|

|

市場調査レポート

商品コード

1518477

患者ポジショニングシステム市場:製品、用途、最終用途別、2024年~2032年の予測Patient Positioning Systems Market - By Product (Tables [Surgical Tables, Radiolucent Imaging Tables, Examination Tables] Accessories), Application (Surgery, Diagnostics, Rehabilitation), End-use (Hospitals and Clinics, ASC) & Forecast, 2024 - 2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 患者ポジショニングシステム市場:製品、用途、最終用途別、2024年~2032年の予測 |

|

出版日: 2024年04月24日

発行: Global Market Insights Inc.

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

患者ポジショニングシステムの市場規模は、慢性疾患と外科手術の罹患率上昇に牽引され、2024~2032年にCAGR 3.6%を記録します。

WHOによると、非感染性疾患(NCDs)は年間4,100万人の死亡をもたらし、世界全体の死亡率の74%を占めています。心血管疾患、がん、整形外科疾患などの慢性疾患は、効果的な治療と正確な医療画像を確保するために、正確な患者の位置決めに依存する外科的介入や診断手順を必要とすることが多いです。患者ポジショニングシステムは、手術や診断検査中の患者のアライメントを安全かつ最適にし、手技の結果と患者の回復時間を向上させるという重要な役割を担っています。

ヘルスケア施設では、患者の快適性を高め、医療従事者の怪我のリスクを最小限に抑え、処置の効率を最適化するために、人間工学的な配慮が優先されています。医療従事者が患者の転帰と業務ワークフローの改善に努める中、人間工学に基づいた患者位置決めソリューションの需要は伸び続けており、市場拡大の原動力となっています。

患者ポジショニングシステム産業は、製品、用途、最終用途、地域によって分類されます。

アクセサリー分野は、患者をサポートし、臨床要件に応じた正確なポジショニングを容易にする設計により、2032年まで急速に成長します。ヘルスケア施設では患者の安全性と人間工学的な配慮が優先されるため、さまざまな医療専門分野に合わせた特殊なアクセサリーの需要が伸び続けています。ヘルスケアメーカーは、耐久性に優れ、洗浄が容易で、さまざまな患者ポジショニングシステムと互換性のあるアクセサリーの開発に注力しており、これにより多様な医療環境に対応し、患者ケアの全体的な成果を向上させています。

患者ポジショニングシステムは、正確な画像診断や診断処置に不可欠であるため、診断分野は予測期間中に大きな需要を生み出すと思われます。これらのシステムは、X線、CTスキャン、MRIスキャンなどの放射線検査における患者の正確な位置決めを容易にし、最適な画像品質と診断精度を保証します。高度な画像処理技術と人間工学に基づいたポジショニングソリューションの統合により、ヘルスケアプロバイダーは、患者の不快感や放射線被ばくを最小限に抑えながら、鮮明で詳細な診断画像を得ることができます。

欧州の患者ポジショニングシステム産業規模は、ヘルスケアインフラの進歩、医療支出の増加、高齢者人口の増加を背景に、2032年まで速いペースで拡大します。ドイツ、フランス、米国などはヘルスケアの革新と技術導入でリードしており、最先端の患者位置決めソリューションの需要を促進しています。規制の枠組みが厳しく、患者の安全性が重視されていることも、病院や診断センターでの人間工学に基づいた使いやすいポジショニングシステムの採用を後押ししています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患の増加

- ヘルスケア支出の増加

- 手術件数の増加

- 画像診断技術の進歩

- 業界の潜在的リスク&課題

- 先端システムの高コスト

- 製品リコールと再生品の入手可能性

- 促進要因

- 成長可能性分析

- 規制状況

- パイプライン分析

- ポーター分析

- PESTEL分析

- 今後の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2032年

- 主要動向

- 台

- 手術台

- 診察台

- 放射線透過イメージングテーブル

- アクセサリー

- 放射線治療固定製品

- その他アクセサリー

- その他の製品

第6章 市場推計・予測:用途別、2021年~2032年

- 主要動向

- 外科手術

- 診断

- リハビリテーション

第7章 用途別市場推計・予測:最終用途別、2021年~2032年

- 主要動向

- 病院および診療所

- 外来手術センター

- その他のエンドユーザー

第8章 市場推計・予測:地域別、2021年~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東とアフリカ

第9章 企業プロファイル

- Baxter International Inc.

- CQ Medical

- C-RAD

- Elekta AB

- Getinge AB

- Guangzhou Renfu Medical Equipment Co, Ltd

- Medline Industries, LP.

- Mizuho Medical Co. Ltd.

- ORFIT INDUSTRIES NV

- Smith & Nephew PLC

- STERIS plc

- Stryker Corporation

The Patient Positioning Systems Market size will register 3.6% CAGR during 2024-2032, driven by the rising incidence of chronic diseases and surgical procedures. According to WHO, noncommunicable diseases (NCDs) account for 41 million deaths annually, representing 74% of all global mortality. Chronic conditions such as cardiovascular diseases, cancer, and orthopedic disorders often require surgical interventions and diagnostic procedures that rely on precise patient positioning to ensure effective treatment and accurate medical imaging. Patient positioning systems play a crucial role in facilitating safe and optimal patient alignment during surgeries and diagnostic tests, thereby enhancing procedural outcomes and patient recovery times.

Healthcare facilities are prioritizing ergonomic considerations to enhance patient comfort, minimize injury risks for healthcare providers, and optimize procedural efficiency. As medical professionals strive to improve patient outcomes and operational workflows, the demand for ergonomic patient positioning solutions continues to grow, driving market expansion.

The patient positioning systems industry is classified based on product, application, end-use, and region.

The accessories segment will grow rapidly through 2032, owing to their design to support patients and facilitate accurate positioning according to clinical requirements. As healthcare facilities prioritize patient safety and ergonomic considerations, the demand for specialized accessories tailored to different medical specialties continues to grow. Manufacturers are focusing on developing accessories that are durable, easy to clean, and compatible with various patient positioning systems, thereby catering to diverse healthcare settings and improving overall patient care outcomes.

The diagnostics segment will generate significant demand over the forecast period, as patient positioning systems are essential for precise imaging and diagnostic procedures. These systems facilitate accurate positioning of patients for radiological examinations such as X-rays, CT scans, and MRI scans, ensuring optimal imaging quality and diagnostic accuracy. The integration of advanced imaging technologies with ergonomic positioning solutions enables healthcare providers to obtain clear and detailed diagnostic images while minimizing patient discomfort and radiation exposure.

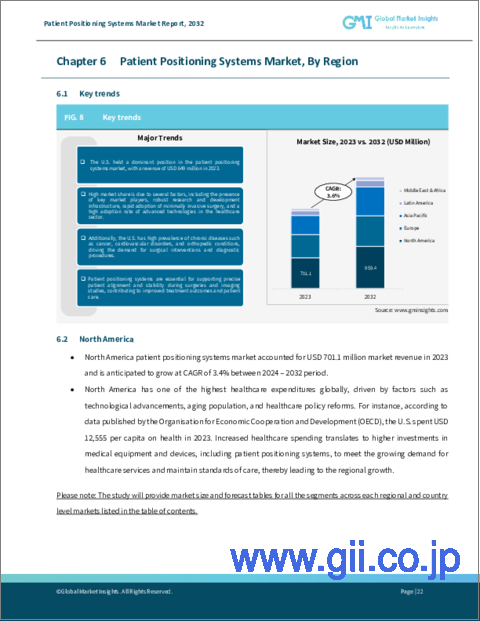

Europe patient positioning systems industry size will expand at a fast pace through 2032, driven by advancements in healthcare infrastructure, increasing medical spending, and a growing elderly population. Countries like Germany, France, and the United Kingdom lead in healthcare innovation and technology adoption, fostering demand for state-of-the-art patient positioning solutions. The stringent regulatory framework and emphasis on patient safety further encourage the adoption of ergonomic and user-friendly positioning systems across hospitals and diagnostic centers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360 degree synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Growing healthcare expenditure

- 3.2.1.3 Rise in number of surgical procedures

- 3.2.1.4 Technological advancements in diagnostic imaging

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of advanced systems

- 3.2.2.2 Product recalls and availability of refurbished systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Future market trends

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2032 ($ Mn)

- 5.1 Key trends

- 5.2 Tables

- 5.2.1 Surgical tables

- 5.2.2 Examination tables

- 5.2.3 Radiolucent imaging tables

- 5.3 Accessories

- 5.3.1 Radiotherapy immobilization/ fixation products

- 5.3.2 Other accessories

- 5.4 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2032 ($ Mn)

- 6.1 Key trends

- 6.2 Surgery

- 6.3 Diagnostics

- 6.4 Rehabilitation

Chapter 7 Market Estimates and Forecast, By End-use, 2021 - 2032 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Ambulatory surgical centers

- 7.4 Other end-users

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2032 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Baxter International Inc.

- 9.2 CQ Medical

- 9.3 C-RAD

- 9.4 Elekta AB

- 9.5 Getinge AB

- 9.6 Guangzhou Renfu Medical Equipment Co, Ltd

- 9.7 Medline Industries, LP.

- 9.8 Mizuho Medical Co. Ltd.

- 9.9 ORFIT INDUSTRIES NV

- 9.10 Smith & Nephew PLC

- 9.11 STERIS plc

- 9.12 Stryker Corporation