cisco Systems

- Dell

- DXC

- Equinix

- Eaton

- Fujitsu

- HCL

- Hewlett-Packard Enterprise(HPE)

- Hitachi

- Huawei Technologies

- IBM

- Microsoft

- NTT

- Schneider Electric

- Siemens

- Vertiv

- 地域プレーヤー

- AirTrunk

- AtlasEdge

- CoreSite Realty

- Iron Mountain Data Centers

- Keppel Data Centre

- NEXTDC

- Switch

- 新興プレーヤー

- Applied Digital

- CoreWeave

- Crusoe Energy Systems

- Vapor IO