|

市場調査レポート

商品コード

1913441

酢酸ビニルモノマーの市場機会、成長要因、業界動向分析、および2026年から2035年までの予測Vinyl Acetate Monomer (VAM) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 酢酸ビニルモノマーの市場機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月16日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

概要

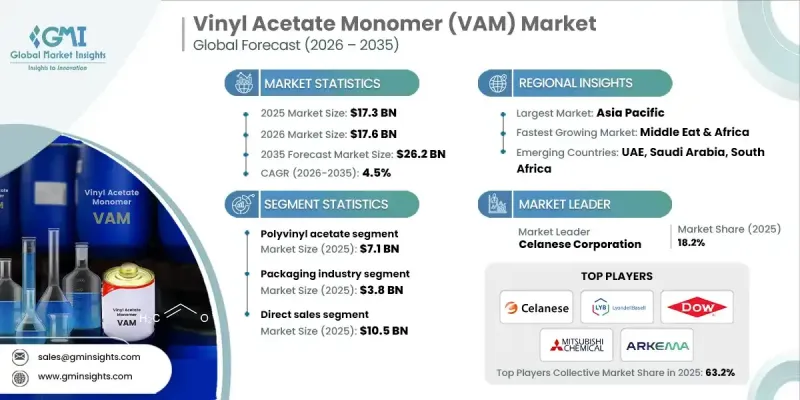

世界の酢酸ビニルモノマー(VAM)市場は、2025年に173億米ドルと評価され、2035年までにCAGR4.5%で成長し、262億米ドルに達すると予測されています。

本市場の成長は、高性能で持続可能な包装ソリューションへの需要増加と、ポリ酢酸ビニル、エチレン酢酸ビニル、ポリビニルアルコールなどのVAM由来ポリマーの用途拡大に牽引されています。これらのポリマーは、優れた接着性、防水性、汎用性から包装フィルムやフレキシブルラミネートに好んで使用されています。さらに、消費財や産業用包装の消費増加、建設・自動車・工業用塗料分野での成長が需要を後押ししています。都市化の進展、インフラ整備、改修活動の増加に伴い、VAM樹脂を基にした接着剤、シーラント、コーティング剤、複合材料の使用が増加しています。低VOCおよび水性配合を促進する環境規制により、従来の溶剤系材料から一部の用途が移行しつつあります。先進的な生産技術と最適化された製造プロセスは、効率性を高め、供給の信頼性を確保し、世界市場における競争力を強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 173億米ドル |

| 予測金額 | 262億米ドル |

| CAGR | 4.5% |

ポリ酢酸ビニル(VAM)セグメントは、接着剤、塗料、コーティング、建設資材における幅広い用途に支えられ、2025年に71億米ドルの市場規模を達成しました。優れた接着性、調合の容易さ、水性用途との相性の良さから、包装、木工、紙製品用途における主要な原料となっています。環境に優しく低揮発性有機化合物(VOC)の接着剤への需要の高まりが、世界のVAM市場におけるその重要性をさらに強化し続けています。

包装業界は2025年に38億米ドルに達し、VAMの消費量で最大の割合を占めました。VAM由来のPVA、PVB、EVOHなどのポリマーは、湿気や酸素を遮断する包装に不可欠な優れた接着性、透明性、バリア性を提供します。電子商取引の成長、FMCG流通ネットワークの拡大、軽量でリサイクル可能な包装材料への移行が、このセグメントの需要を牽引しています。

北米の酢酸ビニルモノマー(VAM)市場は2025年に45億米ドル規模に達しました。同地域は統合された石油化学インフラ、エチレンや酢酸などの原料の豊富な供給、接着剤・水性塗料・包装フィルム・建設用ポリマーといった成熟した下流市場を有するため、26%のシェアを占めています。この強固な産業基盤が、VAMの安定した大量消費と市場成長を保証しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 水性接着剤および塗料に対する需要の増加

- 包装産業の拡大

- 溶剤系から水性系への移行

- 業界の潜在的リスク&課題

- 原材料価格の変動性

- 厳格な揮発性有機化合物(VOC)排出規制

- 市場機会

- 食品包装用高バリアEVOHフィルム

- 医薬品送達システム向け医療用グレードEVA

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 用途別

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許状況

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測用途別、2022-2035

- ポリ酢酸ビニル

- ポリビニルアルコール

- ポリビニルブチラール

- エチレンビニルアルコール

- 塩化ビニルー酢酸ビニル共重合体

- ポリビニルホルマール

- その他

第6章 市場推計・予測:最終用途産業別、2022-2035

- ポリ酢酸ビニル(PVAc)

- エマルジョンポリマー

- 接着剤

- 塗料・バインダー

- エチレン酢酸ビニル共重合体(EVA)

- フィルム

- 発泡体

- ホットメルト接着剤

- 太陽電池封止材

- ポリビニルアルコール(PVOH)

- 繊維

- 紙用コーティング剤

- 塗料・ペイント

- 建築用塗料

- 工業用塗料

- 繊維用化学品

- サイジング剤

- 仕上げ剤

- 紙用化学品

- 紙用バインダー

- ラミネート

- その他

第7章 市場推計・予測:流通チャネル別、2022-2035

- 直接販売

- 販売代理店

- 商社

- オンライン販売

第8章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- Celanese Corporation

- LyondellBasell Industries

- Dow

- Mitsubishi Chemical Corporation

- Arkema

- Wacker Chemie AG

- Henan GP Chemicals Co., Ltd.

- Suneco Chem

- Meru Chem Pvt.Ltd.

- Tiankai Chemical

- Gantrade Corporation

- Opes International

- Jubilant Ingrevia

- Vinipul Chemicals