|

市場調査レポート

商品コード

1982366

機能性印刷市場、成長機会、成長要因、業界動向分析、および2026年~2035年の予測Functional Printing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 機能性印刷市場、成長機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年02月24日

発行: Global Market Insights Inc.

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

概要

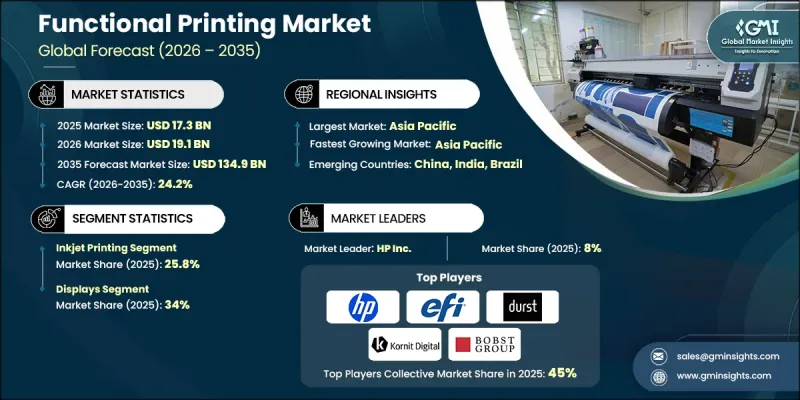

世界の機能性印刷市場は、2025年に173億米ドルと評価され、2035年までにCAGR24.2%で成長し、1,349億米ドルに達すると推定されています。

この市場は、先端材料、導電性インク、およびインクジェット、スクリーン、グラビア印刷などの次世代印刷技術における継続的なイノベーションによって牽引されています。機能性印刷は、高度なカスタマイズ性、廃棄物の削減、製品開発サイクルの短縮を可能にするため、高付加価値用途においてますます好まれるようになっています。リソグラフィーや標準的なPCB製造といった従来の減法製造手法から、積層造形やデジタル化された生産への移行は、製造哲学における大きなパラダイムシフトを表しています。合併、買収、技術提携を通じた戦略的な統合が市場の成長を加速させており、導電性インク、フレキシブル基板、および印刷センサー技術の主要企業が統合ソリューションを構築できるようになっています。業界が柔軟性、少量生産、多品種生産をますます求める中、機能性印刷は、エレクトロニクス、パッケージング、スマートデバイスなどの分野において、重要な推進力として台頭しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 173億米ドル |

| 予測額 | 1,349億米ドル |

| CAGR | 24.2% |

インクジェット印刷セグメントは25.8%のシェアを占め、2025年には44億米ドルの規模に達すると見込まれています。インクジェットは、プリンテッドエレクトロニクス、高解像度機能層、スマートパッケージングへの適応性により、市場をリードしています。ナノ粒子導電性インク、フレキシブル基板、低温焼結技術における急速な技術革新が、市場の成長を支えています。オンデマンド生産、多品種少量生産に適していることから、エレクトロニクス、テキスタイル、および先進パッケージング用途に最適です。

2025年には、ディスプレイ分野が34%のシェアを占め、フレキシブルディスプレイ、OLEDパネル、タッチインターフェース、およびプリントバックプレーンの採用拡大が牽引しました。ロールツーロール製造と透明導電性材料の使用が、さらなる成長を支えています。インクジェット、スクリーン、グラビアを含む機能性印刷技術により、フレキシブルで複雑なディスプレイ構造の製造が可能となり、携帯電子機器、エネルギーソリューション、および建築統合技術(BIT)の用途に貢献しています。

2025年、米国の機能性印刷市場は64.4%のシェアを占めました。プリンテッドエレクトロニクス、フレキシブルディスプレイ、デジタル化されたパッケージングの普及が市場の成長を後押ししています。スマートラベル、プリンテッドセンサー、RFID追跡、アディティブエレクトロニクスに対する需要の急増は、Eコマース、ヘルスケア、民生用電子機器などの分野によって牽引されています。フレキソとインクジェット技術を組み合わせたハイブリッド印刷プラットフォームの活用に加え、AIを活用した印刷最適化、インライン検査、予知保全により、産業用途全般におけるOEMやコンバーターの信頼性が強化されています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 深刻化する労働力不足と製造業のリショアリング

- AI、ジェネレーティブデザイン、およびソフトウェア統合

- 印刷業務におけるIT/OTの融合

- 業界の潜在的リスク&課題

- 高度な統合の複雑さ

- データプライバシーとサイバーセキュリティ

- 機会

- Printing-as-a-Service(PaaS)

- プリンテッドエレクトロニクスおよびスマートパッケージングの成長

- 促進要因

- 成長可能性分析

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 技術別

- 規制情勢

- 規格およびコンプライアンス要件

- 地域別規制の枠組み

- 認証基準

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:材料別、2022-2035

- 基板

- ガラス

- プラスチック

- 紙

- 炭化ケイ素

- 窒化ガリウム

- その他

- インク

- 導電性インク

- 誘電性インク

- グラフェンインク

- その他

第6章 市場推計・予測:技術別、2022-2035

- インクジェット印刷

- スクリーン印刷

- フレキソ印刷

- グラビア印刷

- その他

第7章 市場推計・予測:用途別、2022-2035

- ディスプレイ

- センサー

- 太陽光発電

- 照明

- バッテリー

- RFIDタグ

- その他

第8章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Bobst Group

- Comexi Group

- Domino

- Durst Group

- EFI

- HP Inc.

- Kornit Digital

- KYMC

- Mark Andy

- Mimaki Engineering

- PCMC

- Roland DG

- SPGPrints

- Thieme

- Uteco Converting