|

|

市場調査レポート

商品コード

1532644

肝臓がん治療薬の世界市場規模:タイプ別、薬剤クラス別、投与経路別、投薬タイプ別、ジェンダー別 - 予測(2024年~2032年)Liver Cancer Drugs Market Size - By Type (HCC, Cholangiocarcinoma, Hepatoblastoma), Drug Class (Chemotherapeutics, Targeted & Immunotherapy), Route of Administration (Oral, Injectable), Medication Type (Branded, Generics), Gender & Forecast, 2024 - 2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 肝臓がん治療薬の世界市場規模:タイプ別、薬剤クラス別、投与経路別、投薬タイプ別、ジェンダー別 - 予測(2024年~2032年) |

|

出版日: 2024年05月30日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

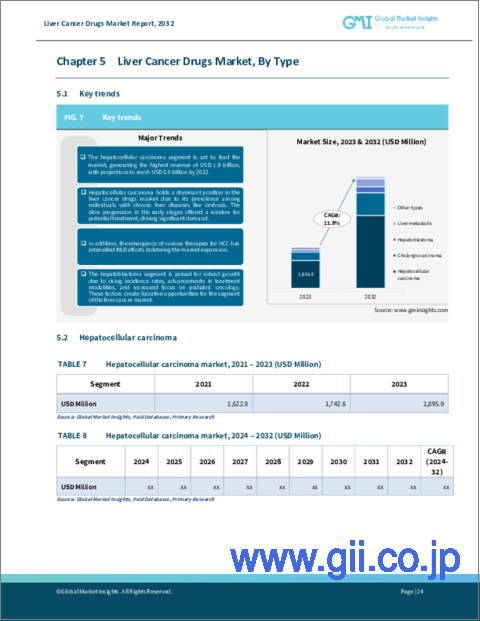

WHOによると、過去20年間に発生率が75%増加したという肝臓がんの世界の有病率の上昇に牽引され、世界の肝臓がん治療薬の市場規模は、2024年~2032年に11.8%のCAGRを記録すると推定されています。

この増加の主な原因は、人口の高齢化、アルコール消費の増加、B型肝炎とC型肝炎の蔓延であり、これらの感染者は世界で3億2,500万人を超えている、とCDCの報告書は述べています。さらに、生活習慣、特に肥満と糖尿病が肝臓がんの発生率をさらに高めています。その結果、より効果的な治療に対するニーズが高まり、先進的な肝臓がん治療薬の技術革新と商業化に拍車がかかっています。

標的療法や免疫療法の登場は、肝臓がん治療の展望を大きく変えつつあります。例えば、米国国立がん研究所によれば、ソラフェニブやニボルマブのような薬剤は臨床試験で顕著な効果を示しています。さらに、製薬企業による研究開発投資の増大と政府の後押しが、創薬と承認のタイムラインを早めています。このような進展は、治療スペクトルを広げるだけでなく、肝臓がん治療薬の安全性と有効性のベンチマークを高め、市場拡大をさらに後押ししています。

世界の肝臓がん治療薬産業は、タイプ、薬剤クラス別、投与経路、投薬タイプ、ジェンダー別、地域に基づいて分類されます。

肝芽腫タイプは、特に小児患者における罹患率の増加により、2032年まで大きく成長する見込みです。小児に最も多い肝臓がんである肝芽腫では、成人の肝臓がんとは異なる特殊な治療法が必要となります。肝芽腫の認知度と早期診断が向上するにつれて、この患者集団に合わせた的を絞った効果的な治療法に対する需要が高まっています。製薬会社は、肝芽腫に特化した革新的な薬剤や治療プロトコルの開発にますます注力しています。このことは、肝芽腫の理解と克服を目指した研究努力と臨床試験の強化とともに、このセグメントのシェアに有利に働くと思われます。

経口肝臓がん治療薬産業セグメントは、利便性と有効性により、予測期間中に大きな牽引力を得ると思われます。経口薬は点滴治療に代わる非侵襲的な治療法であり、患者が自宅で服用できるため、コンプライアンスの向上とヘルスケアコストの削減につながります。製薬技術の進歩により、より優れたバイオアベイラビリティと標的作用を持つ非常に効果的な経口薬が製造され、副作用を最小限に抑え、治療成績を向上させています。さらに、経口製剤の利便性は、その有効性と安全性を裏付ける強力な臨床エビデンスと相まって、患者と医療従事者の双方にとって好ましい選択肢となっています。

アジア太平洋の肝臓がん治療薬市場は、特にB型肝炎とC型肝炎の蔓延、飲酒率と肥満率の上昇に起因する肝臓がんの高い有病率を背景に、2032年まで力強い成長動向を示すと思われます。さらに、中国やインドなどではヘルスケア支出が増加し、医療インフラが整備されたことで、先進治療へのアクセスが向上しています。がん治療と研究の強化を目的とした政府の取り組みや支援政策も、市場の成長に寄与しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 業界の潜在的リスクと課題

- 成長可能性分析

- パイプライン分析

- 規制状況

- 今後の市場動向

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場企業の競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別(2021年~2032年)

- 主要動向

- 肝細胞がん

- 胆管がん

- 肝芽腫

- 肝転移

- その他のタイプ

第6章 市場推計・予測:薬剤クラス別(2021年~2032年)

- 主要動向

- 化学療法剤

- 標的治療薬

- 免疫療法薬

第7章 市場推計・予測:投与経路別(2021年~2032年)

- 主要動向

- 経口

- 注射

第8章 市場推計・予測:投薬タイプ別(2021年~2032年)

- 主要動向

- ジェネリック

- ブランド

第9章 市場推計・予測:ジェンダー別(2021年~2032年)

- 主要動向

- 男性

- 女性

第10章 市場推計・予測:地域別(2021年~2032年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ

第11章 企業プロファイル

- AbbVie Inc.

- Amgen Inc.

- AstraZeneca Plc

- Bayer AG

- Bristol-Myers Squibb Company

- Eisai Co., Ltd.

- Exelixis, Inc.

- F. Hoffmann-La Roche Ltd.

- Johnson & Johnson

- Merck & Co., Inc.

- Novartis AG

- Sanofi SA

- Thermo Fisher Scientific Inc.

The liver cancer drugs market is estimated to register 11.8% CAGR during 2024 and 2032, driven by the escalating global prevalence of liver cancer, which has seen a 75% increase in incidence over the past two decades, according to WHO. This rise is primarily attributed to an aging population, heightened alcohol consumption, and the widespread incidence of hepatitis B and C, which affect over 325 million people worldwide, cites CDC report. Moreover, lifestyle elements, notably obesity and diabetes, are further bolstering the incidence of liver cancer. Consequently, there's a mounting need for more effective treatments, spurring the innovation and commercialization of advanced liver cancer drugs.

The advent of targeted and immunotherapies is reshaping liver cancer treatment landscape. For instance, as per National Cancer Institute, drugs like Sorafenib and Nivolumab have shown significant efficacy in clinical trials. Moreover, amplified R&D investments from pharmaceutical entities, bolstered by government backing, are expediting drug discovery and approval timelines. These strides not only broaden the treatment spectrum but also elevate the safety and efficacy benchmarks of liver cancer drugs, further propelling market expansion.

The global liver cancer drugs industry is classified based on type, drug class, route of administration, medication type, gender, and region.

The hepatoblastoma type segment is poised to significantly growth through 2032, due to increasing incidence, particularly among pediatric patients. Hepatoblastoma, the most common liver cancer in children, necessitates specialized treatment options that differ from those used for adult liver cancers. As awareness and early diagnosis of hepatoblastoma improve, there is a growing demand for targeted and effective therapies tailored to this patient population. Pharmaceutical companies are increasingly focusing on developing innovative drugs and treatment protocols specifically for hepatoblastoma. This, along with enhanced research efforts and clinical trials aimed at understanding and combating hepatoblastoma will favor the segment share.

The oral liver cancer drugs industry segment will gain substantial traction over the forecast period, owing to convenience and effectiveness. Oral medications offer a non-invasive alternative to intravenous treatments, allowing patients to take them at home, which improves compliance and reduces healthcare costs. Advances in pharmaceutical technology have produced highly effective oral drugs with better bioavailability and targeted action, minimizing side effects and improving treatment outcomes. Additionally, the convenience of oral formulations, coupled with strong clinical evidence supporting their efficacy and safety, makes them a preferred choice for both patients and healthcare providers.

Asia Pacific liver cancer drugs market will exhibit strong growth trends through 2032, backed by a high prevalence of liver cancer, particularly due to widespread hepatitis B and C infections and rising rates of alcohol consumption and obesity. Additionally, increasing healthcare expenditure and improving medical infrastructure in countries such as China and India are facilitating better access to advanced treatments. Government initiatives and supportive policies aimed at enhancing cancer care and research are also contributing to market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising burden of liver cancer

- 3.2.1.2 Increasing R&D investments for the development of novel therapies

- 3.2.1.3 Rising aging population

- 3.2.1.4 Government initiatives to increase cancer awareness

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Side effects associated with certain medications

- 3.2.2.2 High cost of cancer therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pipeline analysis

- 3.5 Regulatory landscape

- 3.6 Future market trends

- 3.7 Porters analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2032 ($ Mn)

- 5.1 Key trends

- 5.2 Hepatocellular carcinoma

- 5.3 Cholangiocarcinoma

- 5.4 Hepatoblastoma

- 5.5 Liver metastasis

- 5.6 Other types

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 - 2032 ($ Mn)

- 6.1 Key trends

- 6.2 Chemotherapeutic agents

- 6.3 Targeted therapy drugs

- 6.4 Immunotherapy drugs

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2032 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

Chapter 8 Market Estimates and Forecast, By Medication Type, 2021 - 2032 ($ Mn)

- 8.1 Key trends

- 8.2 Generic

- 8.3 Branded

Chapter 9 Market Estimates and Forecast, By Gender, 2021 - 2032 ($ Mn)

- 9.1 Key trends

- 9.2 Male

- 9.3 Female

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2032 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.3.7 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 AbbVie Inc.

- 11.2 Amgen Inc.

- 11.3 AstraZeneca Plc

- 11.4 Bayer AG

- 11.5 Bristol-Myers Squibb Company

- 11.6 Eisai Co., Ltd.

- 11.7 Exelixis, Inc.

- 11.8 F. Hoffmann-La Roche Ltd.

- 11.9 Johnson & Johnson

- 11.10 Merck & Co., Inc.

- 11.11 Novartis AG

- 11.12 Sanofi SA

- 11.13 Thermo Fisher Scientific Inc.